Homeowners insurance policy document on desk with calculator small house model and US dollar bills representing deductible cost decision

What Is a Good Deductible for Home Insurance? A Homeowner's Guide to Choosing the Right Amount

Content

Choosing your home insurance deductible feels like a gamble. Set it too low, and you'll pay hundreds more each year in premiums. Set it too high, and one major claim could drain your savings account. Most homeowners pick a number without understanding the math behind it—or worse, they stick with whatever their agent suggested during a rushed phone call.

The right deductible depends on three things: how much cash you can access quickly, how much you'll save on premiums, and how likely you are to file a claim. A $1,000 deductible might be perfect for someone with $15,000 in emergency savings but disastrous for someone living paycheck to paycheck. Similarly, a coastal homeowner facing hurricane deductibles of 5% might owe $15,000 on a $300,000 home—far more than they expected.

This guide breaks down the real numbers, common traps, and a practical framework for selecting a deductible that protects both your home and your bank account.

How Home Insurance Deductibles Work and Why They Matter

Your deductible is the amount you pay out of pocket before your insurance company covers the rest of a claim. If a kitchen fire causes $8,000 in damage and you have a $1,000 deductible, you pay the first $1,000 and your insurer pays $7,000.

Higher deductibles mean lower premiums because you're accepting more financial risk. Insurers reward this by charging you less each month. The relationship isn't linear, though. Jumping from a $500 to $1,000 deductible typically saves 10-15% on premiums, but going from $2,500 to $5,000 might only save another 5-7%.

Most US homeowners select deductibles between $500 and $2,500. Standard policies offer flat-dollar options like $500, $1,000, $1,500, $2,000, $2,500, and $5,000. Some insurers cap maximum deductibles at $10,000 for standard coverage, though this varies by state and company.

The premium impact varies by location, home value, and insurer. A homeowner in Florida with hurricane exposure sees bigger premium swings between deductible levels than someone in Iowa with minimal catastrophic risk. This geographical difference makes deductible planning homeowners insurance decisions highly personal rather than one-size-fits-all.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Factors That Determine Your Ideal Deductible Amount

Your Emergency Savings and Financial Cushion

Financial advisors recommend keeping 3-6 months of expenses in accessible savings. Your home insurance deductible should never exceed what you can comfortably pay from this fund without creating hardship.

If you have $20,000 in emergency savings, a $2,500 deductible leaves you plenty of cushion. But if you only have $3,000 saved, even a $1,000 deductible represents a third of your safety net. One claim could force you to use credit cards or skip other essential expenses.

Consider this scenario: A homeowner with $5,000 in savings chooses a $2,500 deductible to save $200 annually on premiums. After two years of saving $400, a burst pipe causes $6,000 in damage. They now need to pay $2,500 upfront, leaving only $2,500 in their emergency fund. The premium savings evaporate when they can't cover other unexpected expenses that month.

The biggest mistake I see homeowners make is treating their deductible as just another number on a form. Your deductible is a financial commitment — a promise you’re making to yourself that you can write that check on the worst day of your year. If you can’t cover it without borrowing, you’ve chosen the wrong number, no matter how much you save on premiums.

— Loretta Worters

Home Value and Replacement Cost

Your home's replacement cost affects both your coverage needs and deductible selection. A $200,000 home and a $500,000 home face different deductible selection homeowners insurance policy considerations.

For expensive homes, percentage-based deductibles can create sticker shock. A 2% deductible on a $600,000 home means paying $12,000 out of pocket per claim. Many homeowners select these higher percentage deductibles for premium savings without calculating the actual dollar amount they'd owe.

Conversely, owners of modest homes sometimes choose deductibles that are too low relative to their home's value. A $500 deductible on a $150,000 home means filing claims for relatively minor damage—which can lead to rate increases or policy cancellations after multiple claims.

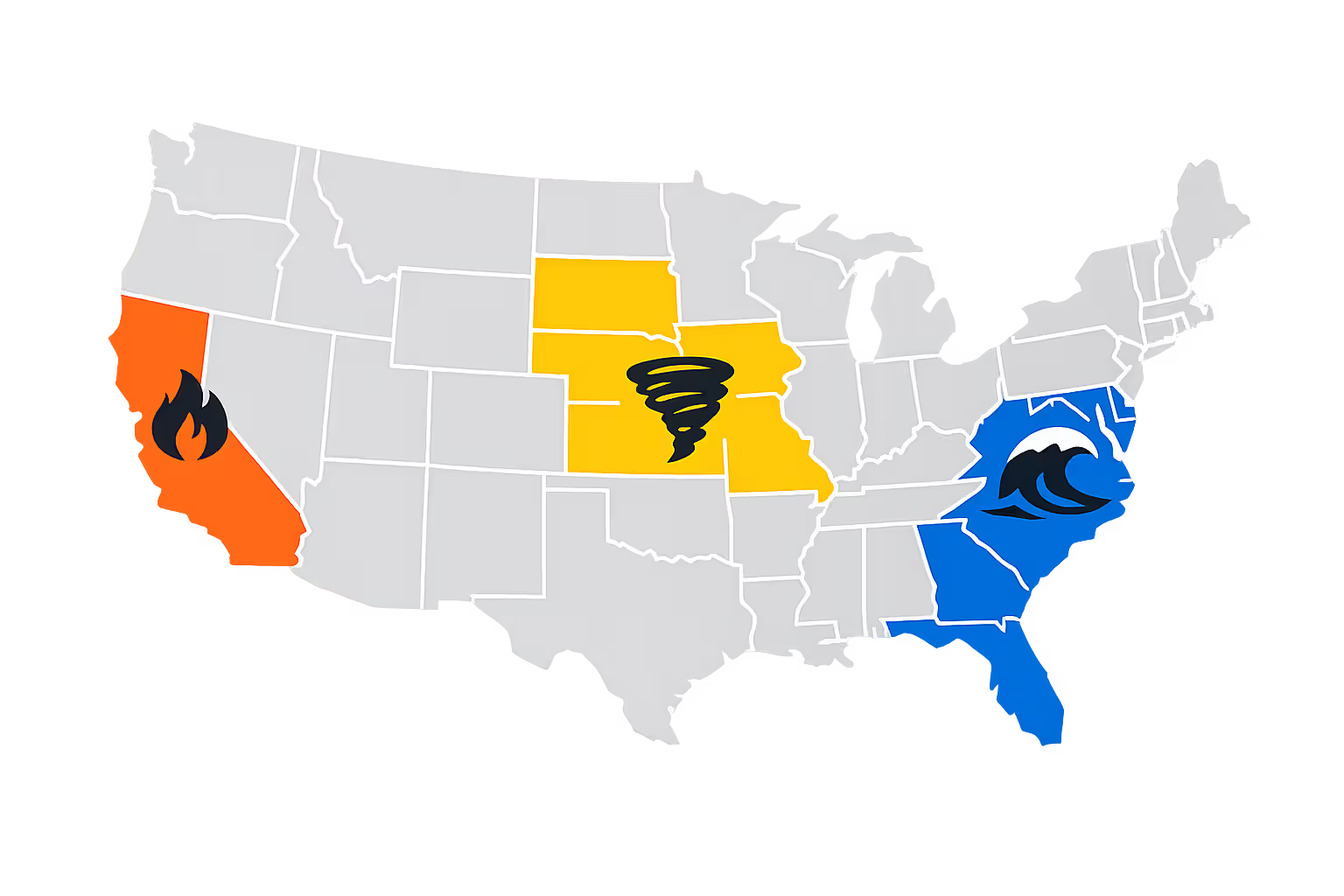

Location-Specific Risks (Hurricanes, Earthquakes, Wildfires)

Geography dramatically changes deductible planning homeowners insurance strategies. Coastal homeowners often face separate hurricane or wind/hail deductibles, typically 2-5% of the home's insured value. These apply only to storm-related claims, while standard deductibles cover other perils.

California homeowners need separate earthquake policies with deductibles commonly ranging from 10-25% of the dwelling coverage. A 15% deductible on a $400,000 home means paying $60,000 before coverage kicks in—essentially self-insuring for everything except catastrophic damage.

Wildfire-prone areas in the West have seen insurers impose higher minimum deductibles or percentage-based deductibles for fire claims. These location-specific requirements limit your choices and force higher out-of-pocket costs.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Claims History and Risk Profile

Your home's age, condition, and your claims history influence which deductible makes sense. Older homes with aging systems (roof, plumbing, electrical) face higher claim likelihood. If your roof is 18 years old and the average lifespan is 20 years, you might face a claim soon.

Homeowners who've filed multiple claims in recent years often see premium increases that dwarf any deductible-related savings. If you've filed two claims in three years, choosing a higher deductible helps avoid filing smaller claims that could trigger rate hikes or non-renewal.

The average homeowner files a claim once every 9-10 years. If your home is well-maintained and you're careful about preventing damage, a higher deductible becomes more attractive since you're unlikely to use it frequently.

Standard Dollar Deductibles vs. Percentage Deductibles: Which Should You Choose?

Flat-rate deductibles are straightforward: you pay the same dollar amount regardless of claim size. A $1,500 deductible means you pay $1,500 whether the claim is $3,000 or $50,000.

Percentage-based deductibles calculate your out-of-pocket cost as a percentage of your home's insured value. A 2% deductible on a $350,000 dwelling coverage limit equals $7,000 per claim. These appear most commonly for wind, hail, and hurricane damage in storm-prone regions.

Insurers push percentage deductibles in high-risk areas because they scale with home values and inflation. As your coverage increases, so does your deductible—without you actively choosing a higher amount. This deductible comparison homeowners insurance shoppers often miss during policy reviews.

Standard deductibles work better for most homeowners because they're predictable and manageable. You know exactly what you'll pay, making it easier to budget and maintain appropriate savings.

Percentage deductibles make sense only when they're mandatory or when the premium savings are substantial. Even then, calculate the actual dollar amount before agreeing. Many homeowners don't realize their 2% hurricane deductible equals $8,000 until they're filing a claim.

| Home Value | $1,000 Flat Deductible | 1% Deductible | 2% Deductible |

| $200,000 | $1,000 | $2,000 | $4,000 |

| $300,000 | $1,000 | $3,000 | $6,000 |

| $400,000 | $1,000 | $4,000 | $8,000 |

| $500,000 | $1,000 | $5,000 | $10,000 |

The table shows how percentage deductibles escalate quickly. A homeowner comfortable with a $1,000 flat deductible might struggle to pay $6,000 under a 2% deductible on a $300,000 home. This choosing deductible homeowners insurance guide emphasizes checking both types before signing.

The Premium Savings Calculator: What You Actually Save by Raising Your Deductible

Premium reductions from higher deductibles vary by insurer, location, and home characteristics. National averages provide a baseline, though your actual savings may differ by 20-30%.

| Deductible Amount | Average Annual Premium | Annual Savings vs. $500 | Years to Break Even |

| $500 | $1,500 | $0 | N/A |

| $1,000 | $1,320 | $180 | 2.8 years |

| $2,000 | $1,200 | $300 | 5.0 years |

| $2,500 | $1,140 | $360 | 5.6 years |

| $5,000 | $1,050 | $450 | 7.8 years |

These figures assume a $300,000 home with standard coverage. The break-even calculation shows how long you'd need to go without filing a claim for the higher deductible to pay off.

A homeowner switching from $500 to $1,000 saves $180 annually. If they file a claim after three years, they've saved $540 but pay an extra $500 out of pocket—a net benefit of $40. If they go five years without a claim, they've saved $900 while taking on only $500 in additional risk.

The deductible risk tradeoff homeowners insurance shoppers face becomes clear: higher deductibles benefit those who rarely file claims but hurt those who experience frequent damage. Since most homeowners file claims infrequently, higher deductibles usually win over time.

However, deductible comparison homeowners insurance strategies must account for claim severity. Small claims under $2,000 shouldn't be filed anyway due to rate increase risks, making low deductibles less valuable. You're effectively paying extra premium for coverage you shouldn't use.

Request quotes at multiple deductible levels from your insurer. Compare the annual savings against the increased out-of-pocket cost. If raising your deductible from $1,000 to $2,500 saves only $120 per year, it takes 12.5 years to break even—probably not worth it. But if it saves $400 annually, you break even in 3.75 years, making it more attractive.

Author: Ethan Caldwell;

Source: sixth-fleet.com

5 Common Mistakes Homeowners Make When Selecting Their Deductible

Choosing the lowest deductible without comparing savings. Many homeowners default to $500 or $1,000 deductibles without requesting quotes at higher levels. They might save $300-400 annually by accepting a $2,500 deductible they could easily afford, effectively paying thousands in unnecessary premiums over a decade.

Ignoring separate wind/hail or hurricane deductibles. Policies in storm-prone areas often include separate deductibles for wind damage. A homeowner might have a $1,000 standard deductible but a 2% hurricane deductible. After a hurricane causes $20,000 in damage to their $300,000 home, they're shocked to owe $6,000 instead of $1,000. Always check your declarations page for multiple deductible types.

Not adjusting deductibles as financial situations improve. You chose a $500 deductible five years ago when you had minimal savings. Now you have $25,000 in the bank and still pay for that low deductible. Reviewing and raising your deductible as your financial cushion grows can save hundreds annually without increasing your actual risk.

Failing to account for multiple claims scenarios. Some homeowners pick high deductibles thinking they'll never file claims, then experience two separate incidents in one year—maybe hail damage in spring and a kitchen fire in fall. Each claim requires paying the deductible separately. A $2,500 deductible becomes $5,000 in total out-of-pocket costs for two claims.

Overlooking minimum deductible requirements by location. Certain high-risk areas have mandatory minimum deductibles, often $2,500 or higher, or required percentage deductibles. Homeowners discover this only after purchasing in these areas, finding they can't choose the lower deductible they're comfortable with. Check local requirements before assuming all deductible options are available.

Insurance is the art of balancing what you can afford to lose against what you can afford to pay. A deductible that saves you three hundred dollars a year but leaves you financially exposed after a single claim isn’t a saving — it’s a delayed cost. Smart homeowners run the break-even math before they sign anything.

— J. Robert Hunter

How to Decide: A Step-by-Step Framework for Choosing Your Deductible

Assess your liquid savings. Calculate your total emergency fund—money in savings accounts, money market funds, or other accounts you can access within days. Subtract one month of essential expenses as a buffer. The remaining amount represents what you could potentially use for a deductible without creating financial hardship.

If you have $12,000 in savings and $4,000 in monthly expenses, you have $8,000 available. A $2,500 deductible leaves comfortable room; a $5,000 deductible is possible but tight; anything higher creates risk.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Calculate premium differences from your insurer. Contact your insurance company or agent and request premium quotes for deductibles at $500, $1,000, $1,500, $2,000, $2,500, and $5,000. Some insurers provide this information through online portals. Write down the annual premium for each option.

Subtract each premium from your current premium to see annual savings. Divide the difference in deductible amounts by annual savings to find break-even years. If increasing from $1,000 to $2,500 saves $250 per year, you break even in six years ($1,500 additional deductible ÷ $250 savings).

Consider your claim likelihood. Evaluate your home's condition, age, and your risk tolerance. Newer homes with updated systems face lower claim probability. Older homes or those with known issues (aging roof, old water heater) face higher risk.

Your behavior matters too. Careful homeowners who perform regular maintenance and address small issues before they become large problems file fewer claims than those who defer maintenance.

Review special deductibles for your region. Check your policy declarations page for wind/hail, hurricane, earthquake, or other special deductibles. Calculate the actual dollar amounts for percentage-based deductibles. Ensure you have savings to cover the highest deductible you might face, not just your standard deductible.

A choosing deductible homeowners insurance guide must address these regional variations since they dramatically affect out-of-pocket costs during common claim types for your area.

Make your decision based on break-even analysis and comfort level. Choose the highest deductible that meets three criteria: you can pay it from savings without hardship, the break-even period is reasonable (typically under 7-8 years), and you're comfortable with the out-of-pocket risk.

Robert Hunter, Director of Insurance at the Consumer Federation of America, offers this perspective: "The deductible decision is fundamentally about self-insurance. You're betting you won't have a claim, and insurers reward that bet with lower premiums. But the bet only makes sense if you can afford to lose it. I generally recommend homeowners choose the highest deductible they can comfortably pay from liquid savings, which for most people lands between $1,500 and $2,500. This balances meaningful premium savings with manageable out-of-pocket risk."

Frequently Asked Questions About Home Insurance Deductibles

Finding Your Deductible Sweet Spot

The right home insurance deductible balances three elements: your available savings, the premium savings you'll gain, and your realistic claim probability. A $1,000 deductible works for most homeowners with moderate savings and average risk, while those with substantial emergency funds and well-maintained homes benefit from $2,000-2,500 deductibles.

Avoid the trap of choosing the lowest deductible out of fear or the highest deductible for maximum savings. Calculate the actual dollars—both what you'll save annually and what you'll owe per claim. Request quotes at multiple levels and run the break-even math. If you can go 5-7 years without a claim, higher deductibles typically win.

Review your deductible every few years, especially after major financial changes. That $500 deductible made sense when you were building savings, but now that you have a solid emergency fund, you're paying for coverage you don't need. Similarly, check for separate wind, hurricane, or earthquake deductibles that might create larger out-of-pocket costs than your standard deductible.

The homeowners who choose well are those who match their deductible to their financial reality, not to generic advice or whatever default option appeared on their quote. Calculate your numbers, understand your risks, and select the deductible that lets you sleep soundly—both from premium savings and claim preparedness.