Suburban American house with insurance shield symbol, calculator, and coin stack representing homeowners insurance cost

What Is the Average Monthly Homeowners Insurance Cost in 2024?

Content

Homeowners insurance typically costs between $125 and $250 per month for most American households, though your actual premium depends heavily on where you live and what you're insuring. Understanding these costs helps you budget accurately and identify when you're overpaying.

The national landscape for homeowners insurance has shifted dramatically over the past three years. Insurers have pulled out of high-risk markets, natural disasters have increased in frequency and severity, and inflation has driven up reconstruction costs. These forces combine to create a market where premiums can vary by 400% or more depending on your zip code.

National Average Monthly Homeowners Insurance Premium Breakdown

The average monthly homeowners premium in the US currently sits at approximately $183, translating to $2,196 annually. This figure represents the mean across all states, coverage levels, and property types—a useful benchmark but not necessarily reflective of what you'll pay.

Understanding the difference between median and mean matters here. The mean average gets skewed upward by expensive coastal states and high-value properties. The median monthly premium—the middle point where half of homeowners pay more and half pay less—comes in closer to $158 per month. If you're comparing your own costs, the median often provides a more realistic reference point for typical American homes.

Annual costs broken down monthly can be misleading. When insurers quote annual premiums divided by 12, they're not accounting for installment fees that monthly payers often face. A $2,400 annual policy might actually cost you $210 per month ($2,520 annually) when you factor in the convenience fees most insurers charge for monthly billing.

Coverage amount dramatically affects your monthly outlay. Here's how premiums scale with dwelling coverage:

| Dwelling Coverage Amount | Average Monthly Premium | Annual Equivalent |

| $200,000 | $142 | $1,704 |

| $300,000 | $183 | $2,196 |

| $500,000 | $271 | $3,252 |

| $750,000 | $396 | $4,752 |

These figures assume standard liability limits ($300,000), a $1,000 deductible, and a property in a moderate-risk area. Your actual costs will vary based on the seven factors we'll examine later.

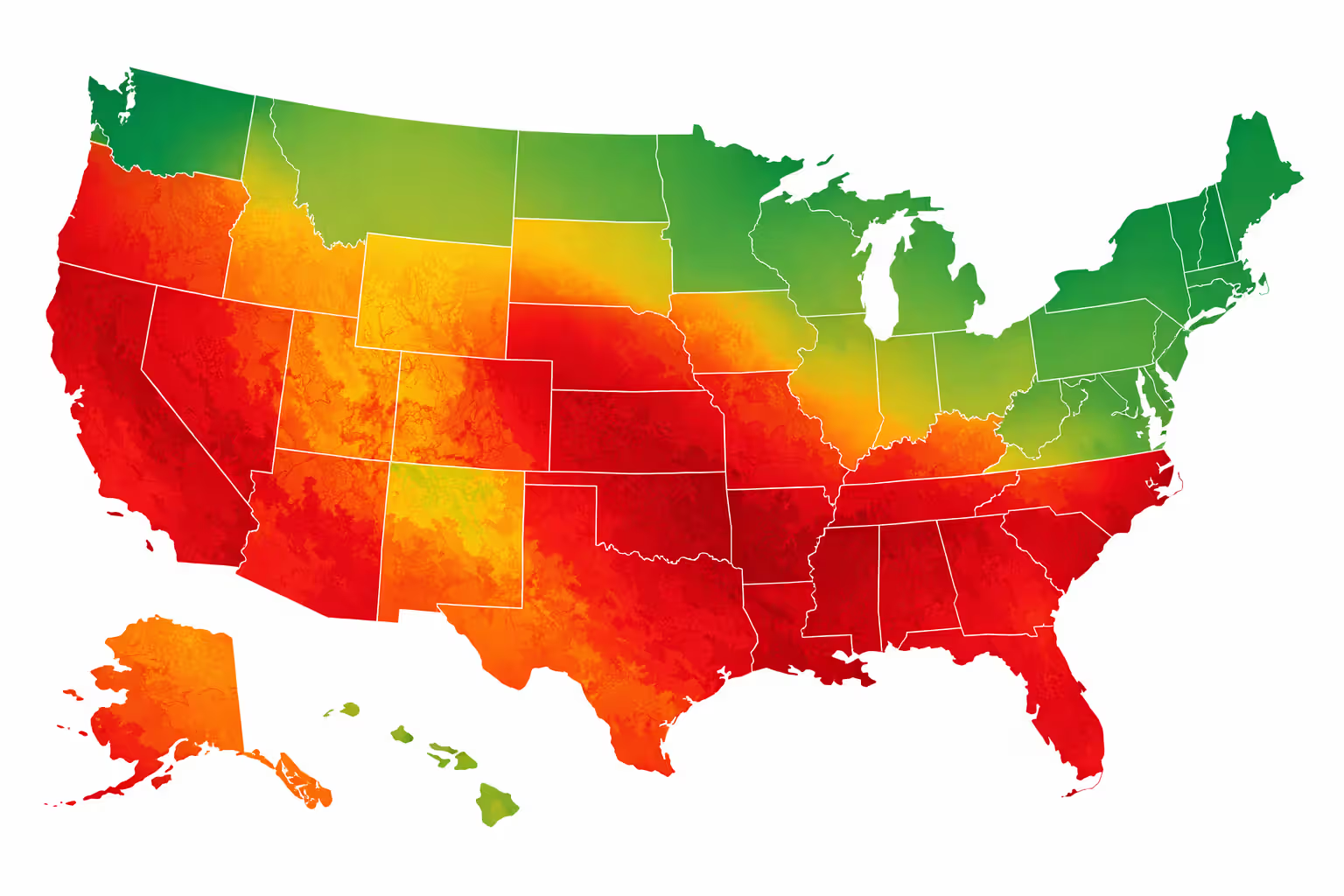

How Monthly Homeowners Insurance Costs Vary by State

State-level differences in homeowners insurance monthly averages across the US reveal stark disparities. A $300,000 home in Hawaii might cost you $29 per month to insure, while an identical property in Louisiana could run $383 monthly—more than 13 times higher.

Here's the current breakdown of monthly premiums by state:

| Most Expensive States | Avg Monthly Premium | Least Expensive States | Avg Monthly Premium |

| Nebraska | $383 | Hawaii | $29 |

| Oklahoma | $367 | Vermont | $96 |

| Kansas | $329 | New Hampshire | $104 |

| Louisiana | $321 | Delaware | $108 |

| Texas | $308 | Utah | $112 |

| Colorado | $292 | Oregon | $117 |

| Mississippi | $283 | Washington | $121 |

| Arkansas | $275 | Idaho | $125 |

| South Dakota | $267 | Maine | $129 |

| Alabama | $258 | Wisconsin | $133 |

These monthly insurance premium homeowners statistics shift annually as climate patterns evolve and insurers reassess risk models. Nebraska's top position reflects recent severe hailstorm activity, while Oklahoma and Kansas face similar weather-related challenges.

Why Coastal and Disaster-Prone States Pay More

Florida no longer appears in the top ten most expensive states by average premium, but that's misleading. Many Florida homeowners now carry bare-minimum coverage or have been dropped entirely, skewing the statistics downward. Those who maintain comprehensive coverage in coastal counties often pay $500+ monthly.

Hurricane exposure creates premium volatility that extends beyond obvious coastal zones. Properties within 100 miles of the Gulf Coast or Atlantic Ocean face wind and hail deductibles separate from standard deductibles—often 2-5% of dwelling coverage. On a $400,000 home, that's an $8,000-$20,000 out-of-pocket expense before insurance pays anything for storm damage.

Wildfire risk has pushed Western state premiums upward. California homeowners in the Wildland-Urban Interface pay 40-60% more than the state average. Some mountain communities in Colorado now face premiums exceeding $400 monthly for modest homes because insurers calculate not just fire risk but also the distance to fire stations and availability of water sources.

Tornado Alley states—Oklahoma, Kansas, Nebraska—experience frequent severe convective storms that produce baseball-sized hail. These events cause billions in claims annually, and insurers have responded by raising rates and increasing deductibles. A homeowner in Moore, Oklahoma (hit by devastating tornadoes in 1999, 2003, and 2013) might pay triple the national average regardless of personal claims history.

Author: Lauren Bishop;

Source: sixth-fleet.com

7 Factors That Determine Your Monthly Premium

1. Dwelling Coverage Amount and Replacement Cost

Your dwelling coverage should reflect the cost to rebuild your home from scratch, not its market value. A 2,000-square-foot home might sell for $350,000 in your market but cost $425,000 to rebuild due to labor and material expenses. Underinsuring to lower premiums backfires during total loss claims when you discover your coverage falls short.

2. Location Down to the Neighborhood Level

Insurers don't just evaluate by state or city—they drill down to specific neighborhoods. Two homes three miles apart can have different premiums based on fire station proximity, local crime statistics, and flood zone designation. Properties in gated communities often receive 5-10% discounts due to lower theft and vandalism rates.

3. Deductible Selection

Raising your deductible from $1,000 to $2,500 typically reduces monthly premiums by 15-25%. The math works if you have emergency savings to cover the higher deductible. A homeowner paying $200 monthly who raises their deductible might save $40 per month ($480 annually). After three claim-free years, they've banked $1,440—nearly enough to cover the higher deductible if needed.

4. Credit-Based Insurance Score

In most states, insurers use credit information to predict claim likelihood. Someone with excellent credit might pay 30-40% less than an identical homeowner with poor credit. This remains controversial, but insurers defend the practice with data showing correlation between credit behavior and claim frequency. Maryland, California, and Massachusetts have banned or limited this practice.

5. Home Age and Condition

Homes built within the past 15 years often qualify for "new home" discounts of 10-20%. Older homes face higher premiums due to outdated electrical systems, plumbing, and roofing. A 1960s home with original knob-and-tube wiring might be uninsurable until updated. Roof age particularly matters—many insurers now require replacement if shingles exceed 15-20 years, regardless of condition.

6. Claims History

Filing even one claim can increase your premiums by 20-30% and remain on your record for 3-7 years. Two claims within five years might result in non-renewal. This creates a difficult calculation: file a $3,500 claim and potentially face $800 in annual premium increases for five years ($4,000 total), or pay out of pocket? Many homeowners now treat insurance as catastrophic coverage only.

7. Coverage Type and Endorsements

Standard HO-3 policies cover your dwelling on an "open peril" basis (everything except specifically excluded events) but personal property on a "named peril" basis (only listed events). Upgrading to HO-5 with broader personal property coverage adds 10-15% to premiums. Adding endorsements for jewelry, home business equipment, or sewer backup coverage incrementally increases monthly costs.

Author: Lauren Bishop;

Source: sixth-fleet.com

According to Robert Hunter, former Texas Insurance Commissioner and Director of Insurance at the Consumer Federation of America: "Most homeowners don't realize that insurers use hundreds of variables in their pricing algorithms, and small changes in any factor can compound into significant premium differences. Two identical homes on the same street might have premiums that differ by 25% simply because one homeowner has filed a claim in the past five years while the other hasn't."

How to Lower Your Monthly Homeowners Insurance Payment

Bundle with Auto Insurance

Most insurers offer 15-25% discounts when you combine home and auto policies. A homeowner paying $200 monthly and $150 monthly for auto could save $50-$87 monthly through bundling. Run the numbers carefully—sometimes the bundled price with one company exceeds buying separate policies from different insurers.

Increase Your Deductible Strategically

Moving from a $500 to $1,000 deductible saves about 10%, while jumping to $2,500 saves 20-25%. The sweet spot for most homeowners sits at $2,500—high enough for meaningful savings but manageable in an emergency. Avoid deductibles you couldn't cover from savings within 30 days.

Install Protective Devices

Central fire and burglar alarms connected to monitoring services earn 5-10% discounts. Smart home systems that detect water leaks can reduce premiums by another 5%. Impact-resistant roofing in hurricane zones might save 10-20%. These upgrades cost money upfront but pay back through reduced premiums and actual protection.

Improve Your Credit Score

In states where credit-based insurance scoring applies, improving your credit from fair to good could reduce premiums by 15-20%. Pay down credit card balances, correct errors on credit reports, and avoid new hard inquiries before insurance shopping.

Shop Around Every Two to Three Years

Loyalty doesn't pay in insurance. Insurers often raise rates on existing customers while offering better deals to new ones. Get quotes from at least five companies, including direct writers (State Farm, Allstate) and independent agent networks (Travelers, Nationwide). Price differences of 30-50% for identical coverage aren't unusual.

Reduce Coverage on Outbuildings

That detached garage or shed might carry more coverage than necessary. Reducing coverage on structures you could afford to replace out-of-pocket lowers premiums without exposing your main dwelling.

The single greatest money-saving strategy in homeowners insurance isn’t raising your deductible or installing a security system — it’s shopping around consistently. Consumers who compare at least five quotes every two to three years save an average of 20 to 35 percent compared to those who auto-renew without question.

— Amy Bach

Ask About Uncommon Discounts

Retiree discounts (5-10% for those over 55 who are home more often), professional organization memberships, claims-free longevity (increasing percentages for each claim-free year), and even being a non-smoker can trim costs. Insurers don't advertise every discount—you must ask specifically.

Author: Lauren Bishop;

Source: sixth-fleet.com

Monthly vs. Annual Payment: Which Costs Less?

Paying annually almost always costs less than monthly installments. Insurers charge convenience fees ranging from $3 to $15 per monthly payment, adding $36-$180 annually. Some insurers also apply interest rates of 5-10% APR to monthly payment plans, effectively treating them as loans.

A $2,400 annual premium might cost: - Paid annually: $2,400 (often with a small discount for full payment) - Paid monthly: $2,520-$2,640 after fees and interest charges

That's $120-$240 wasted annually just for the privilege of spreading payments across 12 months. For a homeowner carrying this policy for 30 years, the difference compounds to $3,600-$7,200.

The budgeting argument for monthly payments makes sense if you lack the lump sum. A better approach: open a dedicated savings account and deposit your typical monthly homeowners premium cost there. When the annual bill arrives, you'll have the funds ready and keep the $120-$240 that would've gone to fees.

Author: Lauren Bishop;

Source: sixth-fleet.com

Mortgage escrow complicates this calculation. When your lender collects insurance premiums through escrow, they typically pay annually on your behalf, so you avoid monthly payment fees. However, you lose control over shopping around and timing, and escrow analysis errors can cause payment shock when your monthly mortgage payment suddenly jumps.

FAQ: Common Questions About Monthly Homeowners Insurance Costs

Making Informed Decisions About Your Homeowners Insurance Costs

Understanding what is the average monthly homeowners insurance cost gives you a baseline, but your actual premium depends on dozens of variables specific to your property and situation. The $183 national average serves as a reference point, not a target.

Smart homeowners treat insurance as a regular budget review item. Set a calendar reminder each year, three months before renewal, to gather quotes from multiple insurers. Your circumstances change, insurer appetites shift, and new competitors enter markets—last year's best rate might not hold this year.

Balance premium savings against coverage adequacy. Cutting your monthly payment by $30 through higher deductibles or reduced coverage might seem appealing until you face a major claim. Insurance exists to protect against financial catastrophe, not to be the cheapest line item in your budget.

Document your home's contents and condition now. When disaster strikes, you'll struggle to remember everything you owned or prove your home's pre-loss condition. Photos, videos, and receipts stored in cloud storage provide evidence that supports claims and ensures you receive full compensation under your policy.

The homeowners insurance market continues evolving rapidly. Climate change, inflation, and insurer profitability concerns drive changes in availability and pricing. Staying informed about these trends helps you anticipate changes and adapt your coverage strategy accordingly.

Your monthly premium represents protection for likely your largest asset. Invest time understanding what you're buying, what you're paying for, and whether you're getting value. The few hours spent researching and comparing options can save thousands of dollars and prevent devastating coverage gaps when you need your policy most.