Mortgage documents, small house model, insurance envelope, and calculator on a desk — escrow and homeowners insurance concept

Is Home Insurance Paid Through Escrow? Understanding Your Mortgage Payment Options

Content

When you sign mortgage paperwork at closing, you'll notice your monthly payment often exceeds the principal and interest you calculated. That extra amount typically covers property taxes and homeowners insurance—funds your lender collects and holds in an escrow account. But is home insurance paid through escrow mandatory, or do you have alternatives?

The answer depends on your loan type, down payment, and lender policies. Most borrowers with conventional loans and less than 20% down will find escrow required. FHA, VA, and USDA loans almost always mandate escrow regardless of equity. Understanding how this system works helps you manage costs, avoid surprises, and decide whether keeping insurance in escrow makes sense for your situation.

"Escrow accounts provide a structured payment method that protects both the homeowner and lender from lapses in coverage. Many borrowers appreciate the convenience of spreading large annual premiums across twelve months rather than facing a lump-sum bill." — Michael Torres, Senior Loan Officer, Apex Mortgage Solutions

How Mortgage Escrow Accounts Handle Homeowners Insurance Payments

Your mortgage escrow account functions as a holding pen for property-related expenses. Each month, your servicer collects a portion of your estimated annual homeowners insurance premium and property taxes, deposits those funds into the escrow account, then pays the bills when they come due.

Here's the basic calculation: if your annual homeowners insurance premium is $1,800, your servicer divides that by 12 and adds $150 to your monthly mortgage payment. The same process applies to property taxes. Your total monthly payment—often called PITI (Principal, Interest, Taxes, Insurance)—bundles everything into one predictable amount.

Servicers maintain a cushion in your escrow account, typically two months' worth of expenses, to handle payment timing mismatches and small increases in premiums or taxes. If your insurance bill arrives before you've accumulated enough monthly deposits, that cushion covers the gap. Federal regulations under the Real Estate Settlement Procedures Act (RESPA) cap this cushion at one-sixth of the total annual escrow disbursements, though servicers often keep less.

When your insurance renewal notice arrives, your servicer reviews it, confirms coverage meets lender requirements, and issues payment directly to your insurance company. You won't write a check or manage the transaction—the servicer handles everything behind the scenes. This arrangement continues until you pay off the mortgage, refinance, or qualify to remove escrow.

The mortgage escrow homeowners insurance payments system creates a three-party relationship: you fund the account, the servicer manages it, and the insurer receives payment. Each party has specific responsibilities that keep coverage active and protect the property securing your loan.

When Lenders Require Escrow for Homeowners Insurance

Lenders require escrow accounts primarily to protect their collateral. If your homeowners insurance lapses and a fire destroys the house, the lender loses its security for the loan. Escrow requirements reduce this risk by ensuring premiums get paid on time.

Author: Lauren Bishop;

Source: sixth-fleet.com

Loan Types and Escrow Requirements

Government-backed loans impose the strictest escrow rules. FHA loans require escrow for insurance and taxes throughout the loan term with very limited exceptions. VA loans mandate escrow for all borrowers unless you're a qualified veteran refinancing with specific exemptions. USDA loans similarly require escrow accounts for the life of the loan.

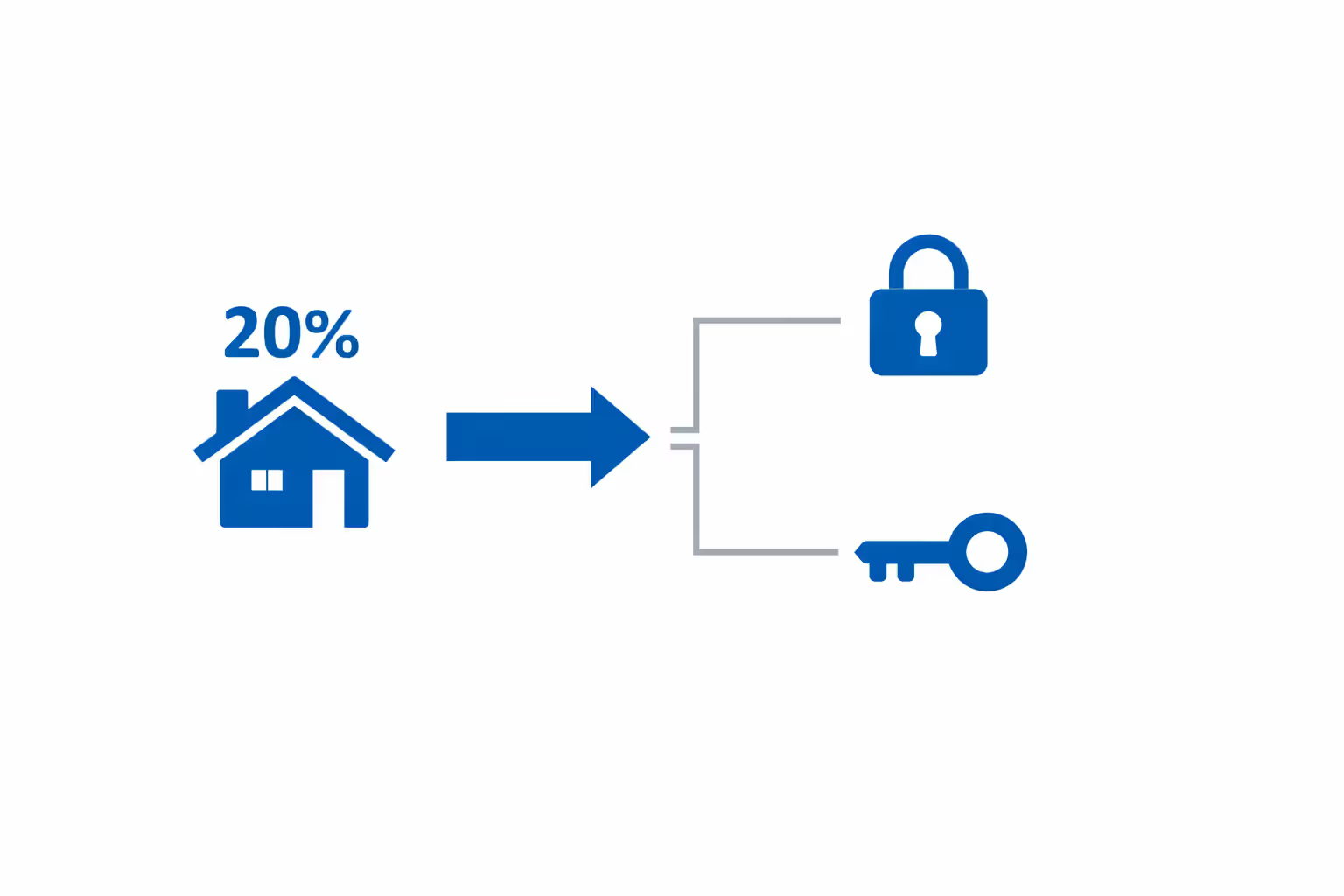

Conventional loans backed by Fannie Mae or Freddie Mac follow different rules. These loans typically require escrow when your loan-to-value ratio exceeds 80%—meaning you put down less than 20%. Once you build sufficient equity, you may request escrow removal, though lenders can refuse if you have a history of late payments.

Some portfolio lenders—banks that keep loans on their own books rather than selling them—offer more flexibility. These institutions set their own escrow policies and may waive requirements for borrowers with excellent credit and substantial down payments.

Down Payment Thresholds That Trigger Escrow

The 20% down payment threshold serves as the primary dividing line for conventional loans. Borrow $300,000 with a $60,000 down payment (20%), and you might avoid mandatory escrow. Put down $45,000 (15%), and escrow becomes required.

Lenders view higher loan-to-value ratios as riskier. Borrowers with less equity have more incentive to walk away if property values decline or financial hardship strikes. Requiring an escrow account insurance homeowners arrangement gives lenders control over insurance payments during this higher-risk period.

Some lenders offer escrow waivers even with less than 20% down, but expect to pay a fee—often 0.25% of the loan amount—or accept a slightly higher interest rate. This trade-off makes sense for borrowers who want payment flexibility and can manage large annual insurance bills without missing deadlines.

Refinancing can change your escrow status. If you originally put down 10% but now have 25% equity through payments and appreciation, your new loan might not require escrow. However, many borrowers choose to keep escrow even when optional because the convenience outweighs the minor loss of control.

Step-by-Step: The Escrow Insurance Payment Process for Homeowners

Understanding the escrow insurance payment process homeowners experience helps you anticipate changes in your monthly payment and avoid confusion when servicers send annual statements.

At closing: Your lender collects an initial escrow deposit covering several months of insurance and taxes. This upfront amount ensures sufficient funds exist to pay the first bills that come due. You might deposit three to six months of insurance premiums at closing, depending on when your policy renews.

Monthly deposits: Starting with your first payment, the servicer collects 1/12 of your estimated annual insurance premium. These funds sit in the escrow account earning minimal or no interest (requirements vary by state).

Premium payment: When your insurance company sends the renewal bill—typically 30 to 45 days before the policy expires—your servicer reviews the coverage and amount. If everything checks out, they issue payment directly to the insurer before the due date. You never see the bill or write a check.

Annual escrow analysis: Once per year, your servicer performs an escrow analysis comparing actual disbursements to the amounts collected. If insurance premiums increased, your monthly payment rises to cover the higher cost plus replenish any shortage. If premiums decreased, you might receive a refund or see a lower monthly payment.

Shortage scenarios: When actual expenses exceed collections, you face an escrow shortage. Servicers typically spread this shortage over 12 months by increasing your monthly payment. A $600 shortage means your payment increases by $50 monthly for the next year, plus the amount needed for the coming year's expenses.

Surplus handling: If your escrow account holds more than the allowed cushion after paying all bills, the servicer must refund the excess (usually amounts over $50) or apply it to the next year's escrow payments, reducing your monthly amount.

This cycle repeats annually. Your payment adjusts up or down based on actual insurance costs and tax bills, keeping the escrow account balanced without requiring you to track payment dates or manage large lump-sum expenses.

The escrow process may seem complex at first glance, but it is essentially a safeguard built into the mortgage system. By collecting small amounts monthly, it prevents homeowners from facing financial shock when large insurance and tax bills come due all at once

— Robert Kiyosaki

Pros and Cons of Paying Homeowners Insurance Through Mortgage Escrow

Paying homeowners insurance through mortgage escrow offers distinct advantages and disadvantages depending on your financial habits and preferences.

Convenience ranks as the primary benefit. You make one monthly payment covering everything—no need to remember insurance due dates or scramble for a large annual premium. The servicer handles all payment logistics, reducing your mental load.

Budgeting simplicity helps many homeowners manage cash flow. Instead of saving throughout the year for a $2,400 insurance bill, you pay $200 monthly as part of your mortgage. This forced savings prevents the temptation to spend those funds elsewhere.

Lender oversight provides a safety net. Your servicer monitors policy renewals and ensures coverage never lapses. If your insurance company fails to send a bill, the servicer will investigate rather than letting coverage expire silently.

Reduced control represents the main drawback. You can't earn interest on escrow funds in most states, and you can't time insurance payments strategically. If you find a better insurance rate mid-year, you'll need to coordinate the switch through your servicer rather than handling it directly.

Escrow shortages create payment volatility. A 15% insurance increase means your monthly mortgage payment jumps, potentially straining your budget. With direct payment, you'd see the increase coming and could shop for alternatives before renewal.

Delayed refunds frustrate borrowers who pay off loans or refinance. Escrow refund checks often take 30 to 45 days to arrive, tying up funds you might need for closing costs or other expenses.

| Feature | Paying Through Escrow | Paying Directly |

| Payment frequency | Monthly (1/12 of annual premium) | Annual or semi-annual lump sum |

| Control over funds | Limited; servicer manages account | Full control; you manage savings |

| Risk of missed payments | Very low; servicer handles deadlines | Higher; you must track due dates |

| Potential savings opportunities | Limited; harder to switch carriers mid-year | Better; you can shop and switch anytime |

| Lender requirements | Often mandatory with <20% down | Available only when permitted by lender |

| Refund timeline | 30-45 days after payoff/refinance | Immediate control of unused premiums |

What Happens When Your Escrow Account Runs Short or Has a Surplus

Escrow accounts rarely stay perfectly balanced. Insurance premiums fluctuate, property tax assessments change, and initial estimates miss the mark. Understanding how servicers handle these imbalances prevents surprise payment increases.

Shortages occur when disbursements exceed collections. Your insurance company raises premiums by $300 annually, but your escrow account only collected the previous year's lower amount. The servicer pays the higher premium, creating a $300 deficit.

Servicers handle shortages in two ways: they calculate the shortage amount, then increase your monthly payment to both repay the deficit over 12 months and collect enough for the coming year's higher expenses. A $300 shortage means your payment increases by $25 monthly to repay the shortage, plus an additional increase to cover the new premium level.

Some servicers offer to let you pay the shortage as a lump sum, avoiding the monthly payment increase. This option makes sense if you have cash available and want to minimize your ongoing monthly obligation.

Surpluses happen when escrow accounts accumulate more than needed. Perhaps you switched to a cheaper insurance policy, or your tax assessment decreased on appeal. After the annual analysis, the servicer finds $800 more than the maximum allowed cushion.

Federal regulations require servicers to refund surpluses exceeding $50. You'll receive a check for the excess amount, or the servicer will apply it to your escrow account, reducing next year's monthly payment. The choice often depends on the surplus size—larger amounts typically trigger automatic refunds.

Author: Lauren Bishop;

Source: sixth-fleet.com

Cushion adjustments fine-tune your escrow balance. Servicers can maintain up to two months' worth of expenses as a cushion, but they often keep less. If your payments consistently arrive on time and expenses stay predictable, the servicer might reduce the cushion, lowering your monthly payment slightly.

Review your annual escrow statement carefully. These documents detail every deposit and disbursement, explain payment changes, and show the projected balance for the coming year. Errors happen—servicers occasionally pay the wrong amount or miscalculate required reserves. Catching mistakes early prevents compounding problems.

How to Remove Homeowners Insurance from Escrow (And Whether You Should)

Many homeowners want to remove escrow accounts once they build sufficient equity. The process requires meeting specific criteria and submitting a formal request.

Eligibility requirements typically include: - Loan-to-value ratio below 80% (at least 20% equity) - No late mortgage payments in the past 12 months - Conventional loan (FHA, VA, and USDA loans rarely allow escrow removal) - No recent escrow shortages or payment issues - Lender approval (not guaranteed even if you meet other criteria)

The formal request process starts with contacting your servicer. Request their specific escrow waiver requirements in writing—policies vary by institution. You'll likely need to provide proof of current homeowners insurance and demonstrate financial stability.

Some servicers charge a one-time escrow waiver fee, typically $200 to $500. Others require you to maintain a slightly higher interest rate (often 0.125% to 0.25%) as compensation for the increased risk they assume when you self-manage insurance payments.

Risks of self-managing include missing payment deadlines, losing track of renewal dates, or spending insurance money on other expenses. If your coverage lapses, your lender will purchase expensive force-placed insurance and bill you for it—often at two to three times the cost of a standard policy.

Approval criteria extend beyond equity. Lenders review your payment history, credit score, and overall relationship. A borrower with 25% equity but three late payments in the past year will likely face denial. Someone with 22% equity and a perfect payment record might get approved.

Consider keeping escrow even when removal becomes optional. The convenience often outweighs the minor benefits of controlling the funds yourself. However, financially disciplined borrowers who want to earn interest on insurance savings or prefer managing their own payment schedule find direct payment worthwhile.

If you remove escrow, set up automatic savings transfers to a dedicated account. Transfer 1/12 of your annual premium monthly, ensuring funds are available when the bill arrives. Calendar reminders 60 days before renewal help you shop for better rates without risking a coverage gap.

Financial discipline is not about restricting yourself—it is about creating systems that work in your favor. Whether you manage insurance payments through escrow or on your own, the key is building a structure that ensures you never leave your most valuable asset unprotected

— Suze Orman

Common Mistakes Homeowners Make with Escrow Insurance Payments

Even with servicers managing payments, homeowners make errors that create problems and cost money.

Ignoring escrow statements tops the list. These annual documents arrive in the mail, often get filed away unread. But they contain critical information: payment increases, shortage explanations, and disbursement details. A servicer paying the wrong insurance company or sending money to a canceled policy only gets caught if you review the statement.

Assuming escrow covers everything creates dangerous gaps. Escrow accounts handle standard homeowners insurance and property taxes, but flood insurance, earthquake coverage, and umbrella policies require separate payments. Borrowers sometimes believe their mortgage payment includes all insurance, then face devastating losses when a flood isn't covered.

Not shopping for better rates wastes money. When your servicer pays insurance automatically, you lose the annual reminder to compare quotes. Set a calendar alert 90 days before renewal to request quotes from multiple insurers. Even if you save $200 annually, that's $6,000 over a 30-year mortgage.

Failing to update coverage leaves you underinsured. Home values rise, renovation projects increase replacement costs, and inflation drives up rebuilding expenses. Your escrow account will pay whatever premium the insurance company charges, but if that premium reflects outdated coverage limits, you'll face out-of-pocket costs after a major loss.

Canceling insurance without lender notification triggers force-placed coverage. You switch insurance companies to save money but forget to notify your servicer. The old policy cancels, the servicer doesn't receive a new policy declaration, and they purchase expensive lender-placed insurance automatically. You end up paying for both policies until the mess gets sorted out.

Spending escrow refunds immediately creates problems when shortages arrive. You refinance, receive a $2,000 escrow refund check, and spend it on vacation. Six months later, your new servicer notifies you of a $1,500 shortage requiring higher monthly payments. The refund should have covered that shortage, but now you're struggling with increased payments.

Not maintaining required coverage levels violates your mortgage agreement. Lenders require replacement cost coverage meeting specific minimums. You reduce coverage to lower premiums, thinking the servicer won't notice. When they conduct an annual insurance review, they discover the deficiency and either require you to increase coverage or purchase force-placed insurance at your expense.

Author: Lauren Bishop;

Source: sixth-fleet.com

Frequently Asked Questions About Escrow and Homeowners Insurance

Conclusion

Homeowners insurance gets paid through escrow for most borrowers with less than 20% equity or government-backed loans. This arrangement offers convenience and forced savings but reduces your control over insurance funds and payment timing. Understanding how escrow accounts work—from monthly deposits to annual analyses to shortage handling—helps you manage costs and avoid surprises.

Whether you keep insurance in escrow or pay directly depends on your loan terms, equity position, and personal preferences. Borrowers who value simplicity and automatic payments benefit from escrow. Those who want to maximize interest earnings, maintain payment flexibility, or prefer direct control should explore escrow removal once they meet eligibility requirements.

Review your annual escrow statements, shop for competitive insurance rates before renewal, and maintain adequate coverage levels. These habits prevent costly mistakes regardless of your payment method. If you're unsure whether escrow makes sense for your situation, calculate the trade-offs: convenience and forced savings versus control and potential interest earnings. Most homeowners find the convenience worth the minor drawbacks, but your financial habits and priorities should guide the decision