Homeowners insurance policy document on desk with magnifying glass, model house, pen, and reading glasses

How to Read a Homeowners Insurance Policy Section by Section

Content

Your homeowners insurance policy isn't light reading. Most run 30 to 50 pages and use language that feels deliberately obscure. But buried in those pages are the exact terms that determine whether you'll receive $150,000 or $15,000 after a kitchen fire—or whether your claim gets denied entirely.

This guide walks you through each section of your policy document, translates the jargon, and shows you exactly where to look for the details that matter most.

Most people spend more time researching a new TV than understanding their homeowners policy. Then when disaster strikes, they're shocked to discover they don't have the coverage they assumed they had. Reading your policy isn't optional—it's financial self-defense

— Amy Bach

What Makes Up Your Homeowners Insurance Policy Document

Your policy packet contains five distinct components, each serving a specific legal purpose:

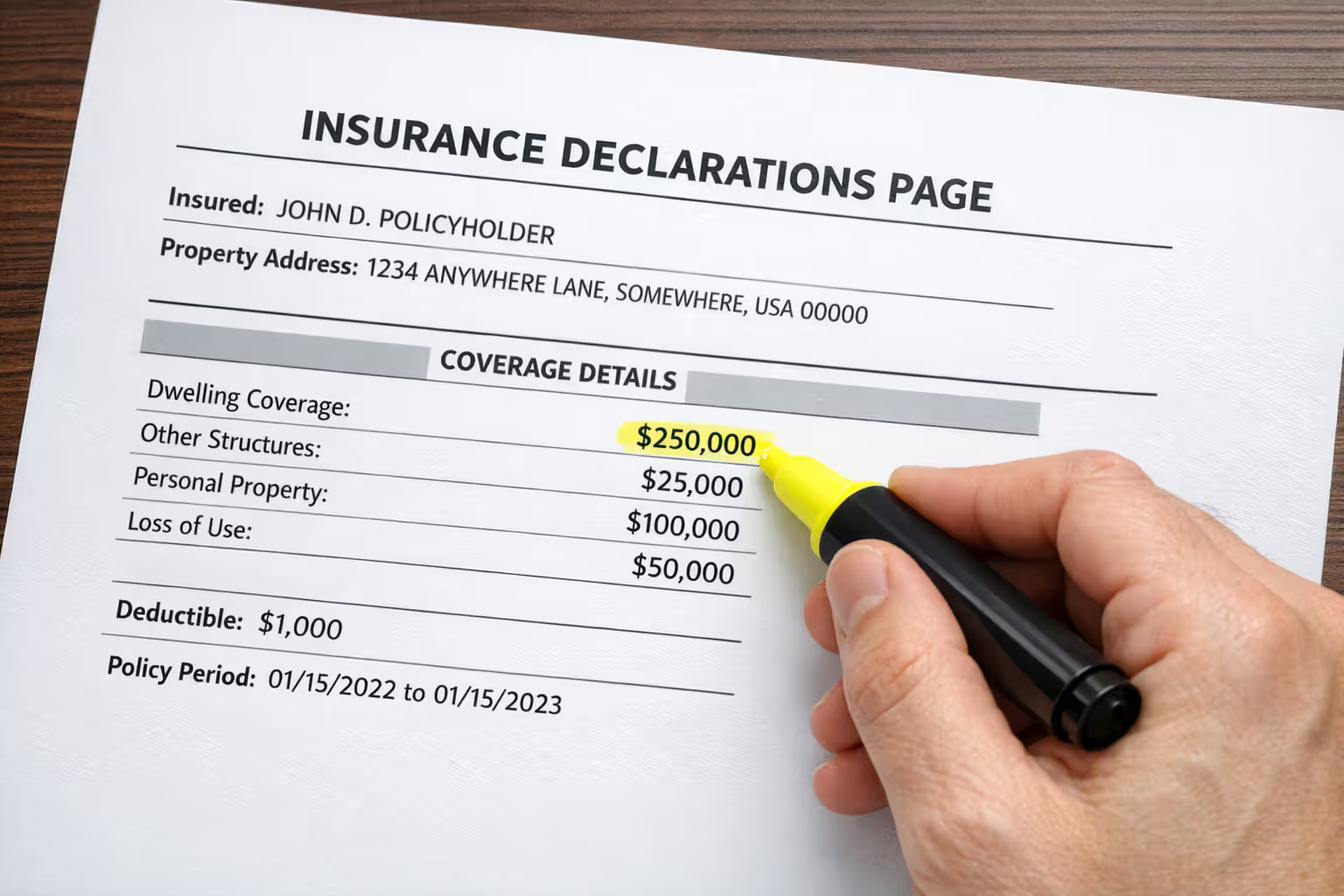

The declarations page (or "dec page") is your policy's snapshot—a one- or two-page summary listing your coverage limits, deductibles, premium, and basic property information. Think of it as the executive summary.

Coverage sections describe what the insurer agrees to pay for. Standard policies divide this into six lettered sections (A through F), each addressing different types of property or expenses.

Conditions outline the rules both you and your insurer must follow. This section explains your duties after a loss, how the company will settle claims, when coverage can be cancelled, and other procedural requirements.

Exclusions explicitly list what the policy won't cover—floods, earthquakes, intentional damage, and dozens of other scenarios. These limitations often surprise policyholders because they're not always intuitive.

Endorsements (sometimes called riders) modify your base policy. They might add coverage for jewelry, remove certain exclusions, or adjust policy terms. Each endorsement is typically a separate page added to your packet.

Why does this structure matter? Because when you file a claim, adjusters work through these sections in order. They first check whether the damaged item falls under a coverage section, then verify no exclusion applies, and finally review any endorsements that might affect the claim. Understanding this logic helps you navigate your own policy.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Decoding Your Policy Declaration Page Step-by-Step

The declarations page condenses your entire contract into a scannable format. Here's what each section tells you.

Personal Information and Property Details

At the top, you'll find your name (the "named insured"), policy number, and property address. Verify the address is correct—errors here can delay claims or cause coverage disputes if you own multiple properties.

Many dec pages also list the home's construction type (frame, masonry, brick veneer), square footage, year built, and number of stories. Insurers use these details to calculate risk. If your dec page says your home is 1,800 square feet but you've added a 400-square-foot addition, you're likely underinsured.

Coverage Limits and Premium Breakdown

This section shows your dollar limits for each coverage type (A through F, discussed in detail below). You might see:

- Dwelling (Coverage A): $350,000

- Other Structures (Coverage B): $35,000

- Personal Property (Coverage C): $175,000

- Loss of Use (Coverage D): $70,000

- Personal Liability (Coverage E): $300,000

- Medical Payments (Coverage F): $5,000

Next to these limits, you'll see individual premium amounts for each coverage, plus charges for any endorsements. The total annual premium appears at the bottom, often broken into installment amounts if you pay monthly or quarterly.

Deductibles and Policy Period

Your deductible is what you pay out-of-pocket before insurance kicks in. Most policies show a single deductible ($1,000 and $2,500 are common), but some states require separate, higher deductibles for wind, hail, or hurricane damage—sometimes expressed as a percentage (2% or 5% of Coverage A).

A $350,000 home with a 2% wind/hail deductible means you'd pay the first $7,000 of storm damage yourself. Many homeowners don't discover this until they file a claim.

The policy period shows your coverage start and end dates (typically one year). Coverage only applies to losses occurring within these dates.

Named Insureds and Mortgagee Information

The "named insured" section lists everyone covered under the policy—usually you and your spouse. Anyone not listed here (adult children, roommates, business partners) may not have coverage.

The "mortgagee" or "loss payee" section lists your mortgage lender. This ensures claim checks for dwelling damage are made out to both you and the lender, protecting their financial interest in your home.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Breaking Down the Six Standard Coverage Sections

Standard homeowners policies (HO-3 is most common) divide protection into six lettered sections. Each has distinct limits, coverage triggers, and common gaps.

| Coverage Letter | What It Covers | Typical Limit Examples | Real-World Example |

| Coverage A: Dwelling | The physical structure of your home, including attached structures like garages; built-in appliances, plumbing, electrical systems | Usually set to estimated rebuild cost; $250,000–$500,000+ depending on home size and location | A kitchen fire damages walls, cabinets, flooring, and roof in three rooms. Coverage A pays to rebuild these structural elements. |

| Coverage B: Other Structures | Detached structures on your property: sheds, fences, detached garages, gazebos | Typically 10% of Coverage A (so $25,000 if Coverage A is $250,000) | A fallen tree destroys your detached workshop. Coverage B pays to rebuild it, minus your deductible. |

| Coverage C: Personal Property | Your belongings: furniture, clothing, electronics, appliances (with sublimits for jewelry, cash, collectibles) | Usually 50–70% of Coverage A; $125,000–$350,000 | A burst pipe floods your basement, ruining furniture, a washer/dryer, and stored boxes of belongings. Coverage C reimburses you for these items. |

| Coverage D: Loss of Use | Additional living expenses if your home becomes uninhabitable: hotel bills, restaurant meals, storage fees | Typically 20–30% of Coverage A; $50,000–$100,000 | After a fire, you live in a hotel for three months while repairs are completed. Coverage D reimburses the extra costs beyond your normal housing expenses. |

| Coverage E: Personal Liability | Legal defense and damages if you're sued for injuries or property damage you cause to others | $100,000–$500,000 standard; can increase to $1 million+ | A guest slips on your icy driveway and breaks their hip. They sue for medical bills and lost wages. Coverage E pays legal costs and any settlement up to your limit. |

| Coverage F: Medical Payments | Medical bills for guests injured on your property, regardless of fault | $1,000–$5,000 (relatively small) | A neighbor's child cuts their hand on your fence. Coverage F pays the emergency room bill without a lawsuit. |

Coverage A is your policy's foundation. All other limits are often calculated as percentages of this number. If you underestimate rebuild costs here, you'll be underinsured across the board. Rebuild cost isn't the same as market value—a $400,000 home in a hot market might cost $500,000 to rebuild from scratch, especially with current lumber and labor costs.

Coverage B catches many people off guard. That $25,000 limit might seem adequate until you price replacing a custom 20-foot fence ($8,000), a large shed ($12,000), and a pergola ($7,000) simultaneously after a tornado.

Coverage C has two critical considerations: sublimits and valuation method. Most policies cap jewelry at $1,500 total, cash at $200, and collectibles at $2,500 unless you purchase additional coverage. The valuation method—actual cash value versus replacement cost—determines whether you get enough to buy new items or just their depreciated value. Always confirm you have replacement cost coverage for personal property.

Coverage D doesn't require receipts for your normal living expenses (your rent or mortgage, typical grocery bill). It only covers additional costs—the difference between your hotel bill and your normal housing cost, or restaurant meals versus home cooking.

Coverage E is where many homeowners are dangerously underinsured. If you have significant assets, the standard $300,000 won't protect you in a serious liability lawsuit. A $1 million umbrella policy costs roughly $150–$300 annually and provides crucial additional protection.

Common Homeowners Insurance Terms You Need to Know

Insurance policies use specific terms that carry legal weight. Misunderstanding them leads to claim disputes.

Actual Cash Value (ACV) means the insurer pays what your property was worth at the time of loss—original cost minus depreciation. A 10-year-old roof might have cost $15,000 new, but with depreciation, you'd receive perhaps $7,500. You'd pay the remaining $7,500 out-of-pocket to replace it.

Replacement Cost Value (RCV) pays to replace or repair property with new materials of similar quality, without deducting for depreciation. That same roof would be covered at today's full replacement cost of $18,000 (assuming prices increased). RCV costs 10–15% more in premiums but prevents you from being undercompensated.

Named perils policies only cover specific disasters explicitly listed—fire, lightning, windstorm, hail, theft, vandalism, and a dozen others. If your loss isn't on the list, you're not covered. HO-2 policies use this approach.

Open perils (also called "special form" or "all-risk") policies cover everything except what's explicitly excluded. This is broader protection. HO-3 policies—the most common—use open perils for your dwelling (Coverage A) but named perils for personal property (Coverage C). HO-5 policies use open perils for both.

Exclusions are losses the policy won't cover under any circumstances without additional endorsements: floods, earthquakes, sewer backups, mold (beyond limited amounts), nuclear hazards, war, and intentional damage. You'll find these listed in a dedicated section, often 3–5 pages long.

Endorsements modify your base policy. Common ones include:

- Water backup coverage (adds protection for sump pump failures and sewer backups)

- Scheduled personal property (increases limits for jewelry, art, or collectibles)

- Inflation guard (automatically increases Coverage A annually to keep pace with construction costs)

- Ordinance or law coverage (pays for upgrades required by current building codes)

Coinsurance clauses penalize underinsurance. If your policy has an 80% coinsurance clause and you insure your home for less than 80% of its replacement cost, the insurer will only pay a proportional amount of any claim. A home that costs $400,000 to rebuild should carry at least $320,000 in Coverage A. If you only carry $250,000, you'll face a penalty on every claim, even small ones.

Loss of use and additional living expenses are often used interchangeably, both referring to Coverage D. Some policies specify time limits (12 or 24 months maximum) in addition to dollar limits.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Where to Find What's NOT Covered (Exclusions and Limitations)

Exclusions typically appear in a dedicated section after coverage descriptions, though some are scattered throughout. Look for headers like "Losses We Do Not Cover" or "Section I – Exclusions."

Standard exclusions include:

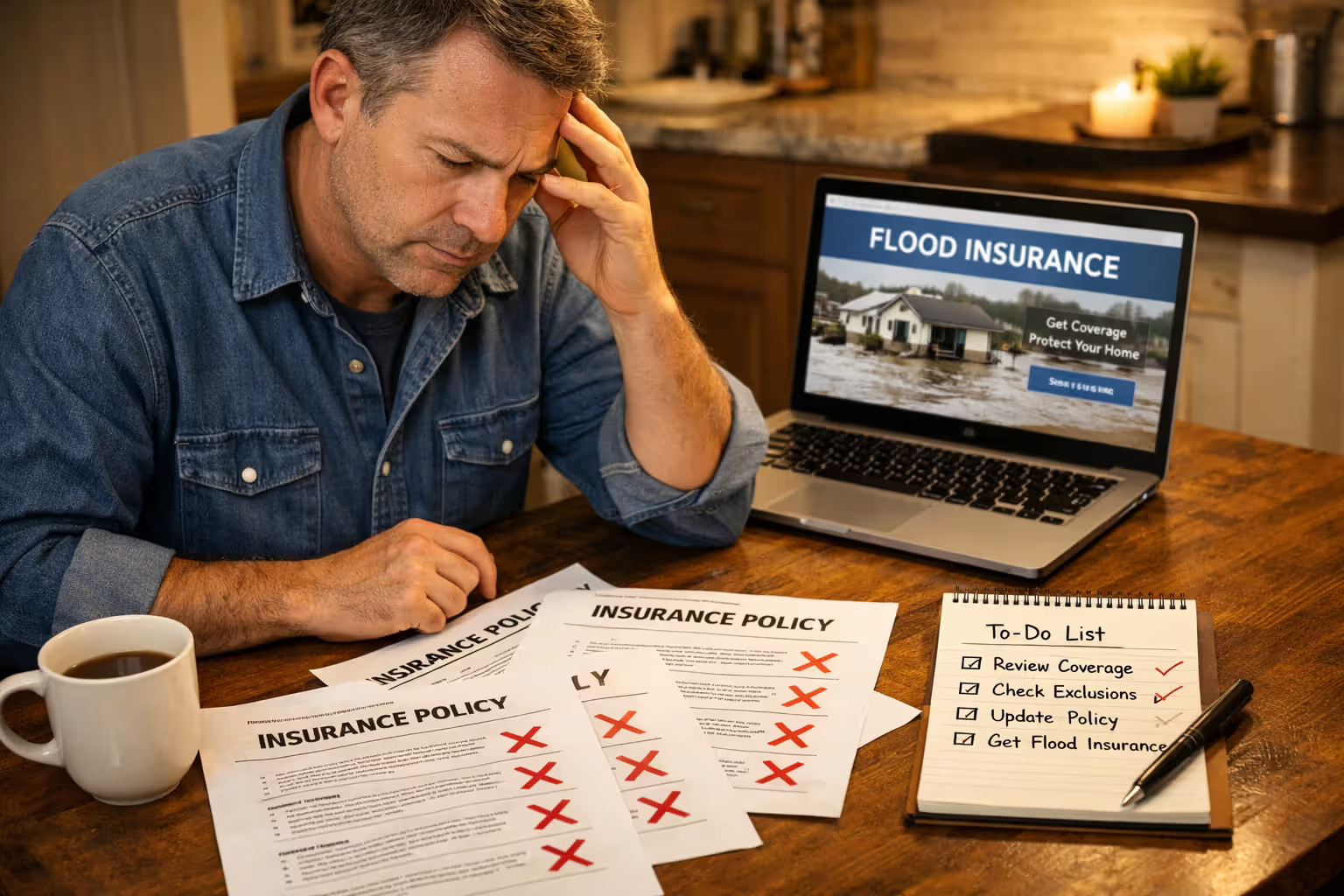

Flood damage from rising water, storm surge, or overflowing bodies of water. This includes basement flooding from heavy rain. You need a separate National Flood Insurance Program (NFIP) policy or private flood insurance. Even homes outside high-risk flood zones should consider this—20–25% of flood claims come from moderate- to low-risk areas.

Earth movement covers earthquakes, sinkholes, landslides, and mudflows. California, Alaska, and Pacific Northwest homeowners should purchase earthquake endorsements. Sinkholes are a particular concern in Florida.

Water damage from poor maintenance such as a slow leak you ignored for months, even though sudden pipe bursts are covered. Mold resulting from long-term leaks is typically excluded or limited to $10,000.

Sewer backup and sump pump failure unless you add water backup coverage (usually $40–$80 annually for $10,000–$25,000 in protection).

Wear and tear, deterioration, and mechanical breakdown means your insurer won't replace your 20-year-old roof just because it's old, or fix your broken furnace unless a covered peril caused the damage.

Business activities conducted from home often void coverage. If clients visit your home office and someone gets injured, your homeowners liability might not respond. You'd need a business policy or home business endorsement.

Certain breeds of dogs may be excluded or cause coverage denial. Pit bulls, Rottweilers, and wolf hybrids frequently appear on insurer restriction lists.

Limitations differ from exclusions—they don't eliminate coverage but cap it. Your policy might limit theft claims to $2,500 for jewelry, $2,500 for firearms, $1,500 for trailers, and $500 for cash. These sublimits apply even if your total Coverage C is $200,000.

Exclusions appear in dense paragraphs using phrases like "We do not cover," "This policy does not insure against," or "We do not cover loss caused by or resulting from." Read this section carefully with a highlighter.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Red Flags and Gaps to Look For When Reviewing Your Policy

Most coverage problems aren't discovered until claim time. Watch for these warning signs:

Underinsurance is epidemic. CoreLogic estimates 60% of U.S. homes are underinsured by an average of 20%. Construction costs have jumped 30–40% since 2020 in many markets. If you haven't increased your Coverage A limit in three years, you're likely underinsured. Request a replacement cost estimate from your insurer or a contractor annually. Don't confuse market value with rebuild cost—tear down your home and reconstruct it from the foundation up. That's your Coverage A target.

Actual cash value for roof or personal property means you'll face significant out-of-pocket costs after a claim. Many insurers have shifted to ACV roof coverage on older homes. If your policy says "Roof surfaces settled on an actual cash value basis," you'll only receive depreciated value. A 15-year-old roof with a 25-year lifespan would be reimbursed at 40% of replacement cost.

Low Coverage E limits relative to your net worth. If you have $500,000 in equity and retirement savings but only $300,000 in liability coverage, a serious injury lawsuit could wipe you out. Increase Coverage E to at least $500,000, or add a $1–2 million umbrella policy.

Missing endorsements for high-value items. That $8,000 engagement ring? Covered for only $1,500 under standard sublimits. Your $5,000 mountain bike? Same problem. Schedule these items individually with appraisals or purchase a blanket increase for jewelry, watches, and collectibles.

Percentage-based wind/hail deductibles in coastal or hail-prone areas. A 2% deductible on a $400,000 home means you pay $8,000 before coverage starts—far more than your standard $1,000 deductible. Some homeowners discover they have separate 5% hurricane deductibles, meaning $20,000 out-of-pocket.

No inflation guard or extended replacement cost. Without these endorsements, your Coverage A stays frozen while construction costs rise. Extended replacement cost (typically 25–50% above your Coverage A limit) provides a buffer if rebuild costs exceed your limit.

Mysterious coverage reductions. Some insurers reduce Coverage A after paying a total loss claim, or automatically decrease coverage on older homes. Review your dec page annually to catch unexpected changes.

Policy non-renewals or coverage restrictions. If you've filed multiple claims (especially water damage or dog bite claims), you may receive non-renewal notices. Two claims in three years often trigger this. Address problems proactively—fix plumbing issues, consider a higher deductible, or shop for a new insurer before you're forced to.

Frequently Asked Questions About Reading Homeowners Policies

Understanding Your Policy Protects Your Financial Future

Reading your homeowners insurance policy isn't about becoming an insurance expert. It's about knowing whether you'll have enough money to rebuild after a fire, replace your belongings after a burglary, or defend yourself in a liability lawsuit.

Most homeowners never look at their policy until disaster strikes, then discover their coverage doesn't match their assumptions. You might believe your $300,000 Coverage A fully protects your home, only to learn rebuild costs are $425,000. You might think your jewelry is covered, then find out the $1,500 sublimit won't replace your $6,000 wedding ring.

Set aside an hour this week to read through your policy with this guide in hand. Check your Coverage A against current rebuild costs. Verify you have replacement cost coverage for your dwelling and personal property. Look for percentage-based deductibles. Identify exclusions that leave you exposed. Compare your liability limits against your assets.

If you spot gaps, call your agent Monday morning. Adding endorsements or increasing limits costs far less than discovering you're underinsured after filing a claim. Your policy is a legal contract that determines whether a disaster becomes a financial catastrophe or a manageable setback. Treat it accordingly.