A modern American house with floating price tags showing $1,000 and $10,000 annual insurance costs, over a US risk map background

What Is the Average Price of Homeowners Insurance in 2024?

Content

If you've opened your insurance bill lately and felt your stomach drop, you're not alone. Most American homeowners now pay around $2,377 per year for coverage—but that's just an average. Depending on your zip code and the value of your property, you might be paying under $1,000 or well over $5,000 annually for similar protection.

Here's what really matters: dozens of variables affect your final premium. Where you live matters most, but insurers also weigh your home's age, your credit history, what you're actually protecting, and whether you've filed claims recently. This creates wild price swings across the country.

The pricing gap between states has grown shockingly wide. Florida homeowners in hurricane zones might pay eight times what Vermont residents pay for the same coverage amount. Wildfire-prone California neighborhoods and tornado-heavy Oklahoma counties have watched their bills triple since 2019. Other states? Their rates have barely budged.

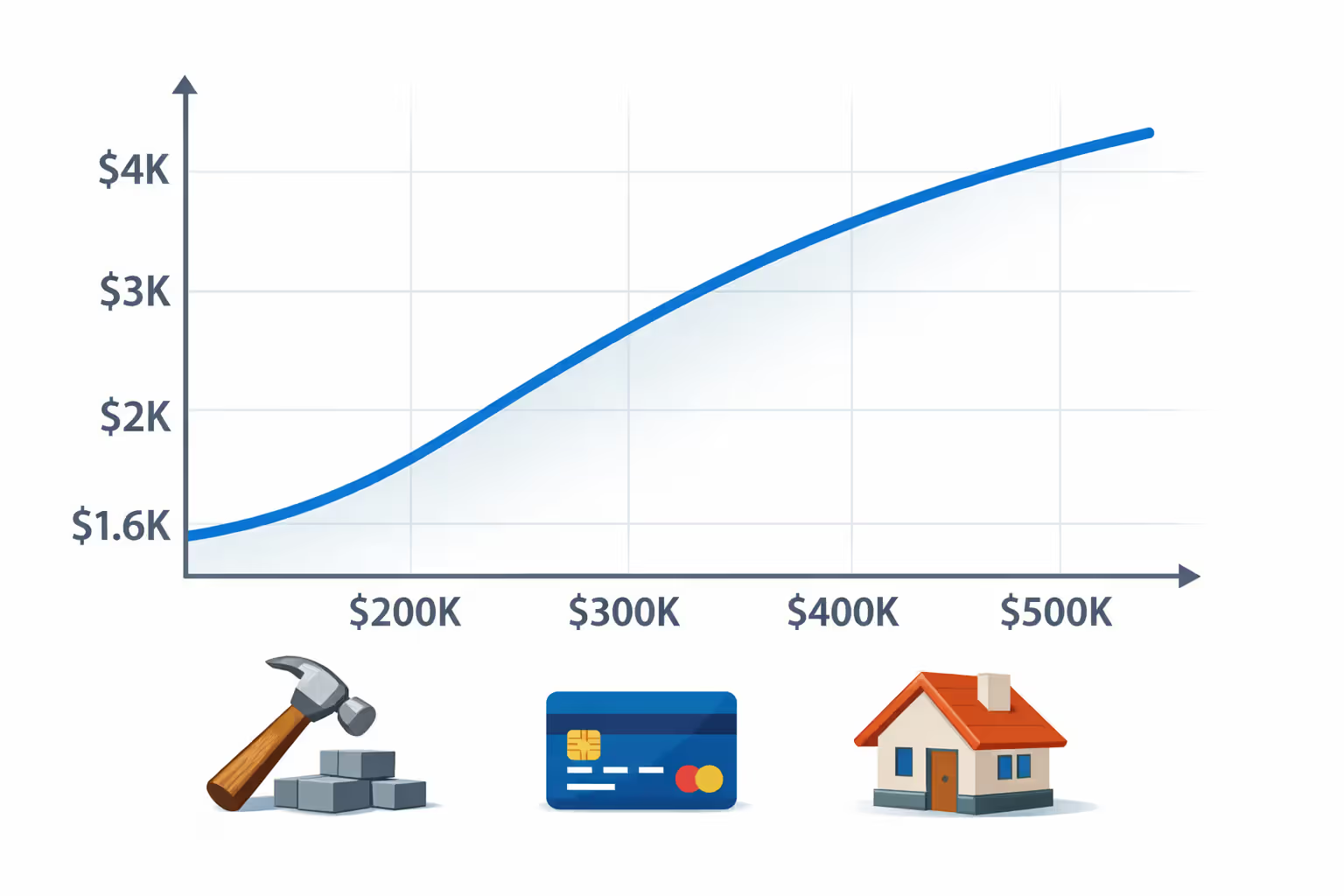

National Average Homeowners Insurance Costs by Coverage Amount

Your dwelling coverage limit—the amount your insurer would pay to rebuild your house—heavily influences your annual bill. But here's something that catches people off guard: doubling your coverage doesn't double your premium.

| Dwelling Coverage Amount | National Average Annual Premium | Average Monthly Cost |

| $200,000 | $1,678 | $140 |

| $250,000 | $1,987 | $166 |

| $300,000 | $2,377 | $198 |

| $400,000 | $3,156 | $263 |

| $500,000 | $3,945 | $329 |

These numbers assume you've chosen a $1,000 deductible and standard liability limits between $100,000 and $300,000. Your actual quote will differ based on dozens of other factors.

Notice how the premium jumps work? A $300,000 policy costs about 42% more than $200,000 coverage—not 50% more, as you might expect. Insurance companies build much of their administrative cost and risk assessment into the base premium. Processing paperwork, underwriting the policy, and maintaining customer service systems cost roughly the same whether they're insuring a $150,000 cottage or a $400,000 home.

Here's a crucial distinction many homeowners miss: your coverage should reflect rebuilding costs, not your home's real estate market value. That $400,000 house in a trendy urban neighborhood might only need $280,000 in dwelling coverage if construction costs run lower in your region. Meanwhile, a custom-built home in a less expensive area could require $450,000 to reconstruct even if it would only sell for $350,000.

Author: Ethan Caldwell;

Source: sixth-fleet.com

How Homeowners Insurance Premiums Vary by State

Where you bought your house dramatically impacts what you'll pay to insure it. State-level premium differences often exceed 400%, driven by weather patterns, local building costs, how courts handle liability cases, and state insurance regulations.

Top 10 Most Expensive States for Home Insurance

Florida dominates this unfortunate list. Coastal county residents routinely face annual premiums topping $10,000—sometimes $15,000—for standard coverage. Oklahoma and Nebraska claim second and third place thanks to relentless hail storms and severe weather. Louisiana battles hurricane exposure combined with widespread property damage from past storms. Texas has seen explosive premium growth following the 2021 freeze disaster and increasingly destructive wind events.

| State | Average Annual Premium | % Above National Average |

| Florida | $10,996 | +363% |

| Oklahoma | $5,317 | +124% |

| Nebraska | $4,926 | +107% |

| Louisiana | $4,732 | +99% |

| Texas | $4,456 | +87% |

| Kansas | $4,312 | +81% |

| Colorado | $4,198 | +77% |

| Mississippi | $3,784 | +59% |

| South Dakota | $3,621 | +52% |

| Alabama | $3,544 | +49% |

Insurance companies have abandoned entire markets in several of these states. When major carriers decide a region is too risky and pull out, homeowners face fewer choices and steeper prices. Many wind up in state-sponsored "insurers of last resort" programs that charge even higher premiums while providing more limited coverage options.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Top 10 Most Affordable States for Home Insurance

Vermont takes the crown for lowest average premiums, followed closely by Hawaii and Delaware. Annual rates in these states typically stay below $1,500. They share common advantages: infrequent natural disasters, predictable weather, and relatively stable insurance markets.

| State | Average Annual Premium | % Below National Average |

| Vermont | $1,023 | -57% |

| Hawaii | $1,087 | -54% |

| Delaware | $1,154 | -51% |

| Utah | $1,198 | -50% |

| New Hampshire | $1,243 | -48% |

| Oregon | $1,312 | -45% |

| Wisconsin | $1,356 | -43% |

| Pennsylvania | $1,398 | -41% |

| Maine | $1,432 | -40% |

| Virginia | $1,467 | -38% |

Don't assume cheap automatically means better. Vermont's rock-bottom premiums reflect its small, spread-out population and minimal hurricane or tornado exposure. But homeowners there still need solid protection against harsh winters—think ice dams, frozen pipe bursts, and heavy snow loads on roofs. The premiums might be low, but the risks haven't disappeared.

7 Factors That Determine Your Homeowners Insurance Premium

Knowing what insurance companies actually evaluate gives you leverage to lower your costs and predict what you'll pay.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Location and Natural Disaster Risk: How close you live to the ocean, a flood zone, an earthquake fault, or wildfire-prone terrain directly shapes your rate. Two houses three miles apart might have wildly different premiums because one sits 200 feet higher in elevation or has better access to fire hydrants. Modern insurers use satellite imagery and advanced modeling to assess individual properties, not just general neighborhoods.

Home Age and Construction Type: That charming 1955 ranch probably costs more to insure than the bland 2020 subdivision house next door. Why? Original electrical panels, galvanized steel plumbing, and aging roofing materials create higher fire and water damage risks. Interestingly, wood-frame houses often cost less to insure than brick structures—not because they're stronger (they're not), but because repairs run cheaper.

Credit-Based Insurance Score: About 85% of states let insurers check your credit when pricing policies. Research shows people with lower credit scores statistically file more claims. Fair or not, a 580 credit score might inflate your premium by 40% compared to someone with a 780 score, everything else identical.

Claims History: File two or three claims within five years and watch your rates jump—even for claims where you weren't at fault. Insurance companies interpret frequent claims as a red flag suggesting property maintenance problems. One $15,000 claim might barely affect your rate. Three $3,000 claims? That could trigger a 30% increase.

Deductible Selection: Switch from a $500 deductible to $2,500 and you could slash your premium by 30% or more. You're essentially telling the insurer, "I'll handle anything under $2,500 myself," which dramatically reduces their exposure. Most financial advisors recommend carrying the highest deductible you could pay from savings without stress.

Coverage Limits and Policy Features: Your liability limits matter as much as dwelling coverage. Bump liability from $100,000 to $500,000 and you'll see a moderate premium increase. Add scheduled coverage for jewelry, purchase separate earthquake or flood policies, or include equipment breakdown coverage—each addition increases your total cost.

Home Security and Safety Features: Monitored burglar alarms, fire sprinkler systems, impact-resistant windows, and modern storm shutters can trim 5% to 25% off your premium. Exact discounts vary wildly between insurance companies. Some carriers now offer substantial breaks—15% to 20%—for comprehensive smart home systems that detect leaks, monitor for smoke, and alert you to break-ins via smartphone.

The single biggest factor driving premium increases right now is the rising cost of rebuilding homes. Labor shortages and supply chain disruptions have pushed construction costs up 30% to 40% in many markets since 2020. When it costs more to rebuild, insurers must charge higher premiums to maintain adequate reserves for future claims.

— Robert Hunter

Breaking Down What Your Premium Actually Covers

Most homeowners don't know exactly what they're paying for until disaster strikes and they file their first major claim. Standard policies bundle several distinct protections.

Dwelling Coverage (Coverage A): This covers your home's structure—walls, roof, built-in appliances, attached garage. It's usually your policy's largest component. Insurers calculate this number based on estimated reconstruction costs using local labor and material prices, completely separate from what your home would sell for.

Other Structures (Coverage B): Detached buildings like garages, sheds, workshops, fences, and driveways get their own category, typically set at 10% of dwelling coverage automatically. If you've got a substantial detached guest house or large workshop, that standard 10% probably won't cut it—you'll need to increase this limit.

Personal Property (Coverage C): Everything you own that isn't permanently attached to the structure—furniture, electronics, clothing, kitchenware. Standard policies set this at 50% to 70% of your dwelling coverage. Watch out for sublimits on specific categories: most policies cap jewelry at $2,000, meaning that $8,000 engagement ring needs separate scheduled coverage.

Loss of Use (Coverage D): When fire, storm damage, or another covered disaster makes your house unlivable, this pays hotel bills, restaurant meals, and other extra costs while you're displaced. Typically set at 20% to 30% of dwelling coverage, it continues until repairs finish or you hit the dollar limit.

Personal Liability (Coverage E): Legal protection when someone gets hurt on your property or when you accidentally damage someone else's stuff. Most policies start at $100,000, but that's frankly inadequate in today's lawsuit-happy environment. Bump this to at least $300,000—better yet, $500,000.

Medical Payments (Coverage F): A modest amount—usually $1,000 to $5,000—that covers medical bills when guests get injured at your home, no fault determination required. This helps prevent small injuries from turning into liability lawsuits.

Your total annual premium reflects all these coverage components combined, plus the insurer's administrative overhead and profit margin. When you understand how each piece works, you can make smarter decisions about adjusting coverage to control costs.

How to Lower Your Homeowners Insurance Premium Without Sacrificing Coverage

Strategic moves can cut hundreds—sometimes thousands—off your annual premium while keeping your protection intact.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Bundle Policies: Put your home and auto insurance with one company and you'll typically save 15% to 25% on both. The discount grows if you add umbrella liability coverage or insure a second property. Some insurers sweeten the deal further when you add life insurance or have multiple vehicles.

Raise Your Deductible Strategically: Jump from $500 to $1,000 and you might save $200 yearly. Go five years without a claim? You've gained $1,000 while paying out nothing. Push that deductible to $2,500 and you could save another $300 annually. Just make sure you've got enough emergency savings to comfortably cover that higher deductible if disaster strikes.

Improve Home Resilience: Install impact-resistant roof shingles, add storm shutters, or reinforce your garage door against high winds. These upgrades earn immediate discounts—5% to 15% typically—while genuinely reducing your risk of damage. The improvements often pay for themselves through insurance savings within five to seven years, plus they boost your home's resale value.

Shop Around Every Two to Three Years: Staying with the same insurer for a decade rarely rewards you. Insurance companies constantly adjust their risk models and target markets. The carrier that gave you the best deal in 2021 might be overpriced now. Pull quotes from at least three companies every few years—include both national brands and regional carriers, which sometimes offer better rates for local properties.

Maintain Good Credit: Since most states permit credit-based pricing, improving your credit score gradually lowers your premium. Pay every bill before the due date, chip away at credit card balances, and scrub errors from your credit reports. A 100-point credit score improvement could cut your premium by 15%.

Avoid Small Claims: Filing a $1,800 claim when you carry a $1,000 deductible gets you $800 now but could cost you $300 extra per year for the next five years—you're actually losing $700 overall. Reserve insurance for genuinely catastrophic losses that would create financial hardship, not routine repairs you could handle from savings.

Review Coverage Annually: Your home's rebuilding cost changes as material and labor prices fluctuate. Maybe you've paid down your mortgage substantially and you're carrying more coverage than necessary. Or perhaps construction costs have spiked 20% in your area and you're actually underinsured now. Annual policy reviews prevent both overpaying and dangerous coverage gaps.

Ask About Lesser-Known Discounts: Insurance companies offer dozens of discounts they won't mention unless you ask. Examples: five years claim-free, age 55 or older, new home (less than 10 years old), certain professional occupations, alumni associations, professional organizations. These discounts aren't advertised prominently—you've got to inquire specifically.

Frequently Asked Questions About Homeowners Insurance Costs

Making Informed Decisions About Your Homeowners Insurance Costs

Understanding insurance pricing mechanics gives you power. The premium gap between highest and lowest-cost states will probably keep widening as climate change intensifies weather extremes and natural disasters grow more frequent and destructive.

Focus on three priorities. First, carry enough coverage to genuinely rebuild your home and replace your belongings—underinsurance creates catastrophic financial risk. Second, choose the highest deductible you can comfortably afford to pay from savings, which dramatically reduces premiums. Third, shop rates every two to three years to ensure you're getting competitive pricing from a financially stable company.

Review your entire policy annually, particularly after major life changes. Completed a kitchen renovation? Paid off your mortgage? Inherited valuable jewelry or art? What made perfect sense three years ago might be completely wrong for your current situation. Spending an hour annually reviewing coverage and exploring cost-reduction strategies can easily save $2,000 to $5,000 over a decade of homeownership.