Home insurance policy documents with calculator, model house, pen and glasses on a wooden desk

What Is a Home Insurance Premium? Understanding Costs and Payment Structures

Content

A home insurance premium is the amount you pay to maintain active coverage on your homeowners policy. This payment—whether made monthly, quarterly, or annually—keeps your financial protection in place against damage, theft, liability claims, and other covered perils. Unlike your deductible (the out-of-pocket amount you pay when filing a claim), the premium is your ongoing cost for having the policy itself.

Most homeowners focus on finding the lowest premium, but understanding what drives that number helps you make smarter coverage decisions. The premium you're quoted reflects a complex calculation based on your property's characteristics, your location's risk profile, and the coverage limits you select.

Breaking Down the Premium: Core Components That Determine Your Cost

Your total premium isn't a single line item. Insurance companies build it from several coverage components, each priced according to specific risk factors.

Dwelling coverage forms the largest portion of most premiums. This protects the physical structure of your home—walls, roof, built-in appliances, attached structures. Insurers calculate this cost based on your home's replacement value, not its market price. A 2,000-square-foot home in coastal Florida carries a higher dwelling premium than an identical house in rural Iowa because rebuilding costs and hurricane risk differ dramatically.

Personal property coverage protects your belongings—furniture, electronics, clothing, and other possessions. Standard policies typically cover 50-70% of your dwelling coverage amount for personal property. If you own high-value items like jewelry, art, or collectibles, you'll need scheduled personal property endorsements, which increase your premium proportionally.

Liability protection covers legal and medical costs if someone is injured on your property or if you accidentally damage someone else's property. Most policies start at $100,000 in liability coverage, but many homeowners opt for $300,000 or $500,000. Each increase in liability limits adds to your premium, though the incremental cost is often modest—sometimes $50-75 annually for an extra $100,000 in protection.

Author: Samantha Kessler;

Source: sixth-fleet.com

Additional living expenses (ALE) coverage pays for hotel stays, meals, and other costs if your home becomes uninhabitable due to a covered loss. This component typically represents a smaller fraction of your total premium but proves invaluable during major repairs. Policies usually cap ALE at 20-30% of your dwelling coverage.

The premium structure homeowners insurance policies follow combines these components into a single price, though your declarations page should itemize each coverage type. Some insurers offer à la carte pricing where you can adjust individual coverage limits; others bundle components into tiered packages (basic, standard, premium).

How Insurance Companies Calculate Your Homeowners Premium

Insurance underwriters use sophisticated models to predict claim likelihood and severity. Your premium reflects their assessment of how much risk you bring to their pool of policyholders.

Risk Assessment Factors Insurers Evaluate

Location dominates the calculation. Homes in wildfire zones, flood plains, or hurricane-prone coastal areas face substantially higher premiums. Even within the same ZIP code, micro-location matters—properties near fire hydrants or fire stations often receive discounts, while homes farther from emergency services pay more.

Home age and construction type directly impact replacement costs and claim frequency. A 1920s home with knob-and-tube wiring and cast-iron plumbing presents higher electrical fire and water damage risks than a 2020 build with modern systems. Brick and concrete homes typically cost less to insure than wood-frame structures in areas prone to wildfires or high winds.

Claims history follows you. Insurance companies check the Comprehensive Loss Underwriting Exchange (CLUE) database, which tracks claims for seven years. Two claims in three years—even small ones—can trigger premium increases of 20-40%. Some insurers drop customers after three claims in five years, regardless of fault.

Credit-based insurance scores influence premiums in most states. Insurers have found statistical correlations between credit behavior and claim frequency. A poor credit score can increase your premium by 50-100% compared to someone with excellent credit buying identical coverage. This practice remains controversial, and a few states (California, Massachusetts, Hawaii) prohibit using credit scores in homeowners insurance pricing.

Author: Samantha Kessler;

Source: sixth-fleet.com

Coverage limits and endorsements create a direct mathematical relationship with premium calculation homeowners insurance basics. Double your dwelling coverage from $250,000 to $500,000, and your premium increases proportionally—though not always exactly double due to economies of scale in the insurer's risk pool.

The Role of Deductibles in Premium Pricing

Your deductible functions as an inverse lever on your premium. Choose a $500 deductible, and you'll pay a higher annual premium than if you selected a $2,500 deductible—often 15-30% more. The trade-off is straightforward: pay more upfront in premiums for lower out-of-pocket costs when filing claims, or accept higher claim costs in exchange for lower ongoing premiums.

Many homeowners default to the lowest deductible without calculating the break-even point. If raising your deductible from $1,000 to $2,500 saves $300 annually, you'd need five years without a claim to offset the extra $1,500 you'd pay out-of-pocket. For homeowners with emergency savings, higher deductibles often make financial sense.

The most important thing to do if you find yourself in a hole is to stop digging. In insurance, that means understanding your true cost of risk before choosing the cheapest option that leaves you exposed when disaster actually strikes.

— Warren Buffett

Some policies use percentage deductibles for specific perils—commonly wind and hail in coastal states. A 2% wind deductible on a $300,000 dwelling means you'd pay the first $6,000 of wind damage repairs. These percentage deductibles significantly reduce premiums in high-risk areas but can create sticker shock during claims.

Premium Payment Structures: Annual vs. Monthly Plans

How you pay your premium affects both convenience and total cost. Most insurers offer multiple payment schedules, each with distinct advantages and potential fees.

| Payment Structure | Total Annual Cost | Convenience | Fees/Interest | Best For |

| Annual Lump Sum | Lowest (baseline) | Pay once and forget | None | Homeowners with cash reserves who want to minimize total cost |

| Monthly Installments | 3-8% higher | Budget-friendly; spreads cost | $3-10/month service fee or interest charges | Those prioritizing cash flow over total cost |

| Escrow Payments | Same as annual (if paid by lender) | Automatic; bundled with mortgage | None (built into mortgage payment) | Mortgaged homeowners who prefer automated payments |

| Quarterly Payments | 2-5% higher | Balance of convenience and cost | $5-8/quarter service fee | Homeowners who want fewer transactions than monthly but can't pay annually |

Annual payment delivers the best value. You avoid installment fees and sometimes qualify for a "paid-in-full" discount of 5-10%. The downside: a lump-sum payment of $1,500-3,000+ strains budgets for many households.

Monthly installment plans align with how most people manage expenses, but insurers treat this as extending credit. Some add flat service fees ($5-10 per payment), while others apply interest (typically 6-10% APR). A $1,200 annual premium might cost $1,296 when paid monthly—$8/month in fees.

Escrow arrangements work differently. If you have a mortgage, your lender may require insurance payments through escrow, bundling them with your monthly mortgage payment. The lender pays your annual premium directly to the insurer, and you reimburse them monthly with no additional fees. This autopilot approach prevents coverage lapses but gives you less direct control over policy shopping and changes.

The premium meaning homeowners insurance policies carry in escrow arrangements can confuse new homeowners. You're still paying the premium—it's just collected and disbursed by your mortgage servicer rather than paid directly to the insurance company.

Common Factors That Increase or Decrease Your Premium

Certain actions directly impact what you pay, while others create indirect effects through risk profile changes.

Security and mitigation improvements earn discounts at most insurers. Installing a monitored burglar alarm typically reduces premiums 5-10%. Fire sprinkler systems, wind-resistant roofing, and impact-resistant windows can lower premiums 10-25% in high-risk areas. A new roof often qualifies for discounts of 10-20%, though this varies by insurer and region.

One common mistake: assuming all upgrades automatically reduce premiums. You must notify your insurer and provide documentation. Many homeowners replace their roof and continue paying higher premiums for years simply because they never informed their insurance company.

Bundling policies with the same insurer creates multi-policy discounts of 15-25%. Combining home and auto insurance is the most common bundle, but umbrella policies, boat insurance, and other coverage types also qualify. The discount applies to both policies, creating compounding savings.

Claims-free discounts reward customers who don't file claims. After three to five years without a claim, many insurers reduce premiums by 10-20%. This creates a perverse incentive to avoid filing small claims—if your $2,000 water damage repair would trigger a premium increase of $300/year for three years, you've paid $900 in higher premiums plus lost your claims-free discount.

Policy shopping remains the most effective premium reduction strategy. Insurance companies adjust their risk models and pricing strategies constantly. The insurer offering the best rate five years ago may now be 30-40% higher than competitors. Shopping every two to three years—or whenever your premium increases significantly—often uncovers savings of $400-800 annually for identical coverage.

An ounce of prevention is worth a pound of cure. Homeowners who invest time comparing policies and understanding their coverage options consistently pay less while maintaining stronger financial protection against the unexpected.

— Benjamin Franklin

Home improvements that increase your home's value require coverage adjustments, which raise premiums. Adding a $50,000 addition to your home means increasing your dwelling coverage by $50,000, which proportionally increases that component of your premium. Failing to update coverage leaves you underinsured, while updating it raises costs—a catch-22 many homeowners don't anticipate.

According to Robert Hunter, Director of Insurance at the Consumer Federation of America, "Homeowners often focus exclusively on premium costs while ignoring coverage adequacy. The cheapest policy becomes the most expensive if it leaves you underinsured during a major loss. The goal isn't the lowest premium—it's the best value for comprehensive protection."

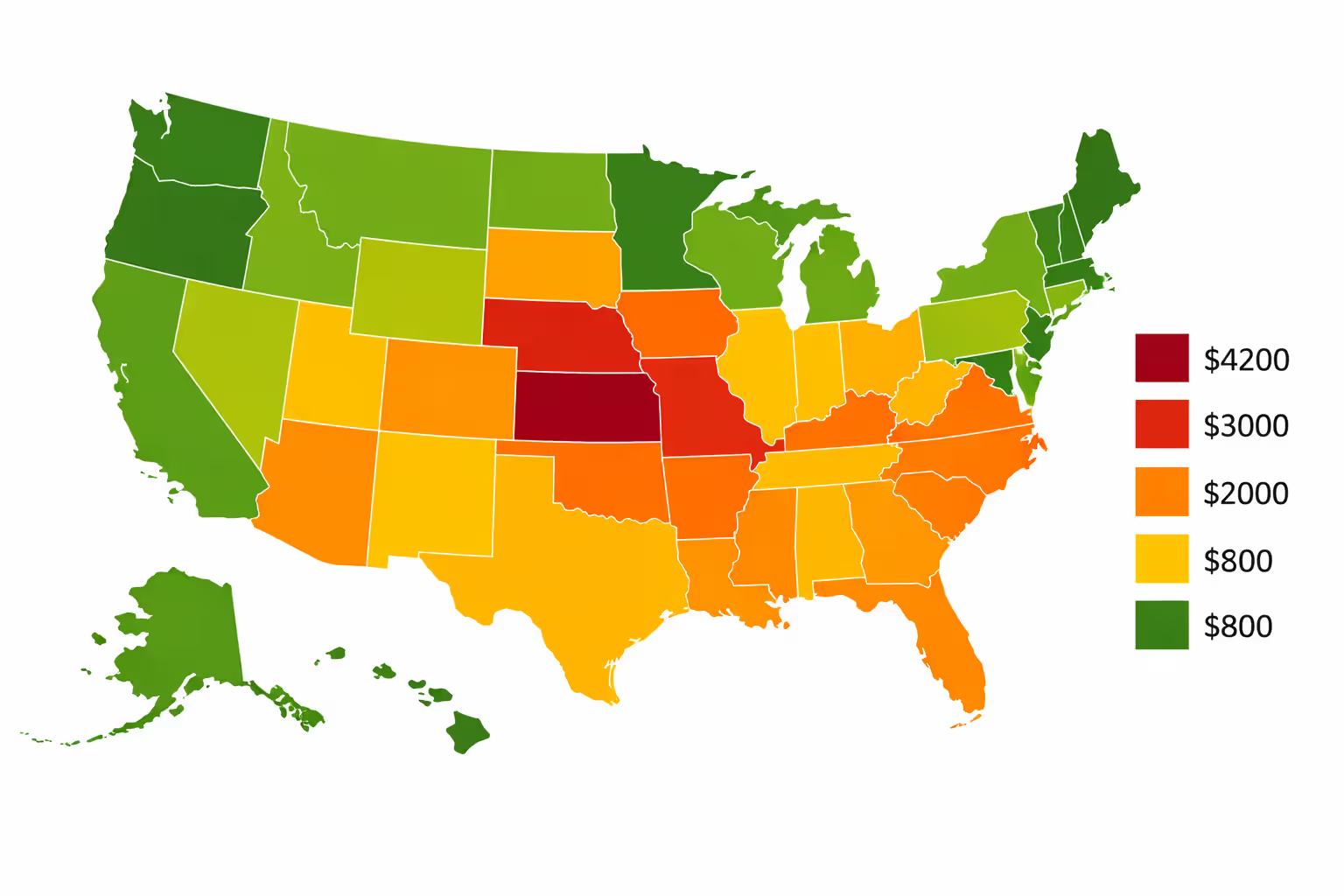

Average Home Insurance Premiums Across the U.S.

National averages provide context, but state-level and local variations matter more for individual homeowners. The national average annual premium hovers around $1,400-1,700, but this figure masks dramatic regional differences.

| State | Average Annual Premium | Primary Risk Factors |

| Oklahoma | $4,200 | Tornadoes, hail, wind damage |

| Nebraska | $3,800 | Severe storms, hail |

| Kansas | $3,500 | Tornado alley, wind events |

| Florida | $3,200 | Hurricanes, flooding, wind |

| Texas | $3,100 | Hail, wind, coastal hurricanes |

| Colorado | $2,600 | Hail, wildfire risk |

| Louisiana | $2,500 | Hurricanes, flooding |

| Alabama | $2,200 | Tornadoes, hurricanes |

| Georgia | $1,800 | Wind, some coastal risk |

| California | $1,400 | Wildfire, earthquake (separate coverage) |

| New York | $1,300 | Coastal storms, winter weather |

| Pennsylvania | $1,100 | Moderate risk profile |

| Wisconsin | $1,000 | Winter weather, moderate risk |

| Oregon | $900 | Lower overall risk |

| Utah | $800 | Lower risk, stable weather |

Oklahoma, Nebraska, and Kansas consistently rank as the most expensive states due to severe convective storms that produce massive hail and tornadoes. A single hailstorm can generate hundreds of millions in claims across a region, driving up premiums for all homeowners.

Florida's high premiums stem from hurricane exposure and a troubled insurance market where several major carriers have exited the state. Many Florida homeowners now rely on Citizens Property Insurance Corporation, the state-backed insurer of last resort, which has raised rates repeatedly.

California presents an anomaly—moderate premiums despite extreme wildfire risk. This reflects heavy state regulation of insurance pricing and many insurers' decisions to stop writing new policies rather than charge actuarially justified premiums. Homeowners in high-risk areas increasingly struggle to find coverage at any price.

Author: Samantha Kessler;

Source: sixth-fleet.com

Understanding what is a home insurance premium in your specific state requires looking beyond averages. Within Texas, coastal Houston homeowners pay vastly more than those in inland San Antonio. ZIP code-level data provides better guidance than state averages.

Frequently Asked Questions About Home Insurance Premiums

Understanding your homeowners insurance premium transforms it from a mysterious monthly expense into a manageable cost you can optimize. The premium components homeowners insurance policies include—dwelling, liability, personal property, and additional living expenses—each respond to different risk factors and coverage decisions.

Your premium reflects dozens of variables: location risks, home characteristics, coverage choices, deductible levels, and personal factors like claims history and credit score. While you can't change your home's location or age, you control many premium drivers through security improvements, policy bundling, deductible selection, and regular comparison shopping.

The payment structure you choose—annual, monthly, or escrow—affects total cost and convenience. Annual payment minimizes fees, while monthly installments ease cash flow at a modest premium. For mortgaged homes, escrow arrangements provide autopilot simplicity.

Rather than fixating on finding the absolute lowest premium, focus on value: adequate coverage at a competitive price. An underpriced policy that leaves you underinsured after a major loss is far more expensive than a slightly higher premium that provides comprehensive protection. Review your coverage annually, shop rates every two to three years, and adjust your policy as your home and financial situation evolve. This approach ensures your premium delivers genuine protection rather than just checking a box.