Mortgage documents, home insurance policy, calculator, and small house model on a desk

Do I Have to Pay Homeowners Insurance Through Escrow?

Content

Whether you must pay homeowners insurance through an escrow account depends primarily on your loan type, down payment size, and lender policies. Most borrowers with less than 20% equity face mandatory escrow requirements, while those with substantial equity may negotiate direct payment arrangements. Understanding these rules helps you plan your finances and potentially save money on insurance premiums.

When Lenders Require Escrow for Homeowners Insurance

Lenders protect their collateral by ensuring property insurance remains current. When you default on insurance payments, the property becomes vulnerable to uninsured losses, jeopardizing the lender's security interest. This explains why escrow requirements homeowners insurance mortgage contracts often mandate aren't arbitrary—they're risk management tools.

FHA, VA, and USDA Loan Requirements

Federal loan programs impose strict mandatory escrow homeowners insurance policies without exception. FHA loans require escrow accounts for the entire loan term, regardless of equity position. You cannot waive this requirement even after building substantial equity or maintaining perfect payment history.

VA loans follow similar rules. The Department of Veterans Affairs mandates escrow accounts for property taxes and insurance premiums on all VA-backed mortgages. Veterans cannot opt out during the initial loan term, though refinancing into a conventional loan may provide exit options.

USDA rural development loans also require permanent escrow arrangements. Since these programs target lower-income borrowers with zero down payment options, the escrow mandate protects both the borrower and the government guarantee.

Author: Lauren Bishop;

Source: sixth-fleet.com

Conventional Loan Thresholds (LTV Ratios)

Conventional mortgages offer more flexibility, but most lenders still require escrow when your loan-to-value ratio exceeds 80%. If you put down less than 20%, expect mandatory escrow for insurance and taxes. This threshold exists because higher LTV ratios represent greater lender risk.

Some lenders set even stricter triggers. A borrower with 15% down might face escrow requirements until reaching 25% equity. Investment properties typically face harsher standards—many lenders require escrow regardless of down payment size for non-owner-occupied properties.

Credit score intersects with LTV requirements. Borrowers with scores below 700 may find lenders unwilling to waive escrow even at 80% LTV. Conversely, excellent credit combined with 25% down payment often unlocks waiver eligibility with minimal resistance.

Lenders view escrow accounts as protection against lapses in insurance coverage that could leave their collateral exposed. Borrowers with strong equity positions and solid payment histories represent lower risk, which is why conventional loans allow escrow waivers that government-backed programs don't permit

— Rachel Moreno, Senior Mortgage Broker, Pinnacle Home Lending

How Mortgage Escrow Accounts Work for Insurance Payments

Understanding the mortgage escrow homeowners insurance explanation requires following the money through several stages. Your lender collects a portion of your annual insurance premium with each monthly mortgage payment, holds these funds in a dedicated account, then disburses payment to your insurance company when premiums come due.

The math starts with your annual premium divided by twelve. If your homeowners insurance costs $1,800 yearly, your monthly escrow contribution equals $150. This amount gets added to your principal, interest, and tax payments to create your total monthly obligation.

Lenders maintain a cushion—typically two months' worth of expenses—to handle premium increases or timing mismatches. For that $1,800 annual premium, expect your escrow account to hold an extra $300 buffer. This cushion prevents shortfalls when insurance companies raise rates mid-year.

Federal escrow payment homeowners insurance rules limit cushions to one-sixth of total annual disbursements. Lenders cannot hoard excessive reserves in your escrow account. If your combined insurance and tax obligations total $4,200 annually, the maximum allowable cushion equals $700.

Annual escrow analysis occurs each year, comparing actual disbursements against collected funds. Overages trigger refunds—if your account holds $500 more than required, you'll receive a check or principal reduction. Shortages result in increased monthly payments or one-time catch-up bills.

Disbursement timing matters more than many homeowners realize. Lenders typically pay insurance premiums 30 days before the due date to prevent coverage lapses. If your policy renews June 1, expect escrow disbursement around May 1. Missing this window could temporarily leave your property uninsured, violating your mortgage agreement.

Author: Lauren Bishop;

Source: sixth-fleet.com

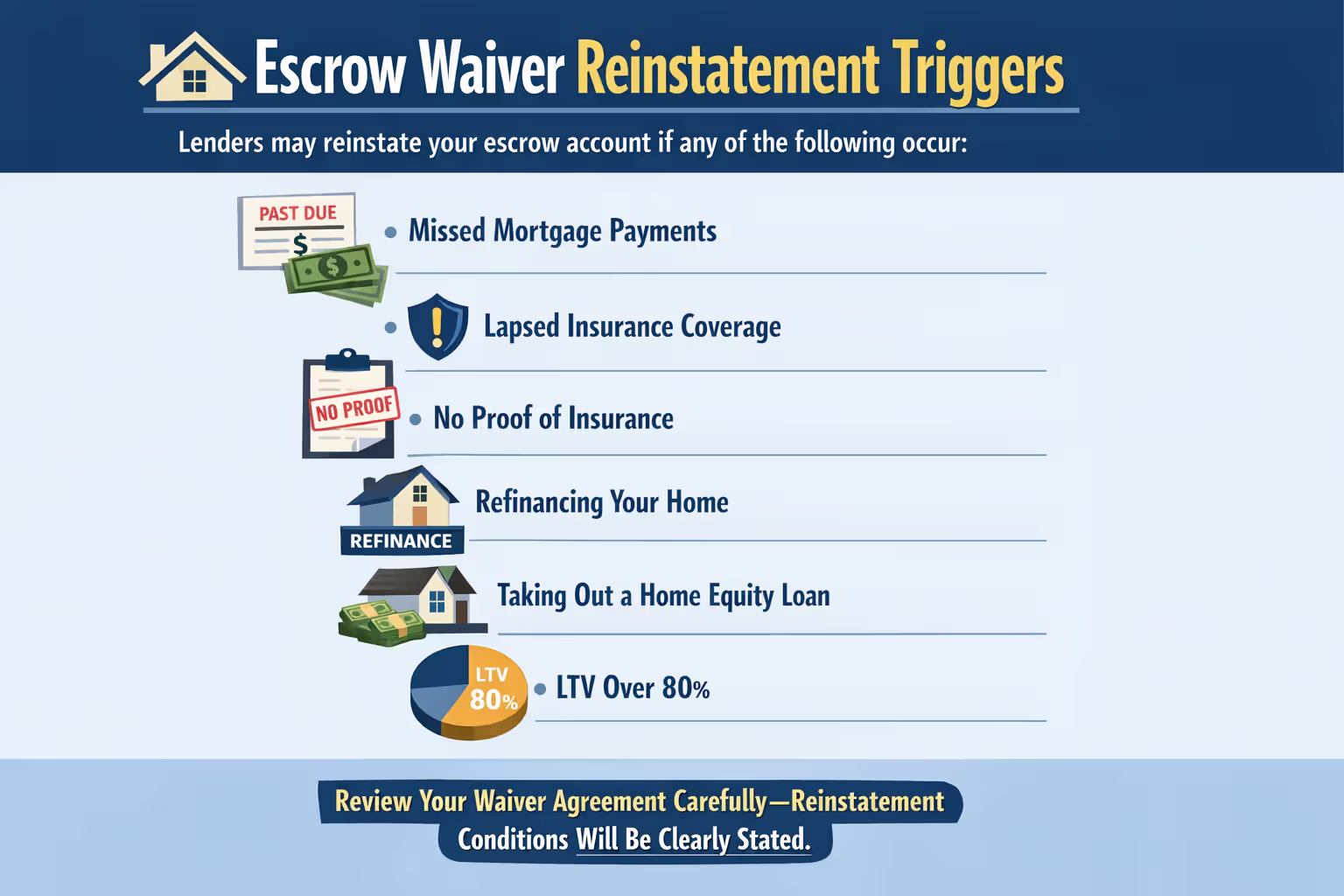

Your Rights to Remove or Waive Escrow Requirements

Federal law doesn't grant automatic escrow removal rights, but many conventional loans permit waivers under specific conditions. Your ability to escape escrow requirements homeowners insurance mortgage contracts impose depends on loan type, equity level, and lender discretion.

Qualifying Criteria for Escrow Waiver

Most conventional lenders consider escrow waivers when you reach 20% equity, though many prefer 25% before approving requests. You'll need to demonstrate consistent payment history—typically 12 months without late payments. A single 30-day delinquency in the past year usually disqualifies you.

Expect waiver fees ranging from 0.125% to 0.25% of your loan amount. On a $300,000 mortgage, that's $375 to $750 added to your loan balance or due at closing. Some lenders add 0.125% to your interest rate instead of charging upfront fees. Over a 30-year term, that rate bump costs significantly more than a one-time fee.

Documentation requirements include proof of paid-up insurance, direct payment authorization to your insurer, and sometimes proof of sufficient liquid reserves. Lenders want assurance you can handle the annual premium lump sum without financial strain. Showing three to six months of expenses in savings strengthens your waiver application.

Refinancing offers another escape route. If you've built sufficient equity, refinancing into a loan without escrow requirements eliminates the account entirely. This works particularly well for borrowers who started with FHA or VA loans but now qualify for conventional financing with 20%+ equity.

State-Specific Escrow Laws

California limits when lenders can require escrow accounts. After meeting specific equity thresholds and payment history standards, California borrowers gain stronger removal rights than federal law provides. Lenders cannot arbitrarily deny escrow cancellation requests from qualified borrowers.

Texas law requires lenders to offer escrow waivers at closing for borrowers meeting minimum down payment requirements, though lenders may charge fees for this privilege. Texas borrowers should review their loan estimate carefully—the escrow waiver option must be disclosed if available.

New York imposes strict escrow accounting rules that benefit borrowers. Lenders must pay interest on escrow balances, and annual statements must meet detailed disclosure requirements. While this doesn't eliminate escrow requirements, it provides more favorable terms than many states offer.

Several states prohibit escrow waiver fees entirely or cap them at specific amounts. Research your state's regulations before accepting your lender's first offer. What seems like a non-negotiable requirement may actually be optional under state law.

Author: Lauren Bishop;

Source: sixth-fleet.com

Pros and Cons of Paying Insurance Through Escrow vs. Directly

The escrow payment insurance homeowners guide comparison reveals distinct advantages and disadvantages to each approach. Your optimal choice depends on financial discipline, cash flow preferences, and potential premium discounts.

| Factor | Escrow Payment | Direct Payment |

| Payment Convenience | Automatic monthly installments bundled with mortgage | Requires manual annual or semi-annual payment |

| Annual Premium Discounts | Not available (insurers don't discount escrowed policies) | Often 5-10% discount for paying annually in full |

| Cash Flow Control | Spreads cost across 12 months; predictable budgeting | Large lump sum due; requires planning and savings |

| Risk of Missed Payments | Virtually eliminated; lender handles disbursement | Entirely your responsibility; late payment voids coverage |

| Lender Requirements | Mandatory for most loans under 80% LTV | Only available with 20%+ equity and lender approval |

| Upfront Costs | Initial escrow funding at closing (2-3 months) | Full annual premium due at policy inception |

| Account Management Fees | None (lenders cannot charge escrow servicing fees) | No account fees, but waiver may cost 0.125-0.25% |

The discount question deserves special attention. Many insurance carriers offer 5-8% discounts for annual lump-sum payments. On a $2,000 premium, that's $100-160 in annual savings. Over a 30-year mortgage, this compounds to $3,000-4,800 in total savings, assuming stable rates.

However, these savings evaporate if you miss a payment deadline. A single lapsed payment can result in policy cancellation, forced-place insurance at triple the cost, and potential mortgage default notices. The convenience of escrow often outweighs modest premium savings for borrowers who struggle with large periodic expenses.

Cash flow considerations cut both ways. Monthly escrow payments ease budgeting by eliminating surprise annual bills. But they also tie up funds that could earn interest or investment returns. A disciplined borrower who saves $167 monthly in a high-yield savings account paying 4% accumulates $2,040 after one year—$40 more than needed for a $2,000 premium.

What Happens If Your Escrow Account Has a Shortage or Surplus

Escrow analysis results arrive annually, typically 30-45 days before your mortgage anniversary date. These statements reconcile collected funds against actual disbursements, revealing whether your account ran surplus or deficit.

Author: Lauren Bishop;

Source: sixth-fleet.com

Shortages occur when insurance premiums or property taxes increase beyond projections. If your insurer raises your annual premium from $1,800 to $2,100, but your monthly escrow contribution remained at $150, you've collected only $1,800 while needing $2,100. The $300 gap creates a shortage.

Lenders handle shortages two ways. They'll increase your monthly payment to cover the new premium amount plus spread the shortage over 12 months. In this example, your new monthly escrow payment becomes $200 (the new premium divided by 12) plus $25 (the $300 shortage divided by 12), totaling $225 monthly—a $75 increase.

Alternatively, you can pay the shortage as a lump sum. Writing a $300 check eliminates the deficit immediately, keeping your monthly payment increase limited to the $50 needed for the higher premium. This option works well if you have available cash and want to minimize payment shock.

Surpluses happen when premiums decrease or lenders over-collected based on conservative estimates. Federal mortgage escrow homeowners insurance explanation rules require refunds when your balance exceeds the allowed cushion by $50 or more. Smaller overages typically get credited to your account, reducing next year's required contributions.

Most borrowers receive surplus refunds as checks, though you can request application to your loan principal. The principal reduction option saves interest over your loan's life but provides no immediate cash benefit. A $400 surplus applied to principal on a $250,000 loan at 6% saves approximately $14 in interest over 30 years—minimal impact.

Payment shock represents the real challenge. A $100 monthly mortgage increase strains budgets built around predictable housing costs. Monitor your insurance premiums throughout the year. When you receive renewal notices showing significant increases, contact your lender immediately to understand how this affects your escrow account and monthly payment.

Homeowners often underestimate the impact of insurance premium increases on their monthly mortgage payments. A well-managed escrow account acts as a financial buffer, but only if you stay informed about your policy costs and communicate proactively with your lender when changes occur. The biggest risk isn’t the escrow system itself — it’s complacency

— David Harrington

Common Mistakes Homeowners Make with Escrow Insurance Payments

Assuming escrow guarantees current coverage ranks among the most dangerous errors. While lenders disburse payments on schedule, they don't verify your policy remains in force. If your insurance company cancels coverage for non-payment of a separate bill or policy violation, your escrow account keeps functioning normally—but you're uninsured.

Review your annual escrow statement carefully instead of filing it away. These documents detail every disbursement and collection. Spotting errors early prevents compounding problems. One homeowner discovered their lender had been paying the wrong insurance company for three years, leaving their actual policy cancelled for non-payment while escrow funds vanished into another carrier's account.

Failing to update insurance information after switching carriers creates disbursement chaos. Your lender needs 30-60 days' notice before policy changes. Switching insurers without notifying your mortgage servicer results in payments to your old carrier, coverage lapses with your new one, and forced-place insurance at exorbitant rates.

Ignoring direct payment deadlines after escrow waiver approval leads to immediate mortgage violations. You've assumed responsibility for timely premium payment. Missing your renewal date by even one day can trigger lender notifications, forced-place insurance, and potential default proceedings. Set calendar reminders 60 days before renewal, then again at 30 days.

Neglecting to shop insurance rates because "escrow handles it" costs hundreds annually. Your lender doesn't care whether you're overpaying—they just ensure someone gets paid. Review your coverage every two years. Switching carriers for better rates requires coordination with your lender, but the process is straightforward and can save 15-30% on premiums.

Misunderstanding the escrow cushion causes confusion when your account balance seems high. That $2,500 sitting in escrow isn't "your money" available for withdrawal—it's reserved for upcoming disbursements plus the required buffer. Demanding refunds of legitimately held cushion amounts wastes time and reveals misunderstanding of escrow mechanics.

The freedom to pay your own insurance premiums comes with real responsibility. I’ve seen disciplined borrowers save thousands over the life of their mortgage by waiving escrow and capturing annual payment discounts. But I’ve also seen homeowners lose coverage entirely because they forgot a single renewal date. Know yourself before you choose

— Linda Castellano

Frequently Asked Questions About Escrow and Homeowners Insurance

Making the Right Choice for Your Situation

Deciding whether to pay homeowners insurance through escrow or directly requires honest assessment of your financial habits and loan terms. Borrowers with government-backed loans face mandatory escrow regardless of preferences, making the decision automatic. Those with conventional financing and sufficient equity must weigh convenience against potential savings.

Escrow provides foolproof payment certainty. Your insurance gets paid on time without effort, eliminating coverage lapse risks that could jeopardize your home and mortgage standing. The monthly installment approach smooths cash flow, preventing the budget shock of annual lump-sum premiums. For borrowers who struggle with large periodic expenses or prefer automated financial management, escrow offers genuine value beyond lender requirements.

Direct payment rewards discipline with tangible savings. The 5-10% paid-in-full discounts most insurers offer add up over time, potentially saving thousands across your mortgage term. You maintain control over timing and can more easily switch carriers for better rates. This approach works best for financially organized homeowners with stable income and sufficient savings to handle annual premium bills without strain.

Your equity position often makes the choice for you. Below 20% down, most conventional lenders require escrow regardless of your preferences. Between 20-25% equity, you'll likely need strong credit and perfect payment history to qualify for waivers. Above 25% equity, most lenders readily approve escrow removal for qualified borrowers, though waiver fees may apply.

Consider your insurance shopping habits. If you review coverage and compare rates every few years, direct payment provides flexibility to switch carriers mid-term without coordinating through your lender. If you've held the same policy for a decade without shopping around, escrow's automation probably serves you better than direct payment's flexibility.

The right answer differs for each homeowner. Calculate potential discount savings, assess your payment discipline honestly, and understand your loan's specific requirements. Whether you pay through escrow or directly, maintaining continuous coverage protects your largest asset and keeps your mortgage in good standing.