Aerial view of American suburban neighborhood with houses and a translucent insurance shield icon with dollar sign overlay

How Much Does Home Insurance Cost Per Month in 2024?

Content

Homeowners across the United States pay vastly different amounts for insurance each month, depending on where they live and what they're protecting. Understanding these costs before you buy or refinance helps you budget accurately and avoid payment shock when your first bill arrives.

National Average Monthly Home Insurance Costs

Most homeowners pay between $125 and $250 per month for insurance, though this range shifts dramatically based on location and coverage needs. The national average sits around $183 monthly, which translates to roughly $2,200 annually for a standard policy.

Breaking down the numbers reveals important distinctions between median and mean premiums. The median monthly cost—the point where half of homeowners pay more and half pay less—typically runs about $165. The mean (mathematical average) skews higher at $183 because expensive coastal and disaster-prone markets pull the average upward. If you're budgeting for a home purchase, using the median gives you a more realistic baseline for typical markets.

Annual premiums divided into monthly payments show clearer patterns across different home values:

| Home Value | Dwelling Coverage | Average Monthly Premium | Annual Cost |

| $250,000 | $200,000 | $145 | $1,740 |

| $350,000 | $280,000 | $175 | $2,100 |

| $500,000 | $400,000 | $225 | $2,700 |

| $750,000 | $600,000 | $310 | $3,720 |

These figures assume standard construction, moderate deductibles ($1,000-$2,500), and locations outside high-risk zones. Your actual payment depends heavily on state-specific factors and individual risk characteristics.

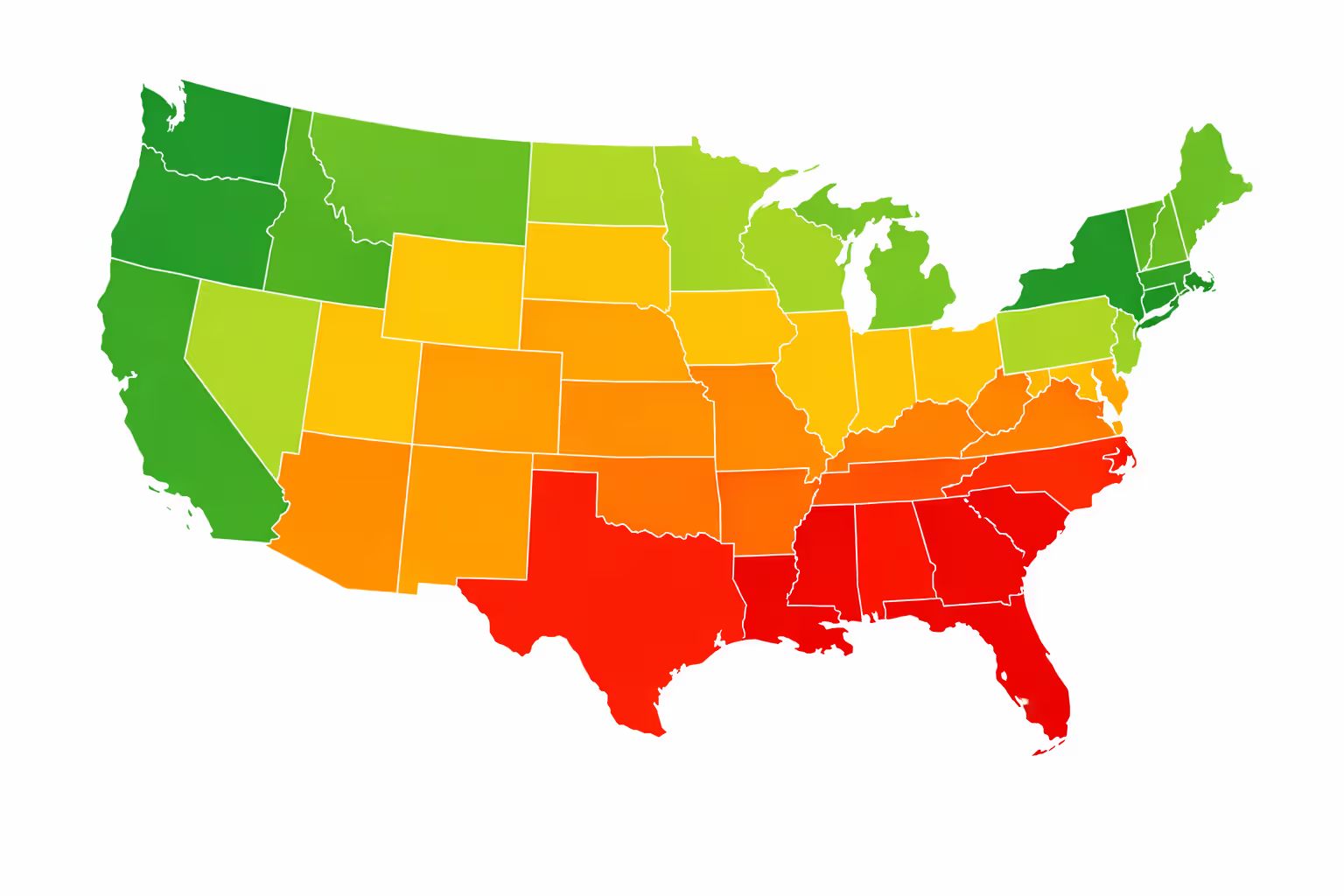

Monthly Home Insurance Costs by State

Author: Ethan Caldwell;

Source: sixth-fleet.com

Geography determines your premium more than almost any other factor. Homeowners in Louisiana face monthly bills averaging $335, while those in Hawaii pay around $58—a difference of nearly $3,300 per year for comparable coverage.

Coastal states with hurricane exposure dominate the expensive end. Florida homeowners pay approximately $285 monthly, while Texas residents average $265. These states combine severe weather risk with high reconstruction costs and frequent claims, creating a perfect storm for premium increases.

The least expensive states cluster in the Pacific Northwest and parts of the Midwest, where natural disasters occur less frequently and building costs remain moderate. Vermont, Oregon, and Wisconsin residents enjoy monthly premiums between $70 and $90.

Regional patterns emerge clearly when examining state-by-state data. The Gulf Coast and Atlantic seaboard show consistently elevated costs. Tornado Alley states like Oklahoma and Kansas fall into the mid-to-high range despite being inland. Mountain West and Great Lakes states generally offer the best value, assuming you avoid wildfire-prone areas in California and Colorado.

| State | Average Monthly Premium | Primary Cost Drivers |

| Louisiana | $335 | Hurricanes, flooding, claims frequency |

| Florida | $285 | Hurricanes, sinkholes, litigation costs |

| Texas | $265 | Hail, windstorms, coastal exposure |

| Oklahoma | $245 | Tornadoes, hail storms |

| Kansas | $230 | Severe weather, wind damage |

| Nebraska | $220 | Hail, tornado risk |

| Colorado | $195 | Hail, wildfires |

| Mississippi | $190 | Hurricanes, poverty rates |

| Alabama | $185 | Tornadoes, coastal storms |

| South Dakota | $180 | Hail, severe weather |

| Oregon | $88 | Low disaster frequency |

| Idaho | $85 | Minimal weather risks |

| Utah | $82 | Dry climate, low claims |

| Wisconsin | $78 | Stable weather patterns |

| Hawaii | $58 | Low wind claims, concrete construction |

7 Factors That Determine Your Monthly Premium

Insurance companies evaluate dozens of variables when calculating your specific premium. Seven major categories account for most of the variation between what different homeowners pay.

Home Characteristics (Age, Construction Type, Square Footage)

Older homes cost more to insure because outdated electrical systems, plumbing, and roofing create higher claim risks. A 1950s ranch with original wiring might run $190 monthly, while an identical floor plan built in 2015 costs $145. Insurers worry about knob-and-tube wiring causing fires and galvanized pipes bursting.

Construction materials matter enormously. Brick homes in tornado zones cost 15-20% less to insure than wood-frame structures because they withstand high winds better. A 2,000-square-foot brick home in Oklahoma might cost $205 monthly versus $245 for wood siding. Fire-resistant roofing materials like metal or tile can shave another $20-30 off monthly bills in wildfire areas.

Square footage drives premium calculations directly because larger homes cost more to rebuild. Adding 1,000 square feet typically increases your monthly payment by $30-50, depending on local construction costs. A 3,500-square-foot home runs about $240 monthly compared to $175 for a 2,000-square-foot property with similar features.

The cost of insurance is directly tied to the cost of rebuilding. Homeowners who invest in resilient construction — impact-resistant roofs, reinforced framing, updated electrical systems — aren’t just protecting their property. They’re fundamentally changing their risk profile, and insurers reward that with meaningfully lower premiums year after year

— Janet Ruiz

Location-Specific Risks (Weather, Crime Rates, Fire Protection)

Distance from the nearest fire hydrant and fire station affects premiums more than most homeowners realize. Living more than five miles from a fire station can increase monthly costs by $40-70 because response times lengthen and total losses rise. Rural homeowners often pay $210 monthly for coverage that costs $155 in town.

Crime statistics in your ZIP code influence theft and vandalism coverage pricing. High-crime neighborhoods see premiums 10-15% above nearby low-crime areas. A home worth $300,000 in a high-theft area might cost $200 monthly versus $170 in a safer neighborhood two miles away.

Weather patterns create the most dramatic variations. Hurricane-prone coastal areas, tornado zones, and wildfire regions all carry substantial surcharges. Moving from inland North Carolina to the Outer Banks can double your monthly premium from $130 to $260 for the same home value.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Coverage Choices and Deductibles

Selecting higher dwelling coverage limits increases monthly costs proportionally. Bumping coverage from $300,000 to $350,000 adds roughly $25-35 to your monthly bill. Extended replacement cost coverage, which pays above policy limits if construction costs spike after a disaster, typically adds another $15-25 monthly.

Deductible selection creates immediate trade-offs. Raising your deductible from $1,000 to $2,500 typically reduces monthly premiums by $20-35. A homeowner paying $195 monthly with a $1,000 deductible might drop to $165 with a $2,500 deductible—saving $360 annually while accepting more out-of-pocket risk per claim.

Personal property coverage, liability limits, and optional endorsements all adjust your final premium. Adding $100,000 in extra liability protection costs about $8-12 monthly. Scheduling expensive jewelry or art adds $3-8 per $1,000 of additional coverage.

Real-world examples illustrate these combinations clearly. A 25-year-old, 2,200-square-foot frame home in suburban Atlanta with $350,000 dwelling coverage and a $1,500 deductible runs approximately $165 monthly. The same home with $500,000 coverage and a $1,000 deductible jumps to $235. Switching to a $5,000 deductible and $400,000 coverage brings it back down to $180.

How to Calculate Your Estimated Monthly Payment

Estimating your specific premium before shopping helps you budget accurately and spot overpriced quotes. Start with your state's average rate per $1,000 of dwelling coverage, then adjust for your home's characteristics.

The basic formula multiplies your dwelling coverage amount by your state's rate per thousand, then divides by twelve for a monthly figure. If your state averages $0.85 per $1,000 of coverage and you need $400,000 in dwelling protection: ($400,000 ÷ $1,000) × $0.85 = $340 annually, or roughly $28 monthly as a baseline.

This simplified calculation ignores many variables, so expect your actual quote to vary by 20-40%. Apply adjustment factors for known risk elements: add 15% for homes built before 1980, subtract 10% for brick construction in wind zones, add 25% for coastal locations within three miles of the ocean.

Step-by-step calculation for a specific example:

- Home value: $375,000 in suburban Denver

- Dwelling coverage needed: $300,000 (80% of home value)

- Colorado state average: $1.95 per $1,000 annually

- Base calculation: (300 × $1.95) = $585 yearly

- Monthly base: $585 ÷ 12 = $48.75

- Adjustments: +30% for wildfire zone, +10% for 1995 construction, -5% for hail-resistant roof

- Final estimate: $48.75 × 1.35 = $65.81 monthly

Author: Ethan Caldwell;

Source: sixth-fleet.com

Online calculators from major insurers provide more accurate estimates by incorporating additional data points. Tools from State Farm, Allstate, and Progressive ask about roof age, claims history, and security features to refine their projections. Expect calculator estimates to land within 15% of actual quotes for standard homes.

According to Robert Hunter, Director of Insurance at the Consumer Federation of America: "Premium estimates based solely on state averages miss critical individual factors. Two identical homes on the same street can have 25% different premiums based on the owners' credit scores, claims history, and chosen deductibles. Always get at least three actual quotes rather than relying on calculators alone."

Ways to Lower Your Monthly Homeowners Insurance Premium

Strategic decisions can reduce your monthly payment by $30-80 without sacrificing essential protection. The most effective tactics address the specific factors insurers weight heavily in their pricing models.

Bundling home and auto insurance with the same company typically saves 15-25% on your homeowner premium. A standalone policy costing $210 monthly might drop to $165 when bundled, saving $540 annually. This discount applies immediately and requires no home improvements or waiting periods.

Security and monitoring systems generate measurable savings because they reduce claim frequency. Installing a monitored burglar alarm cuts monthly costs by $10-20, while adding fire and smoke monitoring saves another $8-15. A complete system with professional monitoring might cost $45 monthly but reduce insurance by $25, creating a net cost of just $20 for substantial protection.

Claims-free history discounts grow over time, rewarding homeowners who avoid filing small claims. Three years without claims typically earns a 5% discount ($8-12 monthly on a $180 premium), while five years claims-free can reach 10% savings ($18-20 monthly). This makes paying out-of-pocket for minor repairs under $2,000 often worthwhile.

The smartest thing a homeowner can do is treat insurance as catastrophic protection, not a maintenance plan. Every small claim you file becomes part of your permanent record with insurers. Paying two thousand dollars out of pocket for a minor repair is far cheaper than the cumulative premium increases that follow even a single low-value claim

— Amy Bach

Deductible increases offer the fastest premium reduction. Each $500 increase in your deductible generally lowers monthly costs by $8-12. Jumping from $1,000 to $5,000 might save $50-70 monthly, though you must maintain emergency savings to cover that higher out-of-pocket amount.

Home improvements that reduce risk deliver ongoing savings. Upgrading to impact-resistant shingles saves $15-25 monthly in hail-prone areas. Replacing old electrical panels and plumbing can reduce premiums by 10-15% ($17-30 monthly). New roofs typically earn discounts of $20-40 monthly depending on material and location.

Avoid these common mistakes that increase premiums unnecessarily:

Filing multiple small claims signals higher risk to insurers. Two claims within three years can raise your premium 20-40% ($35-80 monthly) even if you received minimal payouts. Reserve insurance for losses exceeding $5,000 unless the damage threatens safety.

Letting coverage limits drift below 80% of replacement cost triggers penalties and inadequate protection. Underinsuring by $50,000 might save $15 monthly but leaves you covering tens of thousands out-of-pocket after a total loss.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Ignoring credit score impacts misses significant savings opportunities. Improving your credit from fair to good can reduce premiums by 15-20% in most states. A homeowner paying $225 monthly might drop to $185 simply by raising their credit score 50 points.

Frequently Asked Questions About Monthly Home Insurance Costs

Making Informed Decisions About Your Home Insurance Budget

Monthly home insurance costs range from under $60 to over $300 depending on location, home characteristics, and coverage choices. Understanding your state's baseline costs and the factors that increase or decrease premiums helps you budget accurately and avoid overpaying.

Start by researching your state's average rate per $1,000 of coverage, then adjust for your home's age, construction type, and location-specific risks. Get quotes from at least three insurers since pricing varies significantly between companies even for identical coverage. The difference between the highest and lowest quote often exceeds $50 monthly.

Prioritize adequate coverage over minimal premiums. Saving $30 monthly by underinsuring leaves you financially exposed after a major loss. Aim for replacement cost coverage at 80-100% of your home's rebuild value, then reduce costs through higher deductibles and available discounts rather than cutting coverage limits.

Review your policy annually as home values, construction costs, and personal circumstances change. A premium that seemed reasonable three years ago might now be 20% above market rates, costing you $35-60 monthly in unnecessary expenses. Regular shopping and policy adjustments keep your coverage current and competitively priced.