Suburban house roof with hail damage showing cracked asphalt shingles and scattered granules with golf-ball-sized hailstones on the ground and stormy sky

Does Homeowners Insurance Cover Hail Damage to Your Roof and Home

Content

Last spring, a hailstorm tore through my neighbor's subdivision at 3 p.m. on a Tuesday. By 3:15, her roof had taken a beating from golf ball-sized ice. By Thursday, she'd learned her 14-year-old roof would only get depreciated value—about 60% of what replacement would actually cost.

Here's the thing: your homeowners policy probably covers hail damage, but "covered" doesn't always mean "fully paid." The money you actually receive hinges on your specific policy language, how old your damaged components are, and whether you live in a state where insurers have quietly added restrictions over the past few years.

Let's break down exactly what happens when hail hammers your house and you need to file a claim.

How Standard Homeowners Insurance Policies Handle Hail Damage

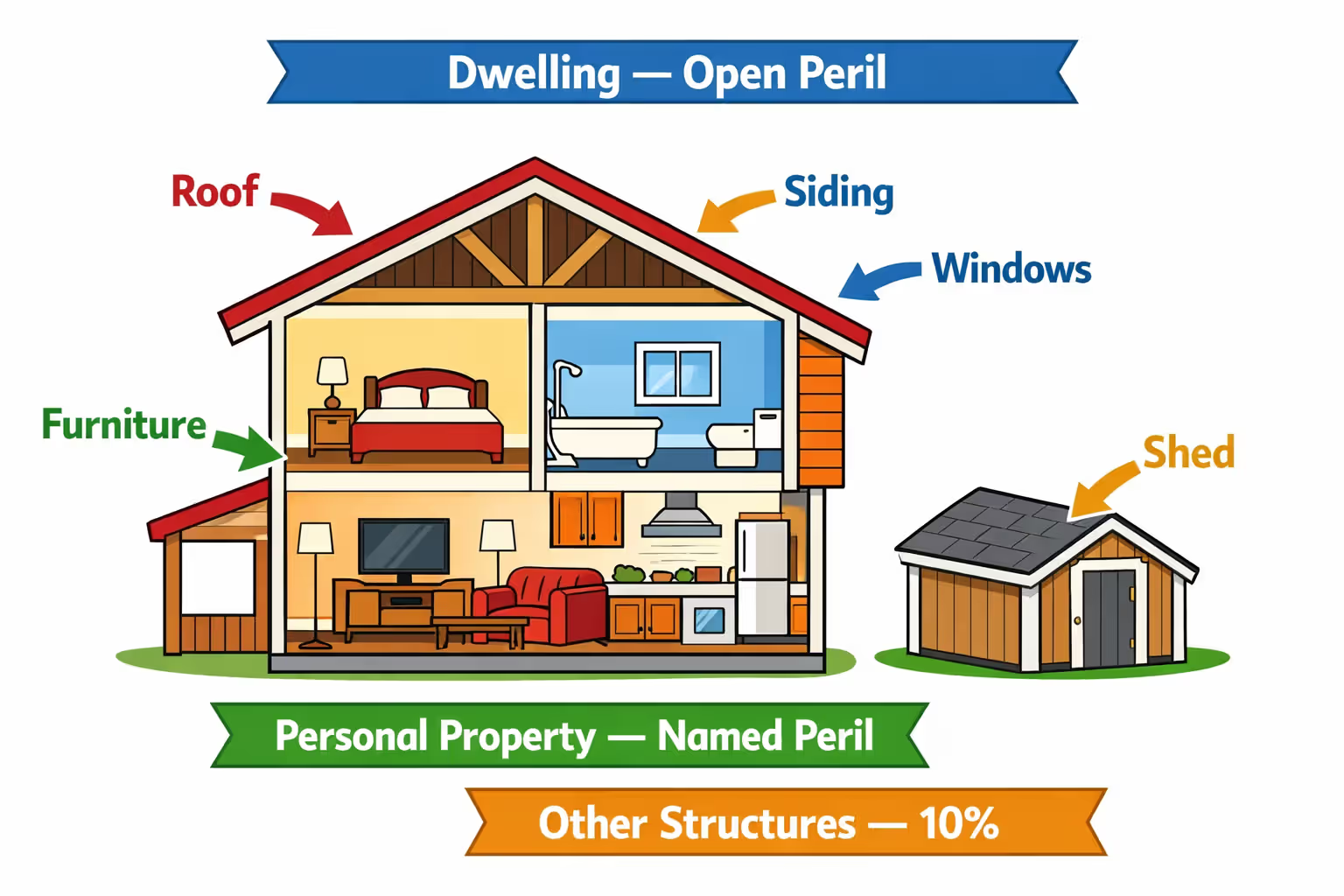

About 85% of American homeowners own an HO-3 policy. This "special form" policy treats your house itself as covered against basically everything except what's specifically excluded in the fine print. Your stuff inside? That works differently—only certain disasters make the list, though hail happens to be one of them.

Your home's structure gets what insurers call "open peril" protection. Hail cracks your roof tiles or punches through vinyl siding? Covered. The personal belongings in your house fall under "named peril" protection—they're only covered for specific disasters spelled out in your policy documents. Fortunately, hail appears on every standard list alongside fire, theft, and windstorms.

Here's where it gets interesting. The dwelling section typically insures your home for its full replacement value. Personal property? Usually maxed at 50% to 70% of whatever your house is insured for. If you've got $300,000 in dwelling coverage, expect around $150,000 to $210,000 available for your belongings.

These limits matter more than you'd think when a severe hailstorm tears through your neighborhood, breaking windows, damaging furniture through those broken windows, destroying outdoor equipment, and wrecking your roof all at once.

Author: Samantha Kessler;

Source: sixth-fleet.com

What "Named Peril" vs. "Open Peril" Means for Hail Coverage

Think of "open peril" as guilty-until-proven-innocent for insurance companies. Unless your policy explicitly says "we won't pay for this," they're on the hook. Your house gets this VIP treatment, which is why hail damage gets covered automatically—you won't find "hail exclusion" clauses in standard policies.

"Named peril" flips the script. Your personal property only gets paid for if the damage came from one of the specific disasters listed in your policy. Good news: every carrier includes hail on that list, right there with lightning strikes and vandalism.

But watch out for secondary damage. Hail shatters your skylight, rain pours in for six hours before you get home from work, and now your hardwood floors are buckling. The skylight's definitely covered. Those floors? You'll need to prove you couldn't have prevented the water damage, which gets complicated if the adjuster thinks you should've tarped things faster.

Coverage Limits and Depreciation Factors

Your insurance payout gets calculated one of two ways, and the difference can cost you thousands.

Replacement Cost Value pays whatever it actually costs to fix or replace something today, using current prices and similar quality materials. A $15,000 roof repair gets you $15,000 (minus your deductible).

Actual Cash Value subtracts depreciation first. That same $15,000 roof installed twelve years ago might only net you $7,500 after the insurance company deducts for age and wear.

Most policies automatically use RCV for your dwelling but default to ACV for your personal property unless you've paid extra for a replacement cost endorsement. Read your declarations page carefully.

Then there's your deductible. Standard deductibles run from $1,000 to $2,500 as a flat dollar amount. But in hail-heavy states, insurers increasingly push "percentage deductibles" specifically for wind and hail claims—sometimes 2%, sometimes 5% of your total dwelling coverage.

Quick math: 5% deductible on a $400,000 policy means you're paying the first $20,000 yourself. Every single time hail strikes.

Which Parts of Your Home Are Protected When Hail Strikes

Hail pummels everything it can reach. Your insurance responds differently depending on what got hit.

Your roof takes the worst beating. Asphalt shingles get pockmarked and lose their protective granules. Wood shakes split down the middle. Metal roofing dents but usually keeps working. All of this falls under your dwelling coverage, though we'll dig into roof-specific complications in a minute.

Siding damage—whether vinyl cracks, aluminum dents, or fiber cement chips—also gets covered through your dwelling protection. Just know that "cosmetic damage" endorsements (increasingly common in Texas, Oklahoma, and Colorado) might limit what you actually collect.

Broken windows and shattered skylights? Dwelling coverage pays for the glass and any water damage that happens before you can reasonably protect your home's interior. The key word is "reasonably"—if you wait three days while rain pours in, expect pushback.

Gutters and downspouts get covered too, though adjusters love to argue these were already worn out. Take dated photos of your gutters before storm season if you want ammunition during claims disputes.

Detached structures like workshops, sheds, and gazebos tap into a different coverage bucket—usually 10% of your dwelling limit. A $300,000 house carries $30,000 for detached structures. Multiple buildings? They share that pool of money.

Your patio furniture, grill, and kids' swing set fall under personal property coverage, which probably uses ACV unless you've upgraded. And your car in the driveway? That's an auto insurance problem, not homeowners—you'll need comprehensive coverage on your vehicle policy.

| What Got Damaged | Does Insurance Respond? | Which Coverage Section | Watch Out For |

| Roof shingles and decking | Yes | Dwelling | Switches to depreciated value after 10-15 years; cosmetic-only clauses |

| Exterior siding | Yes | Dwelling | Cosmetic exclusions increasingly common |

| Broken glass (windows, doors) | Yes | Dwelling | You must protect interior from further rain damage |

| Gutters and trim | Yes | Dwelling | Adjusters often claim pre-existing deterioration |

| Separate garage or shed | Yes | Other Structures | Capped at 10% of your dwelling limit |

| Wooden deck or privacy fence | Yes | Other Structures | Heavy scrutiny on maintenance and age |

| Air conditioning condenser | Yes | Dwelling | Functional damage covered; dents might not be |

| Outdoor furniture and grills | Yes | Personal Property | Depreciated value unless you bought RCV endorsement |

| Your car or truck | No | Auto Insurance | Requires comprehensive auto coverage |

| Above-ground pool | Yes | Other Structures | Only the structure; water isn't covered |

| Trees and plants | Limited | Special Coverage | Usually capped at 5% of dwelling; $500-$1,000 per plant |

Common Exclusions and Situations Where Hail Damage Won't Be Covered

Insurers reject hail claims more often than most homeowners realize, especially in states hammered by repeated storms.

Pre-existing deterioration ranks as the number one denial reason. Your roof was already falling apart, missing shingles, showing rot? The adjuster will photograph every worn spot and argue the hail just finished what time had started. They're not obligated to restore something that was already failing.

Neglected maintenance creates similar headaches. You've ignored those loose shingles for three years, then hail makes it worse, then water pours into your attic. The insurer covers the fresh hail impacts, not the damage that resulted from your failure to maintain the roof properly.

"Cosmetic damage" clauses have exploded across hail-prone markets. These endorsements—sometimes slipped into your renewal without much fanfare—eliminate or severely restrict coverage for damage that doesn't affect how something works. Gutters with dents that still drain water? Siding with dimples that still protects your walls? You might get nothing, even though your home looks terrible.

Age-based roof limitations are becoming standard operating procedure. Many policies in Colorado, Texas, and Oklahoma automatically downgrade your roof to depreciated value once it hits its tenth birthday. Some insurers won't touch roofs older than 20 years at any price. Others will insure your home but exclude wind and hail coverage entirely if your roof's too old.

Gradual damage doesn't count. Hail creates minor damage, you don't notice it, water seeps in over the next four months and ruins your ceiling. The insurer pays for the initial impact points they can identify, not the slow-motion deterioration you should have caught and fixed.

Material changes you didn't report can void your entire claim. Switched from asphalt to metal roofing without updating your policy? Added solar panels without telling your agent? Converted your attached garage to living space? Don't be surprised if your claim gets denied for "misrepresentation" or "material change in risk."

Author: Samantha Kessler;

Source: sixth-fleet.com

How to File a Hail Damage Claim and What to Expect

Act fast after a hailstorm—waiting makes everything harder.

Pull out your phone and photograph every bit of damage you can safely reach. Shoot wide angles showing overall scope, then zoom in on individual impact points. Grab a ruler and photograph any hailstones you find before they melt (yes, adjusters actually use hail size to estimate impact force). Time-stamp everything if your camera allows it.

Call your insurer within 48 hours maximum. Earlier is better. This first call generates your claim number and assigns an adjuster to your file. Write down the claim number, the adjuster's name, their direct phone number, and ask specifically whether you're authorized to make emergency repairs if your home has active leaks.

Stop additional damage immediately. Tarp any roof holes, board up broken windows, move belongings away from active leaks. Save every receipt and photograph your temporary repairs. Your policy explicitly requires you to prevent additional damage, and failing to do so can reduce or eliminate your settlement.

An adjuster will schedule an inspection sometime in the next week, unless your area just got walloped and thousands of claims flooded in at once. After major hail events, you might wait three weeks for an inspection.

The adjuster climbs on your roof (or drones it), measures damage, takes their own photos, and creates an estimate of repair costs. This is where things get interesting.

The first estimate misses damage in probably 40% of claims I review, especially on two-story homes where the adjuster can't easily see everything. These folks work for the insurance company, not you. Get a contractor out there for a second opinion before you accept anything. I've seen $8,000 initial estimates that should've been $18,000—and were, after we pushed back

— Sarah Chen

Review every line item on the estimate. Insurance adjusters sometimes skip damage to detached buildings, undercount how many roof squares need replacement, or apply depreciation formulas that don't match your actual policy terms. Hiring a contractor for an independent assessment runs $200-$400 but frequently uncovers thousands in missed damage.

Most carriers send you an initial check for the depreciated amount minus your deductible. After you complete repairs and send them contractor invoices, they release "recoverable depreciation"—the difference between depreciated and replacement value. This two-payment system keeps insurers from paying for work you never actually do.

Straightforward claims wrap up in 30 to 60 days. Disputes over coverage scope, damage attribution, or policy interpretation can drag on for months and sometimes require formal appraisal or lawsuits.

Author: Samantha Kessler;

Source: sixth-fleet.com

Roof Damage from Hail: Special Considerations for Your Biggest Risk

Your roof represents the most expensive hail target on your property and the most complicated insurance situation you'll navigate.

Hail impacts show up as dark spots where ice crushed the protective granules on asphalt shingles, exposing the underlying material. Severe hits crack shingles completely or punch holes through. Adjusters typically mark off a 10-foot by 10-foot test square and count impacts. Eight or more impacts in that square usually triggers a full replacement recommendation—fewer means spot repairs.

The depreciation calculation matters enormously for roofs. Install your roof 15 years ago? It's depreciated by 60-75% depending on your policy. Under depreciated value coverage, you might collect $6,000 immediately on a $15,000 replacement job, with the other $9,000 coming only after you finish the work and prove it with paid invoices. Many homeowners can't front that kind of cash, so they delay repairs and the damage worsens.

Age-based limitations have become aggressive in hail country. Colorado insurers routinely flip roofs to depreciated-only coverage at the 10-year mark, regardless of condition. Texas carriers in the DFW metroplex won't even quote you if your roof's past 15 years unless you accept a wind/hail exclusion rider.

Building code requirements complicate things further. Many municipalities mandate full roof replacement when damage exceeds 25-30% of the surface area, even if hail only destroyed one slope. Insurers resist paying for code-required upgrades, claiming they only owe for the actual damaged portion. State laws vary wildly on whether carriers must cover compliance costs.

Shingle matching creates arguments too. Your particular shingle style got discontinued five years ago. The adjuster offers a cash settlement for patching the damaged section rather than replacing your entire roof to achieve uniform appearance. These settlements rarely approach what full replacement actually costs.

Your claims history affects everything. File two roof claims in five years and watch insurers either drop you entirely or exclude wind/hail at renewal. This creates brutal choices—file a claim for moderate damage and potentially lose future coverage, or eat the cost yourself to preserve insurability.

Material type matters both for damage susceptibility and coverage quality. Class 4 impact-resistant shingles resist hail better and earn premium discounts (10-30% in some states). Metal roofing dents but rarely fails functionally, though cosmetic damage clauses mean you might not get paid to fix dimpled panels. Tile and slate crack under hail but often qualify for superior coverage terms because of their expense and longevity.

Author: Samantha Kessler;

Source: sixth-fleet.com

State-Specific Differences in Hail Coverage and High-Risk Regions

Where you live determines both how often hail hits and what insurance you can actually buy.

The region from north Texas through Oklahoma, Kansas, Nebraska, and into South Dakota gets hammered hardest—meteorologists call it "Hail Alley." Colorado's Front Range along I-25 catches hell too, as do parts of Wyoming and Montana. These areas see the perfect storm of atmospheric conditions that create massive hailstones multiple times per season.

Finding coverage gets harder every year in these hot zones. Major insurers have either stopped writing new policies in Denver-area counties or pulled out of Colorado entirely. North Texas homeowners in Collin and Denton counties face shrinking options and rising premiums—the carriers that remain know they have you over a barrel.

State insurance regulations create huge coverage differences. Texas law forces insurers to offer full replacement cost for roofs, though you can decline it to save money on premiums. Colorado has no such rule, so depreciated roof coverage dominates the market. Oklahoma prohibits non-renewal based solely on hail claims unless you've filed three claims within three years.

Cosmetic damage restrictions vary by state too. Illinois banned these clauses outright in 2019 after consumer advocacy groups raised hell. Meanwhile, they're standard issue in Texas, Colorado, and Oklahoma policies.

Wind/hail deductibles play by different rules depending on your state. Florida's hurricane deductibles don't touch hail claims, but Oklahoma allows carriers to impose separate percentage deductibles for wind and hail damage up to 5% of your dwelling coverage. These deductibles apply per storm event, meaning three hailstorms in one year means three separate deductibles.

Regional pricing reflects the beating insurers take. Homeowners in Colorado's Weld County pay 40-60% more for identical coverage than folks in low-hail regions, and that's if they can find a willing insurer at all. Some carriers now require roof inspections before binding coverage in high-risk ZIP codes, then reject applicants whose roofs show any age.

State-run FAIR plans (insurers of last resort) typically exclude hail entirely or severely limit coverage, leaving homeowners who can't find private coverage exposed to their primary peril.

FAQ: Hail Damage and Homeowners Insurance

Hail coverage exists in standard policies, but the gap between what's promised and what's paid widens every year—especially in states that see frequent storms.

Insurance companies in high-risk markets have systematically reduced exposure through aggressive roof age policies, cosmetic damage endorsements, percentage deductibles sometimes reaching 5%, and claim denials based on maintenance issues.

Your strongest protection combines three approaches. First, inspect and photograph your roof every year before storm season—date-stamped photos of good condition become powerful evidence during claims disputes. Second, actually read your policy at renewal looking for new restrictive endorsements, particularly cosmetic damage clauses that may have appeared without explicit discussion. Third, document damage thoroughly and file claims fast after hailstorms hit.

Consider Class 4 impact-resistant shingles next time you replace your roof. The premium discounts (10-35% in many states) often offset the higher material cost within five to seven years while reducing future damage severity.

Shopping your coverage every two to three years prevents you from getting trapped in a policy that's been degraded through successive renewals. The insurer that offered great coverage five years ago might now impose restrictions that leave you seriously underprotected.

Understanding precisely what your policy covers—before hail destroys your roof—determines whether you'll recover financially or face thousands in unexpected costs.