Flat lay of homeowners insurance policy document, cancellation letter, house keys, calculator, and small house model on wooden desk

How to Cancel Homeowners Insurance Without Coverage Gaps or Penalties

Content

Most homeowners don't realize that cancellation methods vary significantly based on why you're canceling and who initiates it. A policy you cancel mid-term because you found cheaper coverage will be handled differently than one you're ending because you sold your property. Understanding these distinctions helps you avoid unnecessary fees and ensures you maintain the continuous coverage that keeps your rates competitive.

When You Can (and Can't) Cancel Your Homeowners Insurance

Timing your cancellation involves more than picking a convenient date. Legal restrictions, contractual obligations, and lender requirements all play a role in determining when you're actually free to terminate coverage.

Mortgage requirement restrictions

If you carry a mortgage, your lender holds significant control over your insurance decisions. The mortgage agreement you signed includes a hazard insurance clause requiring continuous coverage until the loan is paid off. Your lender receives notice whenever your policy is canceled or lapses, and they're legally entitled to force-place expensive coverage on your home if you fail to maintain adequate protection.

Force-placed insurance typically costs 2-3 times more than standard policies and offers minimal coverage. Worse, the lender adds this premium to your mortgage balance, and you're powerless to shop for better rates. Before canceling, you must provide your mortgage servicer with proof of replacement coverage showing the same or better limits and naming them as the mortgagee.

Some lenders require 30-45 days advance notice of any insurance changes. Check your mortgage documents or call your servicer directly to understand their specific requirements. Refinancing situations add another layer of complexity—your new lender needs proof of coverage before closing, creating a narrow window where you'll need overlapping policies.

The biggest mistake homeowners make is canceling their existing policy before securing new coverage. Even a single day without protection can create a lapse that follows you for years, increasing premiums by 10-20% or more

— Jennifer Hartman

State-specific cancellation windows

Insurance regulations vary by state, but most follow similar frameworks. California, for example, requires insurers to provide 75 days notice for non-renewal but allows policyholders to cancel anytime with proper notice. Florida mandates that insurers accept cancellation requests but may charge short-rate penalties depending on how much of the policy term has elapsed.

Many states enforce a "free-look period"—typically 10-30 days from policy inception—during which you can cancel for a full refund with no questions asked. This cooling-off period protects consumers who feel pressured into purchases or discover better options immediately after buying.

Certain states prohibit mid-term cancellations during wildfire or hurricane seasons unless you're selling the property or the home is uninhabitable. These emergency restrictions prevent mass cancellations that would destabilize the insurance market during high-risk periods.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Required Steps to Cancel Your Homeowners Policy

The cancellation process follows a specific sequence. Skipping steps or handling them out of order creates delays and potential coverage gaps.

Contacting your insurance company

Start by calling your insurance company or agent directly. Ask about their specific cancellation requirements, potential penalties, and refund calculations. Request the exact forms or documentation they need and clarify whether they accept email submissions or require postal mail.

During this call, confirm your policy number, current premium amount, and renewal date. Ask whether you're within any minimum earned premium period—some insurers require you to keep coverage for at least 60-90 days before allowing cancellation without steep penalties.

Document everything. Write down the representative's name, date, time, and a summary of what they told you. This record becomes crucial if disputes arise later about what was communicated or promised.

Submitting written cancellation notice

Phone calls alone don't cancel policies. Insurance companies require written notice to create an official record and protect both parties. Your written request should include:

- Your full name and policy number

- Property address covered by the policy

- Requested cancellation date (must be future-dated, typically at least 5-30 days out)

- Reason for cancellation

- Your signature and date

- Contact information for follow-up

Send this request via certified mail with return receipt, or use your insurer's online portal if available. Email works for some companies, but always request written confirmation that they received and processed your request. Keep copies of everything.

Never assume verbal confirmations are sufficient. One homeowner discovered this the hard way when her "canceled" policy continued billing her for eight months because the company claimed they never received written notice, despite her phone call notes.

Timing your cancellation date

Choose your cancellation date strategically. If you're switching providers, overlap coverage by at least one day rather than trying to match effective dates exactly. This buffer prevents gaps if your new policy experiences processing delays.

For property sales, coordinate the cancellation date with your closing date. Cancel effective the day after closing—not before. If the sale falls through, you'll still have coverage. You can always adjust the cancellation date later if needed.

Avoid canceling on the first of the month unless necessary. Many insurers process cancellations in batches, and month-end requests sometimes get pushed to the following month, creating unintended coverage extensions and billing complications.

Obtaining proof of cancellation

Request written confirmation showing your policy was canceled, the effective date, and any refund amount owed. This documentation proves you're not carrying duplicate coverage and protects you if billing errors occur.

Your cancellation confirmation should arrive within 10-15 business days. If it doesn't, follow up immediately. Some mortgage servicers require this proof within specific timeframes, and delays can trigger force-placed insurance.

Save cancellation confirmations for at least seven years. You may need them for tax purposes, future insurance applications, or if claims arise from incidents that occurred while the policy was active but weren't reported until after cancellation.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Documents and Information You'll Need

Gathering the right paperwork before starting the cancellation process prevents delays and back-and-forth communications. Create a checklist:

Essential documents: - Current policy declarations page showing policy number and coverage dates - Mortgage account number and servicer contact information - New insurance policy declarations page (if switching providers) - Government-issued ID matching the name on the policy - Written cancellation request letter

Information to have ready: - Exact cancellation date you're requesting - Forwarding address for refund checks - Reason for cancellation (affects refund calculations) - Any outstanding premium balances or payment plan details - Names of all policyholders if jointly held

For specific situations: - Home sale: closing date and buyer information - Divorce: court order specifying insurance responsibilities - Death of policyholder: death certificate and executor documentation - Property damage: adjuster contact and claim numbers

Keep digital and physical copies of everything. Cloud storage ensures you can access documents from anywhere if questions arise during the cancellation process.

Refunds, Penalties, and Fees: What to Expect When Canceling

How much money you get back—or whether you owe additional fees—depends entirely on who initiates the cancellation and when it occurs during your policy term.

| Cancellation Scenario | Refund Method | Typical Refund % | Processing Time |

| Policyholder-initiated mid-term | Short-rate (penalty) | 85-90% of unused premium | 15-30 days |

| Switching providers | Pro-rated (no penalty) | 100% of unused premium | 10-20 days |

| Sold home | Pro-rated (no penalty) | 100% of unused premium | 10-20 days |

| Company-initiated | Pro-rated (no penalty) | 100% of unused premium | 20-30 days |

| Within free-look period | Full refund | 100% of all premiums paid | 7-14 days |

Pro-rated refunds calculate your refund by dividing the annual premium by 365, then multiplying by the number of unused days. If you paid $1,200 annually and cancel with 200 days remaining, you'd receive approximately $658 back ($1,200 ÷ 365 × 200).

Short-rate penalties reduce your refund by 10-15% as an administrative fee for early cancellation. Using the same example, a 10% penalty would drop your refund to about $592. These penalties only apply when you initiate cancellation without qualifying reasons like home sales.

Some insurers charge minimum earned premiums, keeping 25-35% of the annual premium regardless of when you cancel. A policy with $1,200 annual premium and 25% minimum earned premium means the company keeps $300 even if you cancel after one month. This practice is less common but still exists, particularly with non-standard insurers.

Payment plans complicate refunds. If you pay monthly and cancel mid-term, the insurer calculates the refund based on the full annual premium, then subtracts what you've already paid plus any installment fees. You might owe money instead of receiving a refund if you're behind on payments or if fees exceed the unused premium value.

Escrow accounts add another layer. If your mortgage servicer pays your insurance through escrow, refunds go to them, not you. The servicer deposits the refund into your escrow account, which may reduce future monthly payments or result in an escrow refund check during the annual analysis.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Avoiding Coverage Gaps When Switching Insurance Providers

Coverage gaps—even brief ones—create problems that persist for years. Insurers view gaps as red flags indicating higher risk, and many will either decline coverage or charge significantly more if you've had lapses within the past three years.

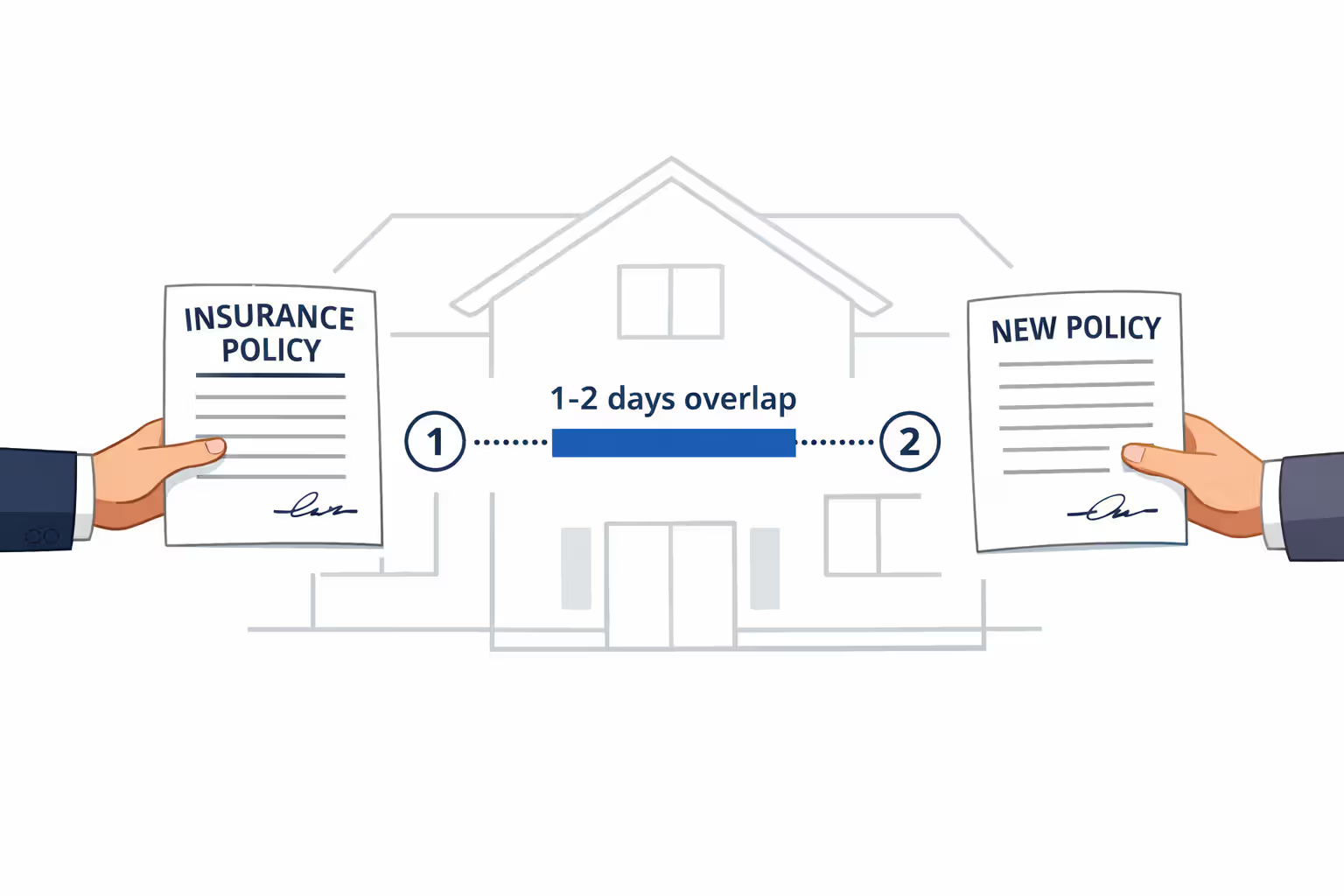

The overlap strategy is simple but effective: purchase your new policy with an effective date 1-2 days before canceling your old one. Yes, you'll pay for duplicate coverage briefly, but this costs far less than the premium increases you'd face from a documented lapse.

Bind your new policy completely before initiating cancellation. "Binding" means you've paid the first premium and received written confirmation of coverage. Quotes and applications aren't binding—they can be withdrawn or modified. One homeowner learned this when her "approved" application was rescinded after an inspection revealed roof damage, leaving her scrambling to keep her old policy active.

Coordinate timing carefully during home purchases. Your new policy should take effect at closing, not before. Insuring a home you don't own yet creates title issues and potential claim complications. Your old home's policy should remain active until ownership transfers.

For mortgage-required coverage, provide your lender with the new policy information before canceling the old one. Most servicers need 5-10 business days to update their records. Canceling first can trigger automatic force-placed insurance, even if your new policy is already active.

Set phone reminders for the cancellation effective date. Verify with both insurers that the transition occurred as planned. Mistakes happen—systems fail, paperwork gets lost, and miscommunications occur. A five-minute confirmation call prevents coverage gaps that could cost thousands.

Author: Marcus Hollowell;

Source: sixth-fleet.com

Common Mistakes That Delay or Complicate Cancellation

Learning from others' errors saves time and money:

Canceling before securing replacement coverage. The most frequent and costly mistake. Insurance companies share lapse information, and a gap on your record increases premiums with every future insurer.

Assuming verbal confirmations are sufficient. Insurance is a written contract business. Without documentation, you have no proof of what was agreed upon or when.

Missing payment deadlines during the cancellation process. If your cancellation date is the 15th but your payment is due on the 10th, you still owe that payment. Missing it can result in automatic cancellation with penalties, rather than the voluntary cancellation you requested.

Forgetting to notify the mortgage servicer. Your insurer doesn't automatically inform your lender about replacement coverage. That's your responsibility, and failure to provide proof triggers force-placed insurance.

Canceling too close to the renewal date. Insurers typically send renewal notices 30-45 days early. If you cancel within that window, you may still be charged for the renewed term, requiring a second cancellation and creating refund complications.

Not accounting for outstanding claims. You can cancel a policy with an open claim, but the cancellation doesn't close the claim. The old insurer continues handling it, but you lose leverage if disputes arise. When possible, resolve claims before canceling.

Ignoring state-specific notice requirements. Some states require 30 days notice; others accept same-day cancellations. Using the wrong timeframe can result in denied cancellation requests or unexpected premium charges.

Frequently Asked Questions About Canceling Homeowners Insurance

Moving Forward With Your Cancellation

Canceling homeowners insurance demands attention to detail and proper sequencing, but the process becomes straightforward when you understand the requirements and potential pitfalls. Start by securing replacement coverage if needed, then submit written cancellation notice with appropriate lead time. Maintain documentation of every step, confirm the cancellation with both your insurer and mortgage servicer, and verify that refunds arrive as expected.

The consequences of rushed or improper cancellation—coverage gaps, penalties, force-placed insurance, and increased future premiums—far outweigh the minimal effort required to do it correctly. Take the time to follow each step methodically. Your financial protection and peace of mind depend on maintaining continuous, appropriate coverage throughout any transition.

Whether you're switching providers for better rates, selling your home, or consolidating policies, treat cancellation as a formal process requiring the same care you'd give to any significant financial decision. The few hours invested in proper cancellation procedures protect you from complications that could persist for years and cost thousands of dollars in increased premiums and penalties.