Top-down view of a desk with homeowners insurance policy documents, laptop showing insurance portal, house keys, magnifying glass, and sticky notes

How to Find Your Homeowners Insurance Policy If You Lost It

Content

You need proof of insurance for a claim, your mortgage company is asking for updated documents, or you're refinancing—and you have no idea where your homeowners insurance policy is. This situation is more common than you'd think. Between digital copies, paper files, and multiple storage locations, tracking down your policy can feel like searching for a needle in a haystack.

The good news: your policy exists somewhere, and there are systematic ways to locate it. This guide walks you through exactly where to look, who to contact, and how to retrieve your documents quickly.

Why You Need to Locate Your Policy Documents Now

Most homeowners don't think about their insurance policy until they need it. That's usually too late. Here's why finding your policy before an emergency matters:

Filing a claim becomes significantly harder without your policy number and coverage details. After a fire, flood, or theft, you're already stressed. Scrambling to find basic policy information adds unnecessary delays when time matters most.

Refinancing or selling your home requires proof of coverage. Lenders won't proceed without verification of adequate insurance. If you can't produce documentation quickly, you risk losing favorable interest rates or delaying a sale.

Policy reviews protect you from coverage gaps. Many homeowners discover they're underinsured only after a loss. Regular policy reviews—which require having the actual document—help you adjust coverage as your home's value increases or you acquire expensive belongings.

Mortgage escrow reconciliations need policy details. If your insurance is paid through escrow, your servicer periodically verifies coverage amounts match loan requirements. Missing these requests can trigger force-placed insurance, which costs significantly more.

I've seen too many homeowners lose thousands because they couldn't produce their policy after a loss. Insurance companies will eventually provide copies, but every day of delay is another day your claim isn't being processed. Keep your policy as accessible as your home's deed

— Jennifer Martinez

The stakes are real. Locating your policy now, while you don't need it urgently, saves you from problems later.

Where Your Homeowners Insurance Policy Is Most Likely Stored

Your policy exists in at least one of these locations. Start with the highest-probability spots first.

| Storage Location | What to Look For | Success Rate | Time Required |

| Insurance company portal | PDF downloads in document center | 85% | 5-10 minutes |

| Email inbox | Policy documents, renewal notices with attachments | 70% | 10-15 minutes |

| Physical files | Folder labeled "Insurance" or "Home Documents" | 60% | 15-30 minutes |

| Mortgage servicer | Escrow records, insurance verification letters | 50% | 1-3 business days |

| Insurance agent | Agent's client files (digital or physical) | 90% | Same day with phone call |

| State database | Limited to specific states with insurance tracking | 20% | Varies by state |

Check Your Email and Online Account Portals

Start here. This is the fastest path to your policy documents for most people.

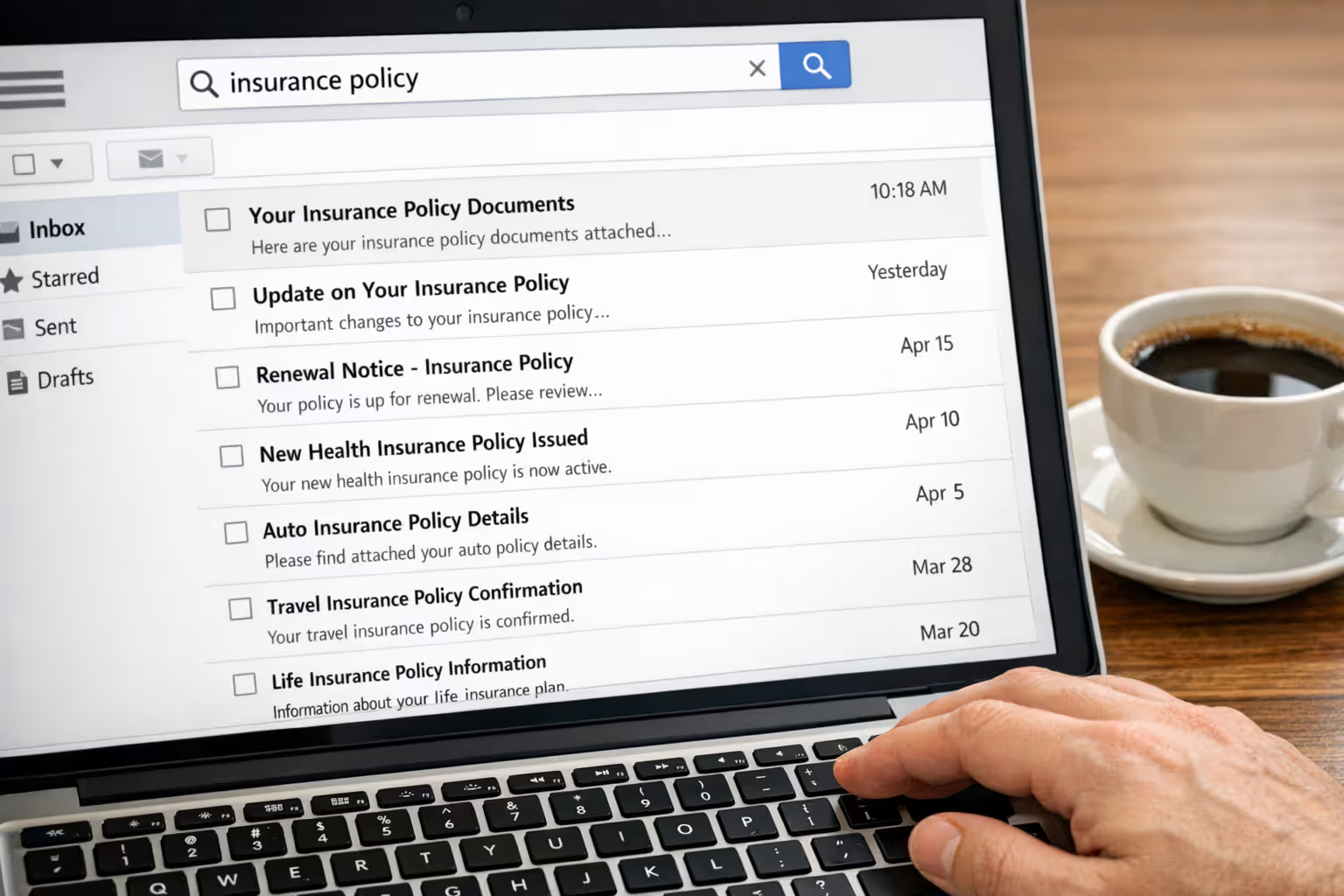

Search your email for the insurance company name, "policy documents," "declaration page," or "renewal." Insurance companies send annual renewal packets, and many attach full policy PDFs. Search back three years—you likely received digital copies even if you don't remember them.

Look specifically for emails with subject lines containing "Your Policy Documents," "Policy Number," or "Declaration Page Enclosed." These often include attachments or links to download your full policy.

Log into your insurance company's website or mobile app. Most insurers maintain customer portals where you can access current and past policy documents. If you've never logged in, use the "forgot password" function with the email address tied to your policy. The account likely exists even if you never activated it.

Once logged in, look for sections labeled "Documents," "Policy Information," "My Coverage," or "Billing & Documents." Policies are usually available as PDFs you can download immediately.

Check your insurance agent's portal if you purchased through an independent agent. Many agencies use client management systems that store all your policy documents in one place. You may have login credentials you forgot about.

Author: Lauren Bishop;

Source: sixth-fleet.com

Search Physical Files and Home Safes

Despite the digital shift, many homeowners still receive and store paper policies.

Check these specific locations: - Filing cabinets under "Insurance," "Home," or "Important Documents" - Home safes alongside deeds, titles, and other critical papers - Desk drawers where you keep bills and financial statements - Bookshelves where you might have stashed a folder - Kitchen junk drawers (surprisingly common)

Your most recent policy is usually 20-40 pages. The declaration page—the summary document—might be separate, often just 2-5 pages. Look for documents with your insurance company's logo and your property address.

Don't overlook renewal notices. Even if you can't find the full policy, renewal notices typically include your policy number, coverage amounts, and company contact information. That's enough to request a complete copy.

Review Mortgage Lender Records

If your insurance is paid through mortgage escrow, your lender has records of your coverage.

Your annual escrow analysis statement lists your insurance company, policy number, and premium amount. This statement, usually sent once per year, gives you everything needed to contact your insurer directly.

Closing documents from your home purchase include initial insurance information. If you haven't switched insurers since buying your home, those documents show your original policy details. Check the folder from your closing—it's typically 2-3 inches thick with various forms.

How to Request a Copy Directly from Your Insurance Company

When you can't locate your policy documents anywhere, requesting a copy from your insurance company is straightforward.

You'll need this information: - Your full name as it appears on the policy - Property address (the insured location) - Policy number if you have it (not required but speeds things up) - Last four digits of your Social Security number or date of birth for verification

Three ways to request your policy:

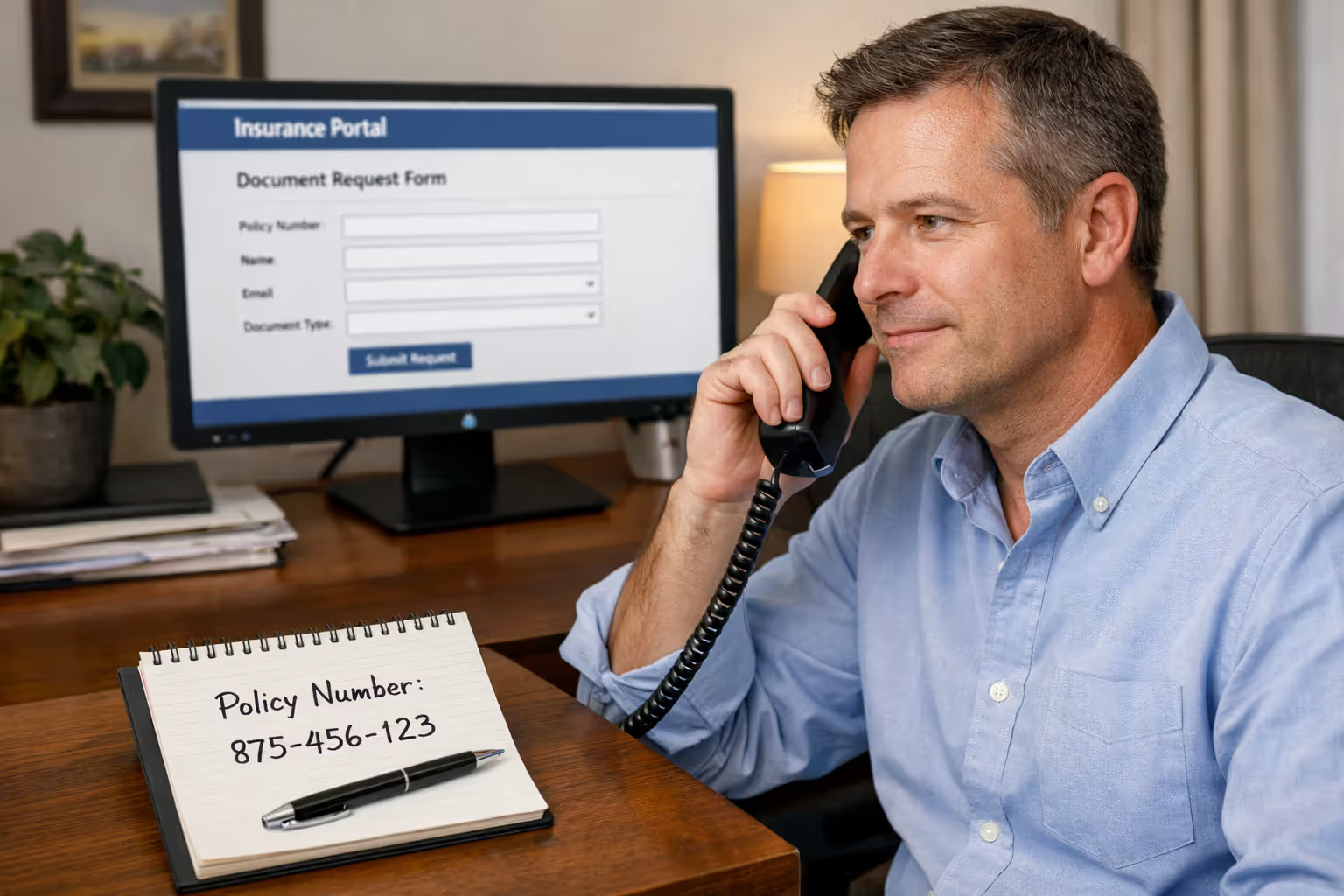

1. Call customer service. This is fastest. Most insurance companies can email a PDF of your current policy within minutes while you're on the phone. The number is on your insurance company's website or any correspondence you've received.

2. Use the online portal. If you can log in but don't see documents, look for "Request Policy Copy" or "Contact Us" features. Submit your request digitally and expect a response within 24-48 hours.

3. Email or mail a written request. This takes longest—typically 5-10 business days. Include your name, address, policy number if known, and a statement like "I am requesting a complete copy of my current homeowners insurance policy and declaration page."

Digital vs. mailed copies: Digital copies arrive via email, usually within 1-2 business days. Mailed copies take 7-10 business days but provide certified documents some institutions prefer for legal purposes. Specify your preference when requesting.

Cost: Requesting your own policy documents is free. Your insurance company must provide copies of your active policy at no charge. If you need historical policies from years past, some insurers charge $10-25 per policy year.

Author: Lauren Bishop;

Source: sixth-fleet.com

Finding Your Declaration Page When You Need It Fast

The declaration page (or "dec page") is your policy's summary sheet. It's not the full policy, but it contains the most critical information in a condensed format.

What's on your declaration page: - Policy number and effective dates - Named insureds (you and any co-owners) - Property address and description - Coverage amounts for dwelling, personal property, liability - Deductible amounts - Premium and payment schedule - Additional coverages or endorsements

Why the dec page matters: Many situations don't require your full policy. Mortgage companies, refinancing lenders, and proof-of-insurance requests often accept just the declaration page. It's 2-5 pages instead of 30-50, making it faster to locate and send.

Fastest retrieval methods:

Your declaration page is usually separate from the full policy in insurance company portals. Look for a specific "Declaration Page" or "Dec Page" link in your online account. It's often under a different menu than the full policy documents.

If you're calling your insurance company, specifically request "just the declaration page" rather than the full policy. Many insurers can email this within minutes since it's a shorter document.

Your annual renewal notice typically includes an updated declaration page. If you received a renewal packet in the last year, the dec page is probably in there even if you discarded other materials.

Common mistake: People assume the declaration page and full policy are the same document. They're not. The full policy includes all terms, conditions, exclusions, and legal language—often 30-50 pages. The declaration page is the personalized summary showing your specific coverage amounts and details. For most purposes, the dec page is sufficient.

What to Do If You Don't Know Your Insurance Company

This happens more often than you'd expect, especially if someone else set up your insurance, you inherited property, or your insurance is paid through escrow and you've never dealt with it directly.

Author: Lauren Bishop;

Source: sixth-fleet.com

Check Your Mortgage Escrow Statements

If your insurance premium is paid through your mortgage escrow account, your monthly mortgage statement or annual escrow analysis shows your insurance company's name.

Look for these sections on your mortgage statement: - "Escrow Account Activity" - "Disbursements" or "Payments Made" - "Annual Escrow Analysis" (sent once per year)

Insurance payments appear as disbursements to your insurance company, usually showing the company name and the amount paid. This tells you exactly who insures your home.

Contact Your Mortgage Servicer

Call your mortgage company's customer service and ask: "Can you tell me which homeowners insurance company my escrow account pays?"

They have this information readily available since they send payments on your behalf. The representative can provide: - Insurance company name and phone number - Policy number (sometimes) - Premium amount and payment dates

This takes one phone call and about 5-10 minutes. Have your mortgage account number ready to verify your identity.

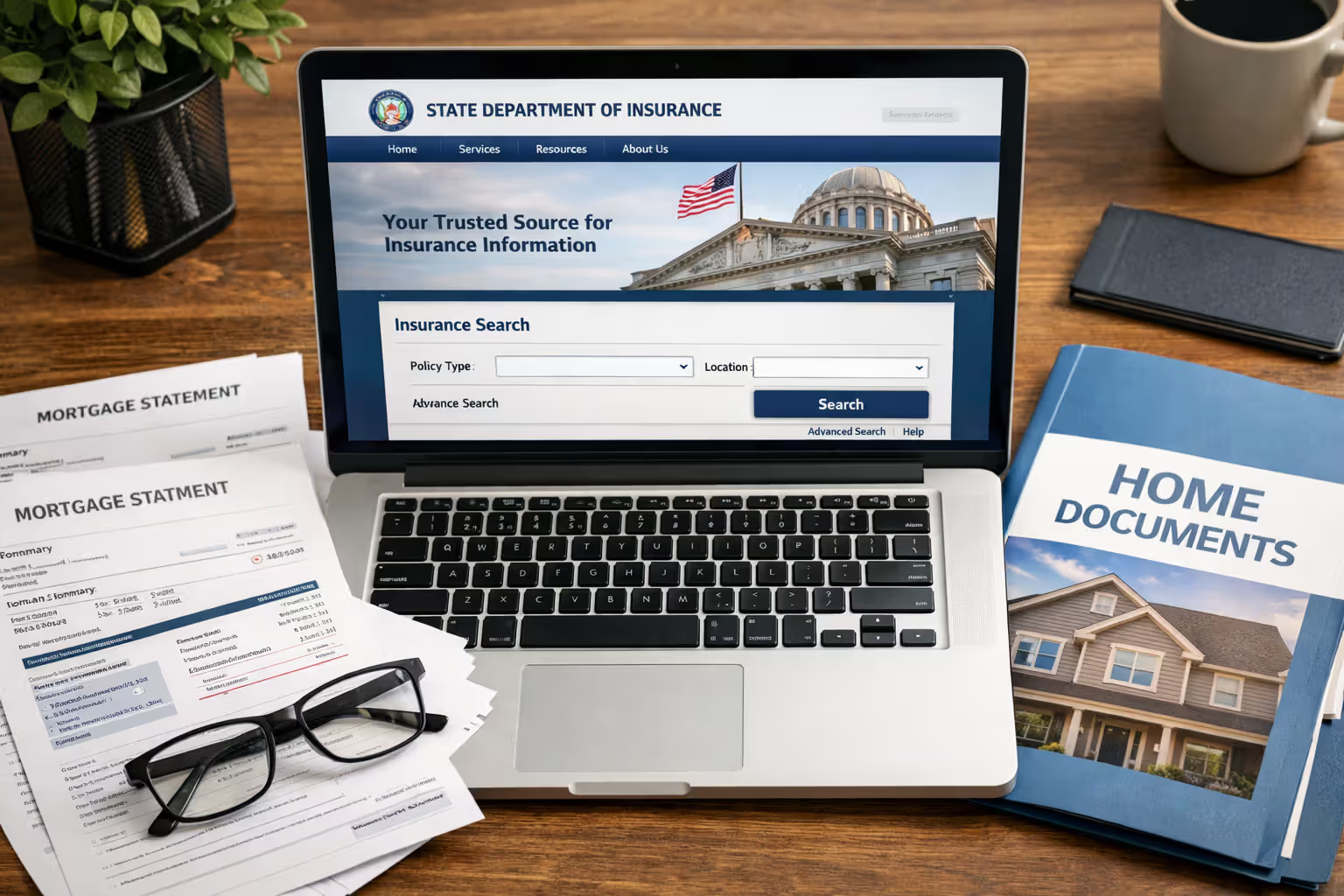

Use State Insurance Department Resources

Some states maintain databases where you can look up insurance policies tied to your property, though this varies significantly by state.

States with searchable databases or assistance programs: - California Department of Insurance offers a company lookup tool - Florida has an online policy search for certain coverage types - Texas Department of Insurance provides consumer assistance for policy lookups - New York's Department of Financial Services can help locate policies

To use state resources: 1. Visit your state's Department of Insurance website 2. Look for "Consumer Services" or "Find My Policy" tools 3. Call the consumer hotline if online tools aren't available 4. Provide your property address and identification

Limitations: State databases typically don't contain full policy information. They might confirm which company insures your property but won't provide policy documents. You'll still need to contact the insurance company directly once you identify them.

For inherited property: If you inherited a home and don't know the insurance status, check the deceased person's bank statements for insurance payments, contact the estate attorney who handled the property transfer, or search the home for any insurance correspondence.

How to Organize and Store Your Policy for Future Access

Once you've located your policy, set up a system so you never lose it again.

Digital storage best practices:

Create a dedicated folder on your computer or cloud storage labeled "Home Insurance" or "Property Insurance." Save your policy PDF with a clear filename like "Homeowners_Policy_2024_PolicyNumber.pdf."

Use multiple cloud backups: Store copies in at least two locations—Google Drive, Dropbox, iCloud, or OneDrive. If one service has issues, you have a backup. Enable automatic syncing so updated policies save automatically.

Email yourself a copy with a subject line like "HOME INSURANCE POLICY - DO NOT DELETE." This creates a searchable backup in your email that survives computer crashes.

Save on your phone. Download your policy PDF to your phone's files app or a document management app. In an emergency evacuation, you'll have immediate access even without internet.

Physical storage recommendations:

Keep one printed copy in a fireproof safe or lockbox with other critical documents like your home deed, birth certificates, and passport.

Store a second copy in an easily accessible file cabinet or desk drawer for quick reference during non-emergency situations.

Tell someone else where your policy is stored. If something happens to you, a spouse, adult child, or trusted person should know how to access your insurance information.

Document retention timeline:

Keep your current policy and the previous year's policy easily accessible. Archive policies from 2-7 years ago in long-term storage (you might need them for historical claim purposes). Policies older than seven years can typically be discarded unless you have ongoing claims from that period.

Set annual reminders: When your policy renews each year, immediately download and save the new policy documents. Add a calendar reminder for your renewal date labeled "Download New Insurance Policy."

Create an insurance information sheet with key details: company name, policy number, agent contact, phone numbers, and website login credentials. Store this separately from your policy so you can quickly access contact information even if you can't immediately locate the full document.

Author: Lauren Bishop;

Source: sixth-fleet.com

Common Questions About Locating Homeowners Insurance Policies

Take Control of Your Insurance Documents Today

Your homeowners insurance policy is one of the most important documents you own, yet it's often one of the least accessible when you need it. Whether you find it in an old email, tucked in a file cabinet, or by requesting a new copy from your insurer, the effort you make now prevents significant stress during claims, refinancing, or emergencies.

Start with your insurance company's online portal—it's the fastest path for most people. If that doesn't work, systematically check email, physical files, and mortgage records. When all else fails, a simple phone call to your insurance company resolves the issue within a day or two.

Once you locate your policy, set up a reliable storage system with both digital and physical backups. Your future self will thank you when you need proof of coverage and can produce it in minutes rather than days.

The five steps are straightforward: check online portals and email, search physical storage locations, contact your insurance company directly, locate your declaration page for quick needs, and establish an organized storage system. Follow this process, and you'll never lose track of your homeowners insurance policy again.