Homeowners insurance policy documents with calculator, dollar bills, house keys, and small house model on wooden desk — flat lay view

What Is the Average Deductible for Homeowners Insurance?

Content

Most American homeowners carry deductibles between $1,000 and $2,500—that's your personal bill before insurance pays a dime. The national median sits right at $1,500 as of 2024.

Your location changes everything. A Tampa homeowner might stare down a $12,000 hurricane deductible (5% of a $240,000 home), while someone in Vermont picks from $500, $1,000, or $1,500 flat rates. Same country, completely different financial exposure.

Getting this choice wrong costs you either way. Set it too low and you're overpaying premiums by hundreds annually. Set it too high and you'll panic when trying to scrape together $5,000 after a kitchen fire. Let's examine actual market data, regional differences, and a decision framework that matches your bank account.

How Homeowners Insurance Deductibles Work

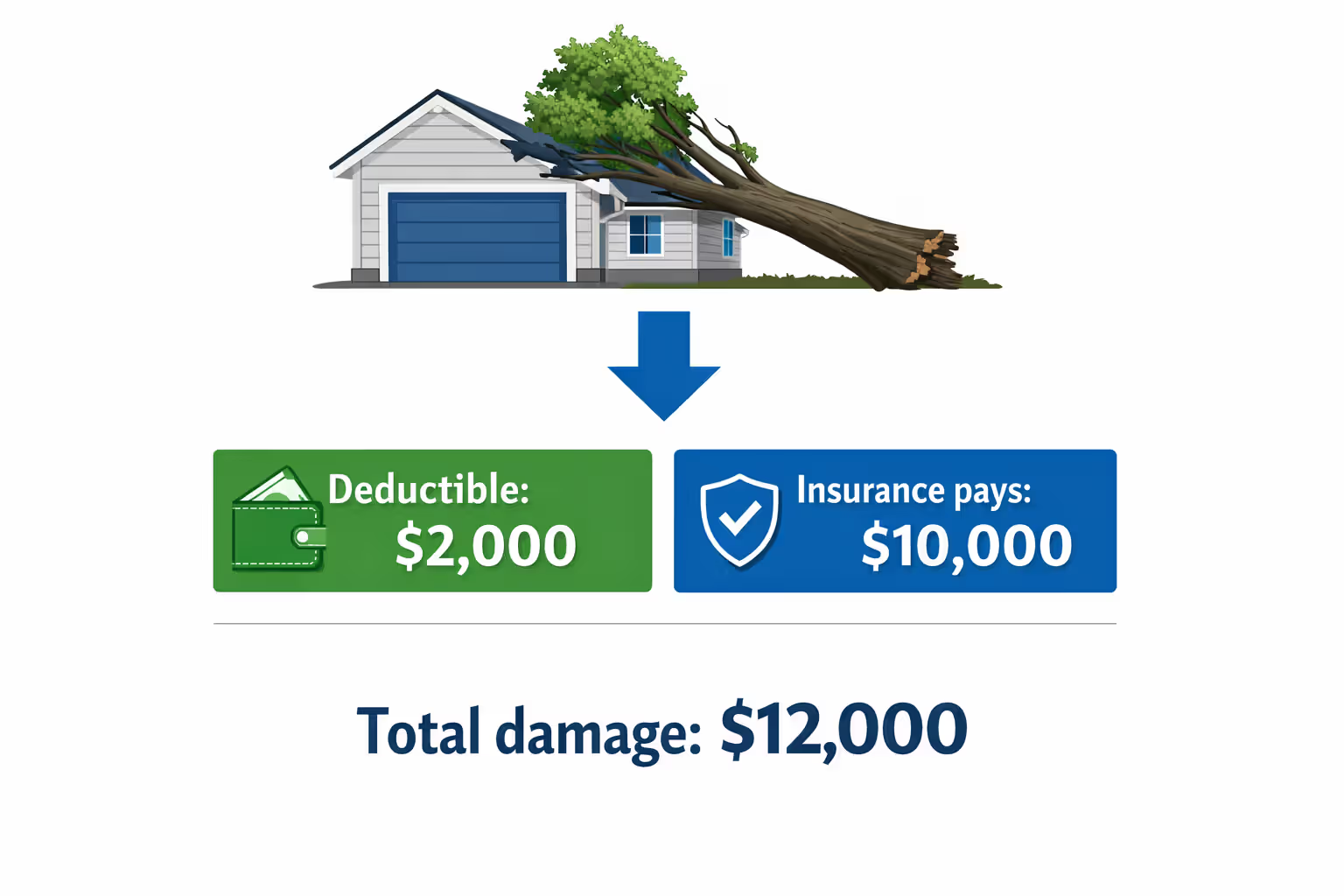

Think of your deductible as the first chunk of repair costs you cover solo. A tree crushes your garage, causing $12,000 damage. With a $2,000 deductible, you pay the first two thousand, and insurance cuts a check for the remaining ten.

Insurers offer two structures: flat-dollar amounts ($500, $1,000, $2,500) or percentages calculated from your dwelling coverage limit. Example—your policy covers $400,000 and carries a 1% deductible. You're responsible for $4,000 before coverage begins.

Every individual claim resets the deductible. Experience four separate incidents in one year? You'll pay four deductibles. Insurance policies don't work like health coverage with annual maximums—each disaster triggers a fresh payment from you.

Standard deductibles apply to fire, theft, vandalism, lightning strikes, and most common perils. But insurers frequently attach separate, steeper deductibles for region-specific disasters. Charleston residents might carry a $1,000 standard deductible yet face a $9,000 hurricane deductible (3% of $300,000 coverage). Identical house, vastly different costs depending whether fire or wind causes the damage.

The kicker? You don't get to pick which deductible applies—the cause of loss determines it. Hurricane damages your roof and interior? Hurricane deductible. Lightning strikes the same roof two months later? Standard deductible.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Current Deductible Averages Across the United States

National claims data from 2024 reveals where most homeowners land on deductible choices. The median deductible sits at $1,500, with roughly 70% of policies carrying deductibles between $500 and $2,500.

Breaking down what's typical for homeowners insurance deductibles:

- $500: 15% of all policies

- $1,000: 35% of all policies

- $1,500: 20% of all policies

- $2,000–$2,500: 18% of all policies

- $5,000 or more: 8% of all policies

- Percentage-based (standard coverage): 4% of policies, excluding catastrophe riders

This distribution has shifted noticeably over the past decade. In 2010, $500 deductibles dominated—now many carriers won't even write policies below $1,000. Insurers actively push customers toward higher deductibles through premium discounts, and it's working.

Percentage deductibles remain uncommon for everyday coverage but become mandatory in hurricane-exposed counties. These range from 1% on the low end to 10% in the most vulnerable coastal zones.

Converting Percentages Into Actual Dollar Amounts

Understanding deductible averages for homeowners insurance policies requires seeing how percentages translate into cash you'll actually pay:

| Deductible % | Home Value: $200K | Home Value: $300K | Home Value: $500K |

| 0.5% | $1,000 | $1,500 | $2,500 |

| 1% | $2,000 | $3,000 | $5,000 |

| 2% | $4,000 | $6,000 | $10,000 |

| 5% | $10,000 | $15,000 | $25,000 |

Watch what happens as home values climb—a seemingly modest 2% becomes a $10,000 financial shock for anyone with a half-million-dollar property. That's substantially more than most American households maintain in readily accessible emergency savings.

Deductible Ranges by State and Region

Geography rewrites the rules on homeowners insurance deductible ranges. States hammered regularly by natural disasters enforce higher minimums, while calmer regions offer flexibility.

Low-risk states including Vermont, Utah, Oregon, and Wisconsin typically allow $500–$1,500 flat deductibles. Insurers compete aggressively in these markets since catastrophic losses rarely materialize. Shopping around actually produces meaningful options.

Moderate-risk regions spanning the Midwest and Mid-Atlantic generally see $1,000–$2,500 ranges. Missouri, Ohio, Pennsylvania, and Virginia experience occasional severe weather—tornadoes, ice storms, heavy wind—without the frequency or intensity of coastal zones.

High-risk coastal states complicate everything. Florida, Louisiana, Texas, the Carolinas, and even New York's coastal counties frequently require percentage-based deductibles specifically for wind and hurricane damage. These typically start at 2% and climb to 5% or higher in ZIP codes directly on the water.

California's expanding wildfire zones have watched carriers impose 2%–5% percentage deductibles exclusively for fire claims in elevated-risk areas. Someone in Paradise, California might carry a $1,500 standard deductible but face $8,000 (2% of $400,000) when wildfire threatens.

Gulf Coast properties showcase the most extreme variation in deductible benchmarks for homeowners insurance. A Mobile, Alabama homeowner could be juggling: - $2,000 standard deductible for fire, theft, lightning, vandalism - 5% hurricane deductible—$15,000 on a $300,000 home - Separate 2% wind/hail deductible at $6,000

Insurance is not about the premium you pay today — it is about the check you can write tomorrow. A deductible should never be a number that looks good on paper but devastates your household when a real loss occurs. The smartest policyholders choose deductibles they can fund from savings within forty-eight hours, not amounts that force them into debt during their worst moments.

— Robert P. Hartwig

Special Deductibles for Wind, Hail, and Hurricane Damage

Nineteen states currently permit or mandate separate wind/hail deductibles, while hurricane deductibles apply along the entire Gulf and Atlantic coastline from Texas through Maine. Insurers introduced these to limit exposure during catastrophic storm seasons.

Hurricane deductibles activate under defined triggers: official National Weather Service hurricane declarations, named storms achieving specific sustained wind speeds, National Hurricane Center warnings affecting your county. Each carrier and state regulatory authority sets slightly different activation criteria—check your specific policy language.

Oklahoma, Kansas, Colorado, and parts of Texas employ wind/hail deductibles addressing constant severe thunderstorms and tornadoes. Moore, Oklahoma has been leveled by twisters multiple times. Residents there might pay $1,000 after an electrical fire but owe $4,000 when a tornado shreds their roof.

This structure explains why some homeowners face sticker shock when filing claims. Your declarations page (that multi-page document you received at purchase) spells out which perils trigger which deductible amounts. Locate it and actually read through the deductible section—before you need to file a claim.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Factors That Influence Your Deductible Amount

Several variables control which deductible options insurers offer and which amount serves your situation.

Your property's insured value and dwelling coverage directly dictate percentage deductibles. Two neighbors with identical $250,000 homes face vastly different costs if one carries $250,000 coverage and the other rebuilt their policy at $450,000 after renovations.

Location and disaster history restrict your available choices. Carriers operating in hurricane territory routinely refuse wind deductibles below 2%. You can't simply select a lower figure when underwriters classify your ZIP code as high-hazard.

Your claims history reshapes both availability and pricing. File two or three claims and insurers may mandate higher deductibles as a condition of renewal. Three claims within five years? Finding any carrier willing to offer $500 deductibles becomes nearly impossible.

Mortgage lender requirements occasionally cap maximum deductibles. Some lenders prohibit deductibles exceeding 2% of dwelling coverage or $5,000, whichever produces a lower number. This safeguards their collateral interest in your property.

The premium-deductible relationship creates the central balancing act. Increasing your deductible from $1,000 to $2,500 typically reduces annual premiums by $200–$400. The typical deductible for homeowners insurance policies reflects this calculation—most people settle on amounts delivering meaningful premium cuts without creating potential financial disasters.

Your emergency fund reality should dominate every other factor. A $5,000 deductible generates attractive premium savings but transforms into a nightmare scenario when you can't produce $5,000 within days after covered damage occurs.

Author: Marcus Hollowell;

Source: sixth-fleet.com

How to Choose the Right Deductible for Your Situation

Selecting your deductible demands uncomfortable honesty about financial reserves and risk tolerance. Start by examining liquid savings you could access within 48 hours.

Financial advisors generally recommend emergency funds covering 3–6 months of essential expenses. Already there? Consider setting your deductible at roughly one month's spending. A household spending $4,500 monthly could reasonably handle a $4,500 deductible while capturing substantial premium reductions.

No emergency fund yet or still building it? Stick with lower deductibles despite higher premiums. An extra $350 annually beats desperately hunting for $2,500 after a pipe bursts and floods your basement.

Calculate the break-even timeline on deductible increases. Suppose raising your deductible from $1,000 to $2,500 saves $300 annually. If you file one claim, recovering that higher out-of-pocket expense takes roughly five years. File zero claims? You pocket $300 every year indefinitely.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Consider your home's age and condition honestly. Older houses with 30-year-old roofs, original plumbing, and outdated electrical systems generate more claims. A 1975 house might justify a $1,000 deductible compared to 2020 new construction, even with higher premiums.

Industry expert perspective:

"The standard deductible for homeowners insurance needs to match actual available cash, not whatever generates the lowest premium quote," notes Jennifer Harrington, a CFP specializing in property insurance for 22 years. "I've watched countless families grab $5,000 deductibles to save $400 yearly, then scramble desperately when they can't fund repairs following losses. Your deductible represents self-insurance for initial damage—make sure you can actually bankroll that self-insurance when problems hit."

Walk through realistic claim scenarios mentally. Would you actually file a claim for $1,800 damage with a $1,000 deductible? Many homeowners wouldn't—that $800 net benefit doesn't justify potential rate increases or non-renewal risks. This suggests a higher deductible might work since you're already self-insuring smaller losses.

Revisit your deductible annually at policy renewal. Home values appreciate, personal finances shift, risk tolerance evolves. The optimal deductible at age 35 might make zero sense at 55 after accumulating substantially more savings.

Common Mistakes Homeowners Make With Deductibles

Chasing premium savings without adequate reserves. The most damaging mistake involves selecting extremely high deductibles purely for reduced monthly costs. Someone barely saving $150 monthly has no business carrying a $5,000 deductible, regardless of premium reductions offered.

People obsess over saving fifty dollars a month on premiums and completely ignore the five-thousand-dollar trap they are building for themselves. The deductible is not a discount lever — it is a promise you make to your future self that you will have that money ready on the worst day of the year. Treat it like a commitment, not a negotiation tactic.

— Loretta Worters

Overlooking that multiple deductibles exist. Countless homeowners discover their 5% hurricane deductible only after filing claims post-storm. Review your declarations page annually and specifically confirm deductible amounts for wind, hail, hurricane, earthquake, and any other coverage extensions relevant to your region.

Ignoring automatic deductible increases after improvements. Add a $60,000 addition and your dwelling coverage increases proportionally, automatically inflating percentage-based deductibles. Your 2% deductible jumps from $5,000 to $6,200 without you actively changing anything. Verify deductible implications whenever coverage limits rise following renovations or market appreciation.

Skipping coordination with umbrella liability policies. Some umbrella policies require underlying homeowners coverage maintaining deductibles below specific thresholds. Confirm umbrella policy terms before dramatically raising deductibles—you might inadvertently void umbrella coverage.

Assuming all carriers offer identical structures. Carrier A might provide $500 increments ($1,000, $1,500, $2,000) while Carrier B leaps directly from $1,000 to $2,500 with nothing between. Shop multiple insurers to locate deductible structures matching your financial preferences.

Failing to calculate realistic loss scenarios. Before committing to a deductible change, work through plausible losses: complete roof replacement, major water damage, significant theft. Does that $5,000 deductible still feel manageable when you visualize writing the actual check during an already stressful situation?

Frequently Asked Questions About Homeowners Insurance Deductibles

Making Your Deductible Decision

Your homeowners insurance deductible boils down to a personal financial choice balancing premium costs against potential out-of-pocket expenses during already-stressful moments. Deductible averages for homeowners insurance policies provide helpful benchmarks, but your ideal amount depends on emergency savings, risk exposure, and financial priorities.

Start by confirming your current deductible—surprisingly, many homeowners don't actually know this figure until filing claims. Check your declarations page for standard deductibles plus any special deductibles for wind, hurricane, or other regionally common perils.

Assess your genuine financial capacity to absorb different deductible amounts without borrowing or raiding retirement accounts. This honest evaluation matters more than premium savings or national statistics.

Request quotes at three different deductible levels to view actual premium differences. The savings sometimes surprise people—occasionally the premium gap between $1,000 and $2,500 deductibles is negligible, making the lower option an obvious winner.

Weigh your property's condition, claim likelihood based on local hazards, and personal tolerance for financial uncertainty. A cautious homeowner with robust emergency savings might still prefer a $1,000 deductible for peace of mind, and that's completely rational.

Reassess your deductible annually as finances evolve. The right choice at policy inception might not fit circumstances five years later after building savings or eliminating debts.

Your deductible selection ultimately reflects how much risk you'll retain versus transfer to insurers. Neither high nor low deductibles are inherently superior—the right amount is whatever you can comfortably afford when disaster strikes while paying premiums that fit your budget during normal times.