Suburban house in wildfire-prone area with denied insurance policy document and distant wildfire smoke on horizon

Can You Just Get Fire Insurance on Your Home Without Full Coverage?

Content

Homeowners facing coverage denials or living in wildfire-prone areas often ask whether they can skip comprehensive insurance and purchase fire protection alone. The short answer: yes, but your options are limited, and the coverage comes with significant trade-offs that most people don't anticipate until it's too late.

Standalone fire insurance exists primarily through state-mandated programs designed as a last resort for properties that can't secure traditional coverage. Understanding when this option makes sense—and when it creates dangerous gaps in protection—requires looking beyond premium costs to examine what you're actually buying.

What Is Fire-Only Insurance and How Does It Differ from Standard Homeowners Policies?

Fire-only insurance policies provide coverage exclusively for fire-related perils, typically including smoke damage and sometimes lightning strikes. Unlike a standard HO-3 homeowners policy that covers your dwelling, personal property, liability, and additional living expenses against a broad range of perils, fire-only policies function as bare-bones protection.

The distinction matters more than most buyers realize. A comprehensive homeowners policy operates on an "open perils" basis for your dwelling, meaning it covers everything except specifically excluded events. Fire-only coverage flips this approach, protecting only against the named peril of fire while leaving you exposed to theft, vandalism, wind damage, falling objects, and dozens of other risks that could destroy your home or drain your savings.

Coverage Scope: Fire-Only vs. Comprehensive Homeowners Insurance

A standard HO-3 policy bundles six coverage types: dwelling protection, other structures, personal property, loss of use, personal liability, and medical payments to others. Fire-only policies typically cover just the dwelling itself against fire damage, with optional add-ons available in some cases.

This means if a visitor slips on your front steps and sues, you're paying out of pocket. If a pipe bursts and floods your basement, you're covering the repair costs yourself. If someone breaks in and steals your belongings, there's no reimbursement. The policy responds only when fire causes the loss.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Who Typically Offers Standalone Fire Policies

Standard insurance carriers rarely sell true fire-only policies because the risk concentration makes them unprofitable. Instead, these policies come primarily from state FAIR Plans (Fair Access to Insurance Requirements), which operate as insurers of last resort in 30+ states.

Some surplus lines carriers also offer limited peril policies in specific markets, though these often include a few additional perils beyond fire. Dwelling fire policies (DP-1 forms) represent another option, covering fire plus a handful of other named perils like lightning, windstorm, and hail—making them slightly broader than pure fire-only coverage.

When Can You Purchase Standalone Fire Insurance Instead of Full Coverage?

The availability of fire-only insurance depends heavily on your circumstances and location. Most people can't simply choose this option as a cost-saving measure; it exists primarily for situations where comprehensive coverage is unavailable or impractical.

Homes in High-Risk Fire Zones

Properties located in wildfire-prone areas—particularly those in California's WUI (wildland-urban interface) zones, Colorado's mountain communities, or similar high-risk regions—increasingly face non-renewals from traditional carriers. When standard insurers exit these markets, FAIR Plans become the primary option for maintaining any coverage at all.

California's FAIR Plan, for instance, has grown from roughly 100,000 policies in 2015 to over 400,000 by 2023, reflecting the state's wildfire crisis. Homeowners in these areas often can't get fire insurance on their home through normal channels, making state programs their only viable path to meeting lender requirements.

Properties Denied Traditional Coverage

Homes with poor claims history, outdated electrical systems, old roofs, or other risk factors may receive denials from multiple standard carriers. A property with knob-and-tube wiring, for example, might get rejected by every major insurer in the state, leaving FAIR Plan coverage as the sole option.

FAIR Plans were never intended to be permanent solutions or competitive alternatives to the standard market. They exist to provide a safety net when the private market won't write coverage, giving homeowners basic protection while they work to improve their property's insurability

— Janet Ruiz

Properties in coastal flood zones sometimes face similar challenges, though flood damage requires separate federal flood insurance regardless of your homeowners policy type.

Vacant or Secondary Properties

Vacation homes, rental properties between tenants, or homes undergoing renovation often need coverage but don't qualify for standard homeowners policies. Some owners opt for fire-only coverage during these periods, though dwelling fire policies usually offer better value for these situations.

A cabin used only during summer months might not justify the cost of comprehensive coverage, especially if you've removed all valuable contents. Fire-only insurance provides basic protection against total loss without paying for liability coverage you're not using.

Author: Ethan Caldwell;

Source: sixth-fleet.com

What Does Fire-Only Insurance Actually Cover (And What It Doesn't)?

Understanding the coverage boundaries prevents nasty surprises when filing a claim. Fire-only policies respond to direct fire damage and resulting smoke damage to your dwelling structure. Some policies extend to detached structures like garages or sheds, but you'll need to verify this specifically.

The coverage typically includes: - Physical damage to your home's structure caused by fire - Smoke and soot damage resulting from the fire - Fire department service charges in some policies - Debris removal related to fire damage

What fire-only policies almost universally exclude creates the real problem. You're unprotected against theft, vandalism, windstorms, hail, falling objects, water damage from burst pipes, ice dam damage, and liability claims. If your neighbor's tree falls on your roof during a storm, you're paying for repairs. If your water heater fails and floods your finished basement, that's entirely your financial burden.

Personal property coverage—your furniture, electronics, clothing, and other belongings—generally isn't included or comes with extremely low limits. Additional living expenses if fire makes your home uninhabitable may have minimal coverage or none at all, forcing you to pay hotel costs out of pocket during reconstruction.

| Coverage Type | Fire-Only/FAIR Plan | Standard HO-3 Policy |

| Fire/smoke damage | ✓ Covered | ✓ Covered |

| Wind/hail | ✗ Not covered | ✓ Covered |

| Theft/vandalism | ✗ Not covered | ✓ Covered |

| Liability protection | ✗ Not included | ✓ $100K-$500K+ |

| Additional living expenses | Limited or ✗ | ✓ Typically 20-30% of dwelling |

| Personal property | ✗ or very limited | ✓ 50-70% of dwelling |

| Medical payments | ✗ Not included | ✓ $1K-$5K typical |

| Water damage (non-flood) | ✗ Not covered | ✓ Covered |

How Much Does Fire Insurance Cost Compared to Full Homeowners Coverage?

Contrary to common assumptions, fire-only insurance doesn't necessarily cost significantly less than comprehensive coverage. FAIR Plan premiums often run 50-80% of what a standard policy would cost, while providing only a fraction of the protection.

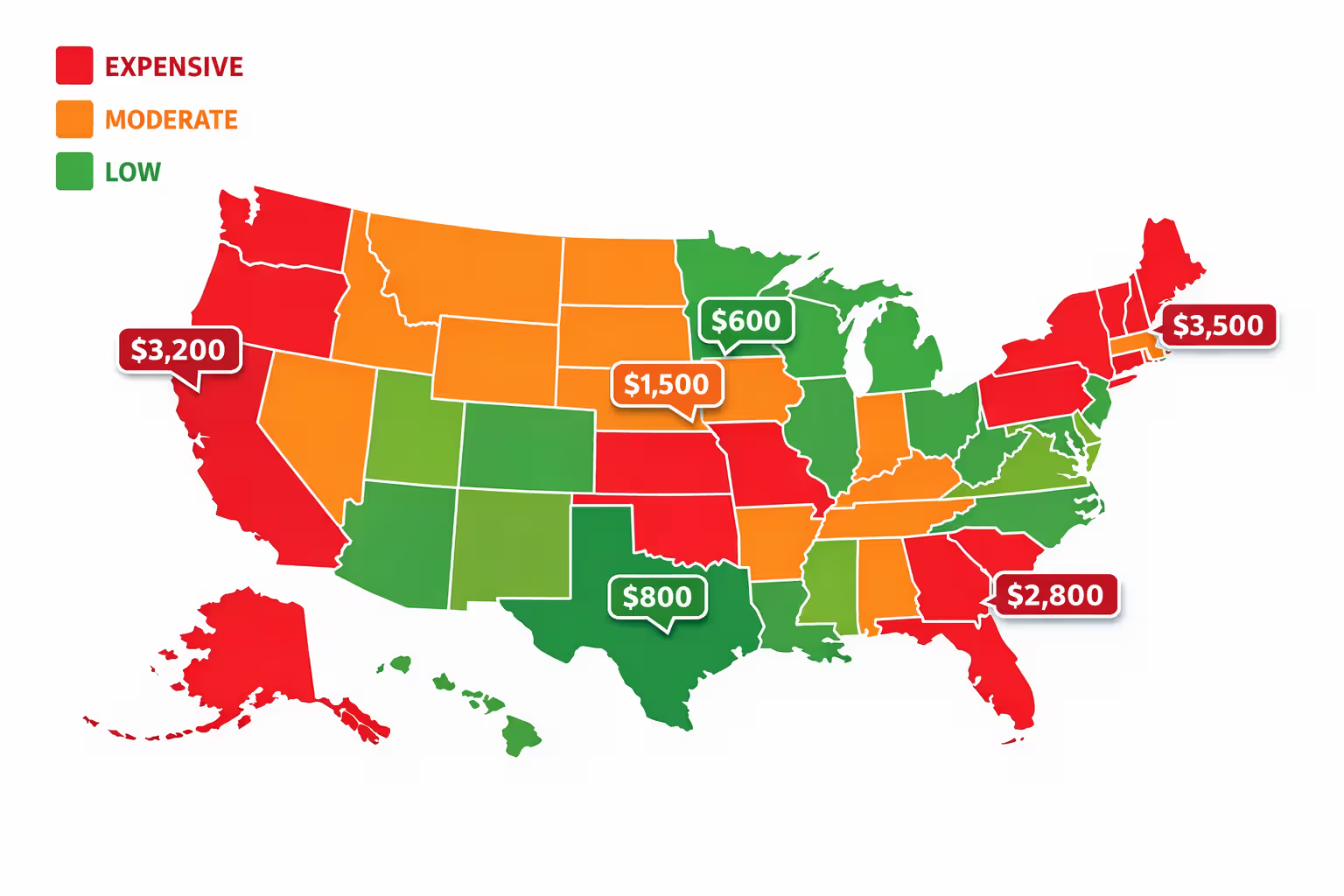

A $300,000 home in California might pay $2,400 annually for a FAIR Plan fire policy, compared to $3,200 for a comprehensive HO-3 policy from a standard carrier—if one were available. That seemingly modest savings disappears quickly when you consider the missing liability protection, theft coverage, and protection against other perils.

Premium Factors for Fire-Only Policies

FAIR Plans calculate premiums based on dwelling replacement cost, location, construction type, and fire protection class (distance to fire hydrants and fire stations). Unlike standard policies, your credit score and claims history typically matter less, since FAIR Plans can't reject applicants who meet basic eligibility requirements.

Deductibles on fire-only policies tend to be higher than standard policies, often starting at $2,500 or 2% of the dwelling coverage amount. This shifts more financial risk to you, partially offsetting the premium savings.

State FAIR Plan Pricing Examples

Pricing varies dramatically by state. California's FAIR Plan tends to be among the most expensive due to extreme wildfire exposure, while states with lower fire risk charge considerably less. A comparable home might pay $1,800 in Texas but $3,500 in California for similar FAIR Plan coverage.

Coverage limits also vary by state. California caps FAIR Plan coverage at $3 million, while some states limit policies to $500,000 or less. If your home's replacement cost exceeds your state's FAIR Plan limit, you'll need a supplemental policy to bridge the gap—adding complexity and cost.

Author: Ethan Caldwell;

Source: sixth-fleet.com

State FAIR Plans: Your Primary Option for Fire-Only Coverage

FAIR Plans operate in over 30 states, each with its own rules, coverage limits, and pricing structures. These state-mandated programs require insurers licensed in the state to participate proportionally based on their market share, spreading the risk across the industry.

The programs function as true insurers of last resort. You can't simply choose a FAIR Plan because you prefer it; you must demonstrate that you've been unable to obtain coverage from at least one (sometimes two or three) standard market insurers. This requirement prevents adverse selection that would destabilize the program.

How to Apply for a FAIR Plan Policy

The application process starts with obtaining formal declinations from standard carriers. Some states require written denial letters, while others accept verbal confirmations. You'll then complete a FAIR Plan application, typically available through insurance agents or directly from the state FAIR Plan association.

An inspection usually follows, evaluating your property's condition, fire hazards, and compliance with basic safety requirements. Properties with severe hazards—like overgrown vegetation against the structure, exposed wiring, or non-functional smoke detectors—may need corrections before approval.

Processing takes anywhere from two weeks to 60 days depending on the state and inspection scheduling. Once approved, coverage typically begins immediately upon payment, though some states impose waiting periods for certain perils.

Coverage Limits and Restrictions by State

Each state's FAIR Plan operates independently with unique rules. California allows up to $3 million in dwelling coverage and recently expanded to include limited personal property and additional living expenses. Florida's plan covers up to $700,000, while Louisiana caps coverage at $500,000.

Some states restrict FAIR Plans to fire-only coverage, while others include additional perils like windstorm, hail, or vandalism. Texas, for example, offers broader coverage than pure fire-only policies, making it closer to a limited dwelling fire policy.

Most FAIR Plans exclude flood, earthquake, and earth movement regardless of state. You'll need separate policies for these perils, which can create coverage coordination challenges and additional premium expense.

Alternatives to Fire-Only Insurance When You Need More Protection

Before settling for fire-only coverage, explore these options that might provide better value and more comprehensive protection.

Dwelling fire policies (DP-1 or DP-3 forms) cover fire plus additional named perils. A DP-1 typically includes fire, lightning, and internal explosion, while DP-3 adds windstorm, hail, explosion, riot, aircraft, vehicles, smoke, vandalism, theft, and falling objects. These policies cost more than fire-only coverage but substantially less than leaving yourself exposed to common perils.

Surplus lines carriers specialize in hard-to-place risks and may offer coverage when standard markets won't. These non-admitted insurers aren't subject to the same rate regulations, allowing them to price risk more flexibly. Premiums run higher than standard market rates, but you get legitimate comprehensive coverage rather than fire-only protection.

Some homeowners successfully combine a FAIR Plan base policy with a "wraparound" or "difference in conditions" (DIC) policy from a standard or surplus carrier. The FAIR Plan covers fire, while the DIC policy adds liability, theft, and other perils. This approach costs more than fire-only coverage but less than being completely self-insured for non-fire perils.

Risk mitigation investments sometimes restore eligibility for standard coverage. Installing a Class A fire-resistant roof, creating defensible space around your property, upgrading electrical systems, or replacing old plumbing can convince insurers to reconsider coverage. The upfront cost may be substantial, but it can pay off through better coverage options and lower long-term premiums.

Common Mistakes When Shopping for Fire Insurance

Author: Ethan Caldwell;

Source: sixth-fleet.com

Buyers frequently underestimate the financial exposure that fire-only coverage creates. Saving $800 annually on premiums seems attractive until you face a $15,000 theft loss or a $50,000 lawsuit from an injured visitor—both completely uncovered by your fire-only policy.

Assuming fire represents your biggest risk is another error. Statistics show that theft, water damage, and liability claims occur far more frequently than total fire losses for most homes. You're optimizing for the wrong scenario if you protect only against fire while leaving yourself exposed to more probable events.

Many buyers fail to read the actual policy language, discovering too late that their "fire insurance" doesn't cover additional living expenses during reconstruction. Paying out of pocket for six months of hotel stays and restaurant meals while your fire-damaged home is rebuilt can cost $30,000-$50,000—far exceeding years of premium savings.

Not shopping dwelling fire policies alongside fire-only options means missing potentially better value. A DP-1 policy might cost only 15-20% more than fire-only coverage while adding meaningful protection against lightning, internal explosions, and other perils you'd otherwise self-insure.

Ignoring the mortgage requirement implications creates problems too. Some lenders specifically require comprehensive coverage and won't accept fire-only policies. Verify your lender's requirements before purchasing limited coverage that doesn't satisfy your loan agreement.

FAQ: Fire-Only Insurance Questions Answered

Fire-only insurance serves a specific purpose: providing basic dwelling protection when comprehensive coverage is unavailable or when you're willing to self-insure all other risks. For homeowners in wildfire zones facing standard market denials, FAIR Plans offer essential protection that beats going completely uninsured.

The decision requires honest assessment of your financial capacity to absorb non-fire losses. Can you replace your belongings after a theft? Pay for six months of temporary housing? Cover a $100,000 liability judgment? If these scenarios would create financial hardship, fire-only coverage leaves you dangerously exposed.

Before committing to fire-only insurance, exhaust alternatives: get quotes for dwelling fire policies, explore surplus lines carriers, investigate what property improvements might restore standard market eligibility, and price out supplemental policies to fill coverage gaps. The comprehensive approach takes more effort but usually delivers better protection per dollar spent.

For properties in extreme risk areas where no alternatives exist, FAIR Plans provide critical safety net coverage. Just understand exactly what you're buying—and more importantly, what you're not buying. Document your uncovered exposures, maintain adequate emergency savings to handle non-fire losses, and continue seeking opportunities to transition back to comprehensive coverage when market conditions improve.