Homeowners insurance policy document on wooden desk with scissors pen small house model and calculator

Can You Cancel Home Insurance at Any Time? What You Should Know

Content

Most homeowners assume they're locked into their insurance policy for a full year, but the reality is more flexible than you might think. You typically have the right to cancel your homeowners insurance whenever you choose, though several factors—including your mortgage status, state regulations, and the timing of your request—can complicate the process and affect whether it's a smart financial move.

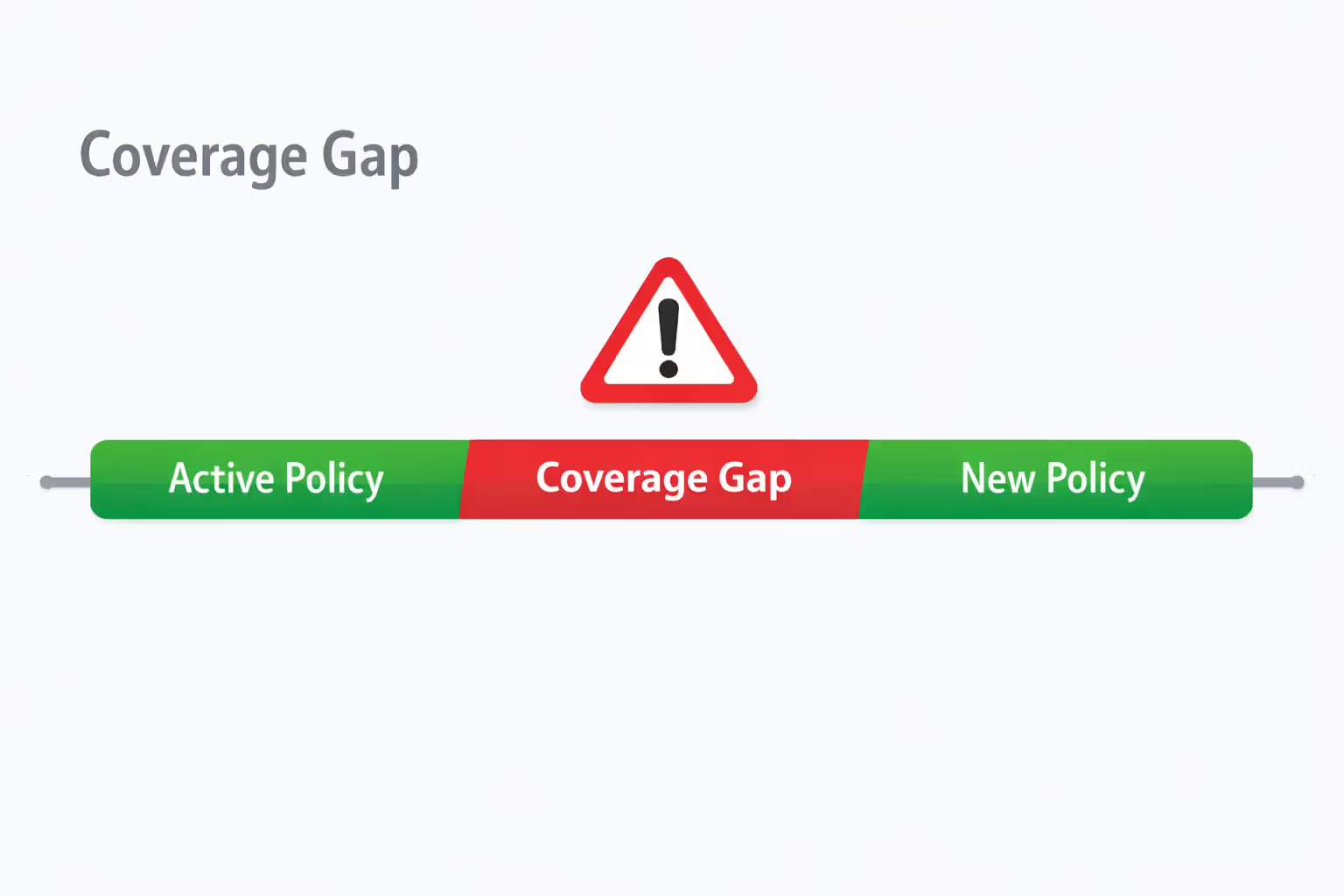

Understanding the cancellation rules, potential penalties, and proper procedures can save you hundreds of dollars and prevent dangerous coverage gaps that leave your property vulnerable.

When You're Legally Allowed to Cancel Your Homeowners Insurance

The straightforward answer: yes, you can cancel your home insurance at any time in most states. Insurance policies are generally considered voluntary contracts, and property owners maintain the right to terminate coverage when they see fit. Unlike auto insurance, which many states mandate, homeowners insurance is technically optional from a legal standpoint—though mortgage lenders have their own requirements that override this freedom.

State insurance departments across the country recognize your right to switch providers or drop coverage entirely. No law forces you to maintain a policy through its full term. However, this legal right comes with practical limitations that can make immediate cancellation difficult or inadvisable.

The biggest exception to this freedom involves mortgage obligations. If you're still paying off your home loan, your lender holds a financial interest in the property and requires continuous coverage to protect their investment. The mortgage contract you signed almost certainly includes an insurance clause requiring you to maintain adequate homeowners insurance throughout the loan term. Breaking this requirement can trigger forced-placed insurance—a much more expensive policy the lender purchases on your behalf and adds to your mortgage balance.

Some states have specific consumer protection laws that give homeowners additional cancellation rights during certain periods. For example, many states allow a "free look" period of 10 to 30 days after purchasing a new policy, during which you can cancel for a full refund without penalty. This window exists to give buyers time to review their policy documents and ensure the coverage matches what they expected.

Rules and Restrictions That May Prevent Immediate Cancellation

While you have the legal right to cancel, several practical barriers can delay or complicate the process. Understanding these restrictions helps you plan your cancellation timeline and avoid unintended consequences.

What Your Mortgage Company Requires

Mortgage lenders don't just require insurance—they require proof of continuous coverage without any gaps. When you cancel a policy, your insurance company sends a cancellation notice to your mortgage servicer. This notification triggers an immediate response from the lender's insurance tracking department.

You'll typically receive a letter giving you 30 to 45 days to provide proof of replacement coverage. If you can't demonstrate that another policy has taken effect, the lender will purchase force-placed insurance. This coverage protects only the lender's interest, not your personal belongings or liability, and can cost two to ten times more than a standard homeowners policy.

Most lenders require that replacement coverage be in place before or on the same day your old policy ends. A gap of even one day can trigger the force-placed insurance process. Some mortgage servicers are more lenient than others, but counting on their flexibility is risky.

If you own your home outright with no mortgage, you face none of these restrictions. You can cancel immediately without needing to prove replacement coverage, though doing so leaves you financially vulnerable to property damage, theft, and liability claims.

Author: Ethan Caldwell;

Source: sixth-fleet.com

State-Mandated Waiting Periods and Notice Requirements

Most states require insurance companies to provide advance notice before canceling a policy themselves, but these same requirements don't always apply when you initiate the cancellation. However, your insurance company may have internal policies requiring advance notice—typically 10 to 30 days—before they'll process your cancellation request.

This notice requirement serves several purposes. It gives the insurer time to process paperwork, calculate refunds, and notify interested parties like your mortgage company. It also protects you from impulsive decisions that might leave you uninsured.

Some insurers allow immediate cancellation if you can prove that replacement coverage is already in effect. You'll need to provide a declarations page from your new policy showing that coverage started before you're requesting the old policy to end.

State regulations also govern how insurers must handle refunds. Most states require pro-rated refunds when policyholders cancel mid-term, though the calculation method can vary. Some insurers are allowed to charge short-rate penalties—essentially an administrative fee for early cancellation—which can reduce your refund by 10% or more.

How Insurance Companies Handle Mid-Policy Cancellations

Insurance companies have standardized procedures for processing cancellations, but the financial implications vary significantly depending on who initiates the cancellation and when it occurs in the policy term.

When you cancel your policy before the term expires, you're entitled to a refund of the unused premium. However, the calculation method determines how much you'll actually receive. The two primary methods are flat cancellation (also called pro-rata) and short-rate cancellation.

Flat cancellation means the insurer calculates your refund based on the exact number of days remaining in your policy term. If you paid $1,200 for a one-year policy and cancel exactly six months in, you'd receive a $600 refund. This method is most favorable to policyholders and is required by law in many states when the policyholder initiates cancellation.

Short-rate cancellation includes a penalty fee—usually 10% of the unearned premium—as compensation for the insurer's administrative costs. Using the same example, your $600 refund would be reduced by $60, leaving you with $540. Some states allow insurers to use this method when policyholders cancel, while others prohibit it entirely.

| Cancellation Method | Who Initiates | Refund Calculation | Typical Fees | Processing Time |

| Flat (Pro-Rata) Cancellation | Policyholder | Exact unused days | None | 2-4 weeks |

| Short-Rate Cancellation | Policyholder | Unused days minus 10% penalty | 10% of unearned premium | 2-4 weeks |

| Insurer-Initiated Cancellation | Insurance Company | Full pro-rata refund | None | 1-2 weeks |

| Mutual Agreement | Both parties | Negotiated terms | Varies | 1-3 weeks |

The timing of your refund depends on your insurer's processing procedures and whether you paid annually or monthly. If you paid your premium in full upfront, you'll receive a check or direct deposit. If you were paying monthly, the insurer will simply stop withdrawing payments and refund any overpayment based on the effective cancellation date.

Most insurers process cancellation refunds within two to four weeks, though some take longer during busy periods. If you haven't received your refund within 30 days, contact your insurer's customer service department to inquire about the status.

Step-by-Step Process for Canceling Your Homeowners Policy

Canceling your homeowners insurance requires careful planning and proper documentation to avoid coverage gaps and ensure you receive any refund you're owed. Following these steps in order minimizes risk and streamlines the process.

Before You Cancel: Finding Replacement Coverage First

Never cancel your existing policy until you have confirmed replacement coverage in place. Start shopping for new insurance at least 30 to 45 days before you want to make the switch. This timeline gives you room to compare quotes, complete applications, and resolve any underwriting issues that might arise.

When you receive quotes from new insurers, pay attention to the proposed effective date. You want your new policy to begin on the same day your old policy ends, creating seamless coverage with no gaps. Most insurers can backdate coverage by a few days if needed, but it's cleaner to coordinate the dates upfront.

Once you've selected a new insurer and completed the application, wait for written confirmation that your policy has been approved and bound before canceling your old coverage. A verbal confirmation or quote isn't sufficient—you need a declarations page or binder letter showing your policy number, coverage amounts, and effective date.

If you have a mortgage, inform your new insurer of your lender's name and address so they can send proof of insurance directly to the mortgage servicer. This proactive step prevents confusion and reduces the risk of force-placed insurance.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Submitting Your Cancellation Request

Contact your current insurance company to request cancellation. Most insurers accept cancellation requests through multiple channels: phone calls, written letters, email, or online account portals. However, many companies require written confirmation even if you initiate the request by phone.

When submitting your request, include these key details:

- Your policy number

- The effective date you want the cancellation to take effect

- Your reason for canceling (optional but can be helpful)

- Your mailing address for the refund check

- Confirmation that replacement coverage is in place (if applicable)

Specify the exact cancellation date you want. If you say "immediately" or "as soon as possible," the insurer will interpret this based on their internal policies, which might not align with your new policy's start date. Being specific prevents gaps and overlaps.

Request written confirmation of your cancellation request. This documentation proves you initiated the cancellation and protects you if disputes arise later about timing or refunds.

Confirming Cancellation and Securing Your Refund

Within a few days of submitting your request, you should receive written confirmation from your insurer acknowledging your cancellation and stating the effective date. This letter should also explain how your refund will be calculated and when you can expect to receive it.

Review this confirmation carefully. Verify that the cancellation date matches what you requested and aligns with your new policy's effective date. If there's a discrepancy, contact your insurer immediately to correct it.

If you have a mortgage, follow up with your lender within a week to confirm they received notice of the cancellation and proof of your new coverage. Mortgage servicers sometimes experience delays in updating their insurance tracking systems, and proactive communication prevents unnecessary force-placed insurance.

Keep copies of all cancellation documentation in your files. Save the cancellation confirmation letter, proof that you submitted the request, and records of any phone conversations (note the date, time, and representative's name). This documentation becomes crucial if you need to dispute charges or prove coverage dates later.

Common Mistakes Homeowners Make When Canceling Coverage

Even straightforward cancellations can go wrong when homeowners overlook important details. These mistakes can result in coverage gaps, unexpected charges, or difficulty obtaining insurance in the future.

The most dangerous error is canceling before replacement coverage is confirmed. Some homeowners cancel their existing policy as soon as they receive a quote from a new insurer, not realizing that quotes aren't guaranteed. If the new insurer discovers issues during underwriting—like prior claims, roof age, or inspection problems—they might decline coverage or offer it at a much higher price. Meanwhile, you've already canceled your old policy, leaving you scrambling to find coverage and potentially facing a gap.

Another frequent mistake involves miscommunicating cancellation dates. If you tell your old insurer to cancel "at the end of the month" but your new policy starts on the first of the month, you've created a one-day gap. Insurance companies interpret vague language differently, so always specify exact dates.

Failing to notify your mortgage company directly is also problematic. While your insurer should send cancellation notice to your lender, don't rely on this alone. Send your own notice to your mortgage servicer along with proof of your new coverage. This redundancy ensures they update their records promptly.

Some homeowners cancel policies shortly after filing a claim, not realizing this can create problems when applying for new coverage. Insurance companies share claims history through databases like CLUE (Comprehensive Loss Underwriting Exchange), and canceling immediately after a claim can appear suspicious to future insurers. While you have the right to cancel, consider the optics and potential impact on future insurability.

Not obtaining written confirmation of cancellation is another oversight that can haunt you later. If your insurer continues charging premiums after you thought you canceled, or if there's a dispute about when the cancellation took effect, written documentation is your only proof.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Special Circumstances: When Canceling Makes Sense (and When It Doesn't)

Certain life events naturally trigger homeowners insurance cancellations, while other situations require more careful consideration of whether canceling is truly in your best interest.

Selling your home is the most straightforward cancellation scenario. Once the sale closes and you no longer own the property, you should cancel your policy effective on the closing date. The new owner will purchase their own coverage. Coordinate with your closing attorney or title company to ensure the timing aligns with the property transfer.

Moving to a new home requires canceling your old policy and purchasing coverage for your new property. Many insurers will simply transfer your existing policy to the new address, which can be simpler than canceling and starting fresh. However, if you're moving to a different state or a location with significantly different risk factors, you might need a new policy anyway.

Refinancing your mortgage doesn't require canceling your homeowners insurance, but it's a good opportunity to shop for better rates. Your new lender will require proof of coverage, and you can either keep your existing policy or switch to a new one during the refinance process.

Switching providers for better rates or coverage is one of the most common reasons homeowners cancel policies. If you've found substantially better pricing or more comprehensive coverage elsewhere, canceling and switching makes financial sense. Just ensure the new coverage is truly comparable—cheaper isn't better if it means lower coverage limits or higher deductibles.

Dropping coverage entirely because you own your home outright is legal but extremely risky. Without insurance, you're personally responsible for all repair or replacement costs if your home is damaged by fire, storms, or other perils. You're also liable for injuries that occur on your property, which could result in devastating lawsuits. The premium savings rarely justify the enormous financial risk.

Homeowners should never cancel existing coverage until replacement coverage is firmly in place, regardless of the reason for canceling. A single day without coverage can result in a total financial loss if a fire or other catastrophe occurs. The small savings from canceling early or going without coverage simply isn't worth the risk of losing your most valuable asset

— According to Robert Hunter

Frequently Asked Questions About Canceling Home Insurance

Canceling homeowners insurance is a right you hold as a policyholder, but exercising that right requires attention to timing, documentation, and the practical constraints imposed by mortgage lenders and state regulations. The process itself is straightforward when you follow proper procedures: secure replacement coverage first, submit a written cancellation request with a specific effective date, and confirm that both your insurer and mortgage company have processed the change correctly.

The key to a smooth cancellation is avoiding coverage gaps. Whether you're switching to a cheaper policy, moving to a new home, or dealing with any other circumstance that requires ending your current coverage, never let your existing policy lapse before new coverage begins. The financial risk of even a single day without insurance far outweighs any potential savings from canceling early.

Understanding the refund calculation methods, potential penalties, and your insurer's specific procedures helps you plan the cancellation timeline and set realistic expectations for when you'll receive any money back. Most importantly, maintaining written documentation of every step protects you if disputes arise and provides proof of continuous coverage for future insurance applications.