Desk with homeowners insurance documents, house key, calculator, pen, and bank envelope with a residential house in the background

How to Change Home Insurance with Escrow Step by Step

Content

Switching homeowners insurance when your premiums are paid through an escrow account requires coordination between you, your new insurer, and your mortgage servicer. Miss a step, and you could face coverage gaps, duplicate charges, or escrow shortages that increase your monthly payment. This guide walks you through the exact process to make the transition smooth while keeping your lender satisfied and your home protected.

Understanding How Escrow Accounts Handle Your Home Insurance Payments

Your mortgage lender collects a portion of your annual insurance premium with each monthly payment, holding these funds in escrow until your policy bill comes due. The servicer then pays your insurer directly from this account. This arrangement protects the lender's investment—if your home burns down without insurance, they lose their collateral.

What Happens to Your Premium Payments When You Switch Providers

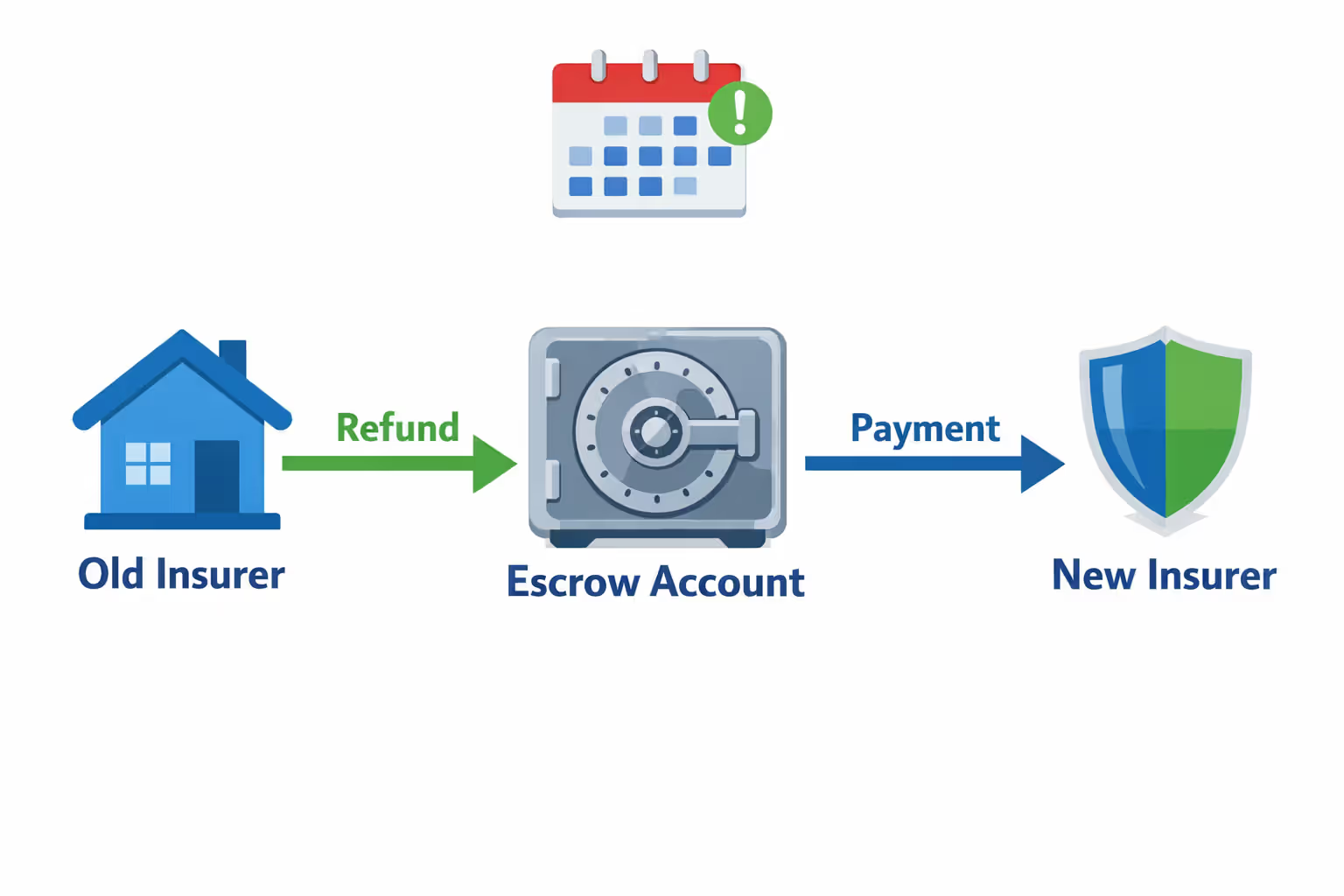

When you change insurance companies mid-policy, several financial transactions occur simultaneously. Your old insurer typically refunds the unused portion of your premium to your escrow account, not directly to you. Meanwhile, your new carrier bills the escrow account for the upcoming policy period. Your mortgage servicer must track these incoming refunds and outgoing payments, then recalculate your monthly escrow contribution based on the new premium amount.

The timing matters significantly. If your new policy costs $1,800 annually and starts July 1st, but your old $2,400 policy doesn't refund the unused six months ($1,200) until July 15th, your escrow account might temporarily run short. The servicer will still pay your new premium on time, but you could face a deficiency notice requiring a lump-sum payment or increased monthly contributions to rebuild the reserve.

Author: Samantha Kessler;

Source: sixth-fleet.com

Why Your Lender Must Be Involved in the Process

Mortgage contracts include an "insurance clause" requiring you to maintain coverage that meets specific standards. Your lender holds a financial interest in your property, listed on your policy as the mortgagee. Without proper notification, your servicer might continue paying your old insurer, leaving you with duplicate coverage and a mess to untangle.

Lenders also verify that your new policy meets their minimum requirements: dwelling coverage at least equal to your loan balance (or the home's replacement cost), liability limits typically $300,000 or higher, and an insurer with acceptable financial strength ratings. Some servicers maintain approved-carrier lists and will reject policies from companies they consider financially unstable.

Before You Switch: What to Check in Your Current Policy and Mortgage Agreement

Preparation prevents the most common switching problems. Before requesting quotes, gather your current declarations page and mortgage documents to understand what you're working with and what constraints you face.

Review Your Policy Cancellation Terms and Refund Policies

Most homeowners policies allow mid-term cancellation, but the refund calculation method varies. "Pro-rata" cancellation returns the exact unused premium—if you cancel halfway through a $1,200 policy, you get $600 back. "Short-rate" cancellation penalizes early termination, typically returning only 90% of the unused premium. Check your policy's cancellation provision, usually found in the "Conditions" section.

Some carriers impose minimum earned premiums. If you cancel within the first 60 days, they might keep the entire first two months' premium regardless of when coverage ends. This particularly affects borrowers who refinance shortly after buying a home and discover their new lender requires different coverage.

Verify Your Lender's Insurance Requirements

Request your servicer's insurance requirements in writing before shopping. Requirements vary by loan type and property characteristics. FHA loans mandate specific coverage types. Homes in flood zones require separate flood insurance. Properties with detached structures might need higher "other structures" coverage than standard policies provide.

Pay attention to deductible restrictions. Many lenders cap wind/hail deductibles at 5% of dwelling coverage in coastal areas. If your home is insured for $300,000, that's a maximum $15,000 deductible. Choosing a $20,000 deductible to save on premiums will trigger a lender rejection, forcing you to scramble for alternative coverage.

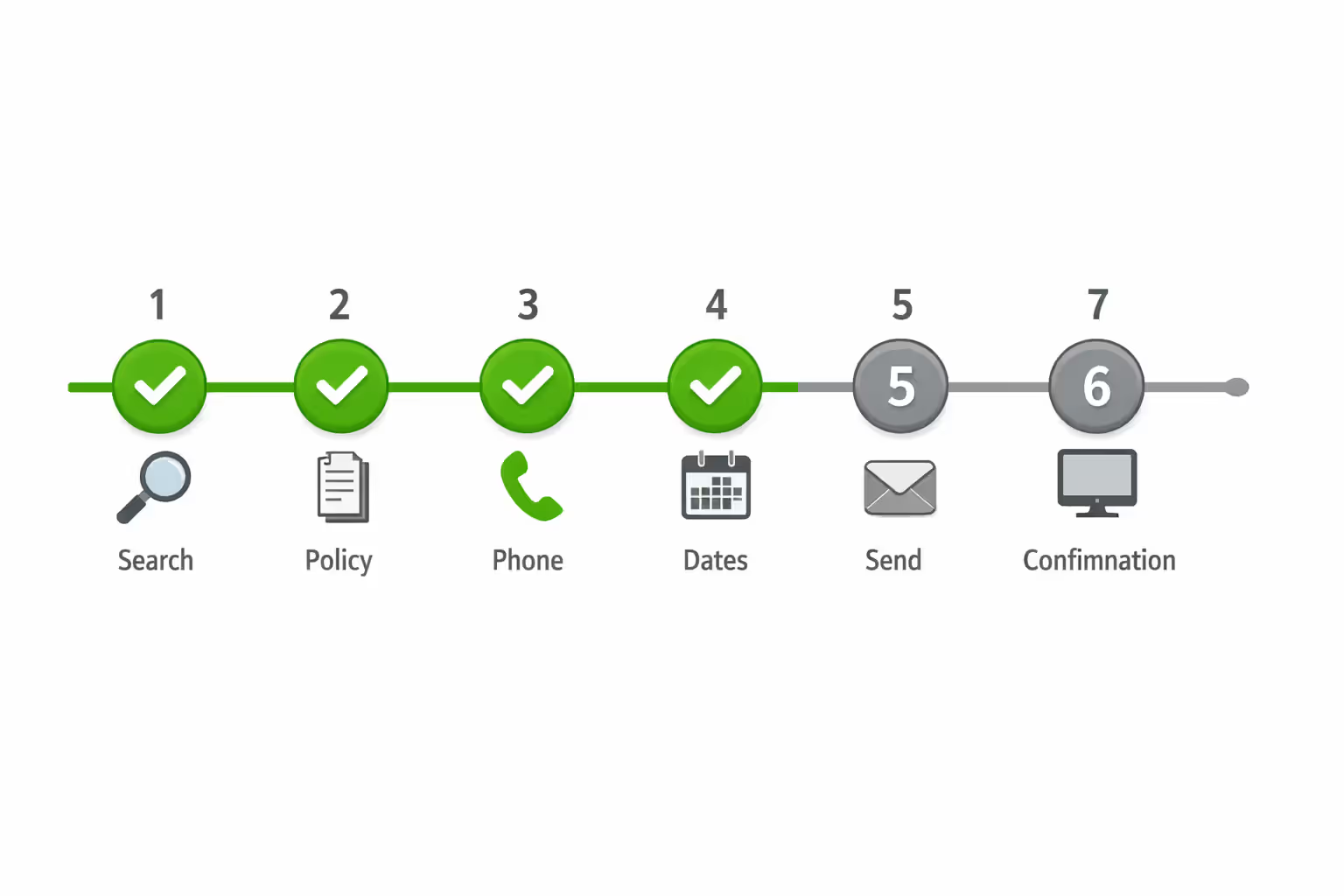

The 7-Step Process to Change Homeowners Insurance with an Escrow Account

This sequence prevents coverage gaps and ensures your escrow account transitions smoothly between carriers.

Step 1: Shop and compare quotes at least 30 days before your desired effective date. This buffer accommodates lender review time and potential complications. Request quotes with identical coverage limits to your current policy first, then adjust based on your lender's requirements. Provide accurate information about your home's age, roof condition, and claims history—misrepresentations discovered after binding can void coverage.

Step 2: Select your new provider and request a policy quote with your mortgage company listed as mortgagee. The insurer needs your servicer's name and address exactly as it appears on your mortgage statement. Misspellings or old addresses (common after servicer mergers) delay the process. Request a binder or evidence of insurance showing your effective date, coverage amounts, and the lender's mortgagee designation.

Step 3: Contact your mortgage servicer's insurance department (not general customer service) to notify them of the upcoming change. Most servicers have dedicated insurance teams with specific procedures. Ask for their exact requirements: Do they need the declarations page, the full policy, or just a certificate of insurance? What's their processing timeline? Get a direct phone number and reference number for follow-up.

Step 4: Coordinate effective dates to avoid gaps or overlaps. Your new policy should begin the day after your old policy ends, or on the same date if you're canceling mid-term. Never let your old coverage lapse before your new policy activates. A single day without insurance can trigger a lender-placed policy—expensive force-placed coverage that might cost three times your regular premium.

Author: Samantha Kessler;

Source: sixth-fleet.com

Step 5: Submit all required documents to your lender at least 15 days before your effective date. Email and follow up by phone to confirm receipt. Request written confirmation that your new policy meets their requirements. If they identify deficiencies (insufficient coverage, unacceptable carrier, missing endorsements), you'll need time to address them before your effective date.

Step 6: Confirm your lender has updated their records and will pay your new carrier. Call your servicer's insurance department two days before your effective date. Verify they have your new policy number, premium amount, and payment schedule in their system. Ask when they'll process the first payment—some servicers pay 30 days before the due date, others wait until the due date arrives.

Step 7: Cancel your old policy only after confirming your new coverage is active and your lender has been updated. Contact your old insurer in writing (email creates a paper trail) specifying your cancellation date and requesting pro-rata refund to your escrow account. Request written confirmation of cancellation and expected refund amount. Keep this documentation for at least two years in case escrow accounting disputes arise.

Notifying Your Mortgage Company: Required Documents and Timelines

Mortgage servicers process thousands of insurance changes monthly, and their systems depend on receiving complete, accurate information. Incomplete submissions sit in queues for weeks, risking coverage gaps.

Most servicers require a declarations page showing policy number, effective dates, coverage amounts, premium, mortgagee clause, and deductibles. Some demand the complete policy, including all endorsements. A few accept certificates of insurance, though these often lack sufficient detail and cause delays.

Submit documents 15-20 business days before your effective date. Servicers typically need 10-15 business days to review, enter data into their systems, and set up payment instructions. Holidays and month-end processing periods extend these timelines. Submitting documents on December 20th for a January 1st effective date almost guarantees problems.

Follow up 7-10 days after submission if you haven't received confirmation. Servicer insurance departments handle high volumes, and submissions occasionally get misfiled or lost. Polite persistence prevents disasters. Get the reviewer's name and direct extension for efficient communication.

What Information Your Lender Needs from Your New Insurance Provider

Your servicer must verify specific data points before accepting your new policy. Dwelling coverage amount must meet or exceed their minimum—usually your loan balance or the home's replacement cost, whichever is higher. The mortgagee clause must list them correctly with their current mailing address (servicer addresses change frequently after corporate mergers).

They'll check your insurer's financial strength rating through A.M. Best, Standard & Poor's, or similar agencies. Most require minimum ratings of A- or better. Policies from unrated or poorly-rated carriers get rejected regardless of coverage quality. Your liability limits must meet their standards, typically $300,000 minimum, sometimes $500,000 for higher-value homes.

Deductibles receive scrutiny, especially in disaster-prone regions. Wind/hail deductibles, often percentage-based in coastal areas, must fall within their caps. Some servicers reject policies with separate roof deductibles or depreciation-based roof coverage, considering these insufficient protection for their collateral.

Common Mistakes That Cause Coverage Gaps or Escrow Problems

Even careful homeowners make errors that create expensive complications. Recognizing these pitfalls helps you avoid them.

Switching without lender approval first: Some borrowers bind new coverage, cancel the old policy, then notify their lender, assuming rubber-stamp approval. If the servicer rejects the new policy (wrong coverage amounts, unacceptable carrier, missing endorsements), you're stuck. You've canceled your old coverage, which most insurers won't reinstate. You'll scramble for replacement coverage, often at higher rates, while your lender threatens force-placed insurance.

Misaligned effective dates: Setting your new policy to start January 1st while your old policy runs through January 15th creates overlap—you're paying for duplicate coverage. Worse, starting new coverage January 16th when old coverage ends January 15th leaves a one-day gap. During that gap, any loss is uninsured, and your lender might impose force-placed coverage with retroactive premiums.

Inadequate coverage amounts: Choosing dwelling coverage based on your loan balance rather than replacement cost causes problems. If you owe $200,000 but rebuilding costs $350,000, your lender might accept $200,000 coverage, but you're dramatically underinsured. After a total loss, you'll receive $200,000, nowhere near enough to rebuild. Some servicers require replacement cost coverage regardless of loan balance, rejecting insufficient policies.

Not following up on escrow adjustments: After switching to cheaper insurance, borrowers assume their monthly payment will automatically decrease. Servicers perform escrow analyses annually, not immediately after policy changes. Your payment might not adjust for months. Meanwhile, excess funds accumulate in escrow. Eventually, you'll receive a refund, but you've essentially given your servicer an interest-free loan. Call and request an immediate escrow analysis after your premium changes significantly.

Canceling the old policy too early: Eager to stop paying for coverage they're replacing, some homeowners cancel their existing policy before their new coverage activates or before their lender updates their records. The old insurer processes the cancellation immediately. The new insurer might delay activation due to inspection requirements or underwriting questions. You're uninsured for days or weeks, violating your mortgage agreement and risking force-placed coverage.

The biggest mistake I see is homeowners treating insurance changes like a simple transaction, forgetting their lender is a third party to the contract.We need time to verify coverage, update our systems, and redirect payments. Rush the process, and you'll create problems that take months to resolve

— Jennifer Martinez

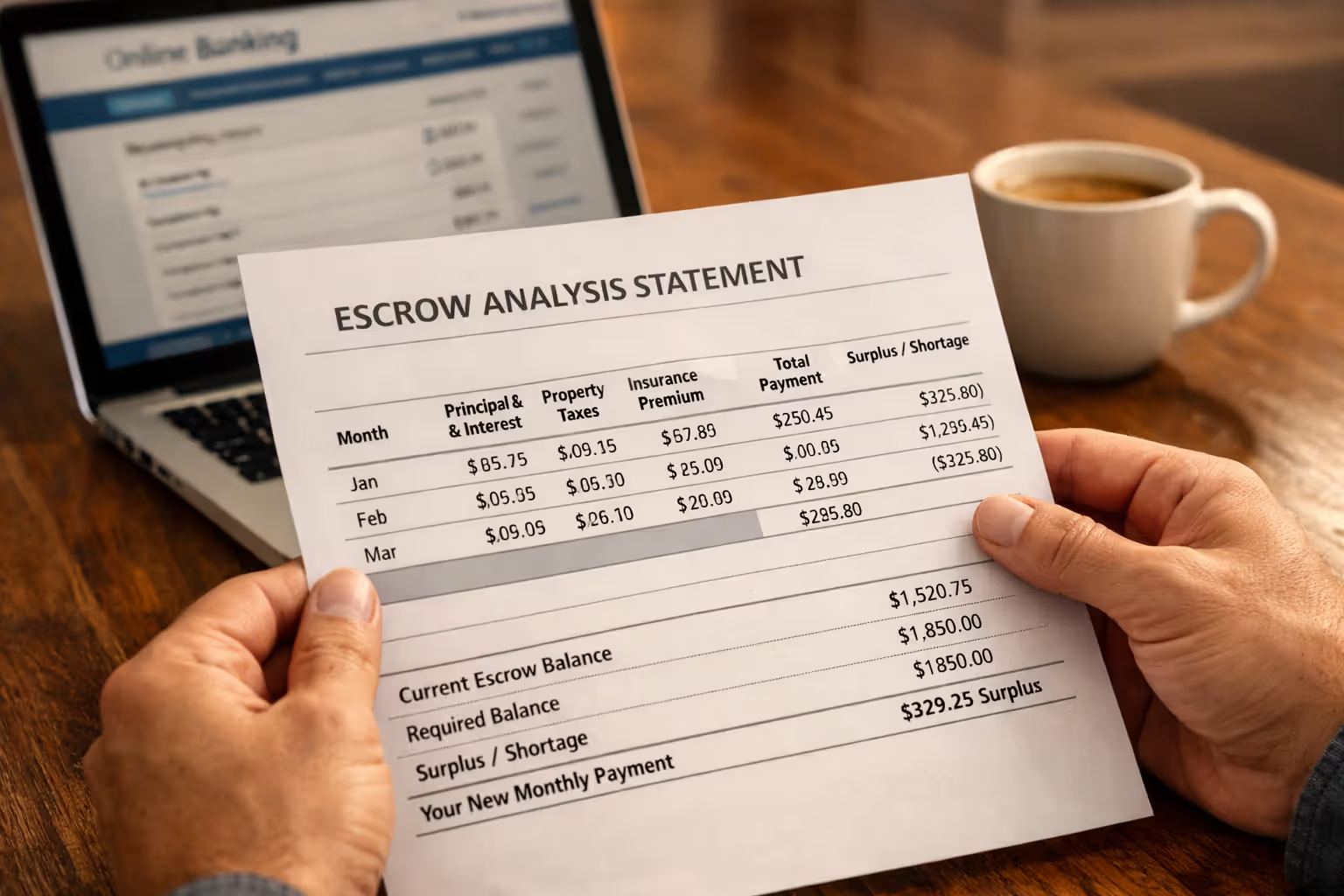

How Your Escrow Payment Changes When You Switch Insurance Providers

Your monthly escrow contribution covers insurance premiums and property taxes, with a cushion (typically two months' expenses) to handle payment timing variations. When your insurance premium changes, your servicer recalculates your required monthly contribution.

| Scenario | Impact on Monthly Escrow | Lender Actions | Timeline |

| Premium Decreases (e.g., $2,400 to $1,800 annually) | Monthly payment drops by ~$50 ($600 annual savings ÷ 12 months). Existing escrow balance may show surplus. | Servicer performs escrow analysis, recalculates required monthly payment, and refunds any surplus exceeding maximum allowed cushion (typically within 30 days of analysis). | Changes typically reflected at next annual escrow analysis unless you request immediate review. Refund issued within 30 days of analysis completion. |

| Premium Stays Similar (e.g., $2,400 to $2,350 annually) | Minimal monthly change (~$4 decrease). Escrow balance remains adequate. | Servicer updates premium amount in system and adjusts monthly payment at next escrow analysis. No significant account impact. | Reflected at annual escrow analysis (typically anniversary of loan closing). May not trigger immediate payment adjustment due to small difference. |

| Premium Increases (e.g., $2,400 to $3,200 annually) | Monthly payment increases by ~$67 ($800 annual increase ÷ 12 months). May create escrow shortage if increase is substantial. | Servicer performs escrow analysis, identifies shortage, and offers repayment options: spread over 12 months (higher monthly payment) or lump-sum payment to cover deficiency. | Shortage notice typically sent within 30-45 days of premium increase. You choose repayment method; new payment amount starts 30 days after notice. |

Escrow shortages occur when your account lacks sufficient funds to cover upcoming payments plus the required cushion. If your premium jumps $800 annually but you've only been contributing for the old premium, your account will run short when the new, higher premium comes due. The servicer covers the shortfall temporarily, then bills you for repayment.

You'll receive an escrow analysis statement showing the calculation: projected annual insurance and tax payments, required cushion, current balance, and any shortage or surplus. Review this carefully. Servicers occasionally make errors, using incorrect premium amounts or failing to credit refunds from your old insurer.

Request an immediate escrow analysis after switching insurance rather than waiting for your annual review. If your premium decreased significantly, you'll receive your refund months earlier. If it increased, you'll avoid a larger shortage accumulating over time. Most servicers perform on-demand analyses if you call and request one after a policy change.

Author: Samantha Kessler;

Source: sixth-fleet.com

Frequently Asked Questions About Switching Home Insurance with Escrow

Changing homeowners insurance with an escrow account demands more coordination than switching when you pay premiums directly, but the process becomes straightforward when you follow the proper sequence. Start early, communicate clearly with both your new insurer and your mortgage servicer, and verify each step before proceeding to the next.

The key is treating your lender as an equal partner in the transaction rather than an afterthought. They control the payment mechanism and have contractual rights to approve your coverage. Submit complete documentation well before your effective date, follow up to confirm receipt and approval, and verify they've updated their payment systems before canceling your old policy.

Most switching problems stem from rushed timelines or skipped steps. The borrower who shops for quotes on December 28th and wants coverage January 1st will face complications—servicers need processing time, especially during holiday periods. The homeowner who cancels existing coverage before confirming their lender accepted the replacement creates unnecessary risk.

Your insurance protects your largest asset and your lender's collateral. Taking time to coordinate the change properly prevents coverage gaps, escrow shortages, and the headache of force-placed insurance. The few weeks invested in doing it right save months of cleanup work and potential financial losses.

When you've completed the switch, keep documentation organized: confirmation from your new insurer showing the effective date and coverage details, written confirmation from your lender accepting the new policy, and cancellation confirmation from your old insurer showing the refund amount sent to escrow. If escrow accounting questions arise months later, these documents resolve disputes quickly.

Switching insurance becomes routine once you understand the mechanics. Whether you're chasing better rates, seeking improved coverage, or replacing an insurer who non-renewed your policy, the same systematic approach ensures your home stays protected, your lender stays satisfied, and your escrow account transitions smoothly between carriers.