Two homeowners insurance policy documents on a wooden desk with a house model, keys, calculator, and pen, one policy crossed out and one signed

How to Change Your Homeowners Insurance Without Gaps or Penalties

Content

Yes, you can change your homeowners insurance at virtually any time—there's no legal waiting period or mandatory lock-in. Unlike health insurance with its annual enrollment windows, property insurance operates under different rules that favor consumer choice. However, "can you" and "should you" are separate questions, and the timing, method, and circumstances of your switch matter significantly.

The freedom to change carriers comes with practical considerations: potential cancellation fees, coordination with your mortgage servicer, avoiding gaps in coverage, and understanding how your switching history affects future insurability. Most homeowners don't realize that while they're legally free to switch, doing so incorrectly can create expensive problems.

When You're Legally Allowed to Switch Homeowners Insurance

No federal law restricts when you can change your homeowners insurance. State insurance regulations universally allow policyholders to cancel coverage with proper notice—typically 30 days for voluntary cancellations initiated by the homeowner. This applies whether you're three months into a new policy or approaching your renewal date.

Your insurance company must accept your cancellation request regardless of timing, though they can impose financial penalties for mid-term cancellations (more on this later). The only exception involves fraud or material misrepresentation during the application process, which could complicate cancellation.

State-specific rules affect the notice period and refund calculations. California requires insurers to provide pro-rata refunds with no penalty when homeowners cancel. Texas allows short-rate cancellations where insurers keep a percentage as an administrative fee. Check your policy declarations page for the exact cancellation clause applicable to your policy.

Author: Lauren Bishop;

Source: sixth-fleet.com

Mortgage company notification represents a practical rather than legal restriction. If your home carries a mortgage, your lender holds a financial interest in the property and must be named as a loss payee on any policy. Most loan agreements require 30-60 days' notice before changing insurance. Failure to notify your lender properly can trigger force-placed insurance—an expensive backup policy the lender purchases and charges to your account.

The policy change homeowners insurance process guide varies by state, but the underlying principle remains consistent: you control when to switch, and insurers must facilitate that choice within regulatory guidelines.

Common Scenarios That Trigger a Policy Change

Homeowners switch insurance for concrete reasons, not on impulse. Rate increases top the list—many carriers raise premiums 10-30% at renewal without corresponding improvements in coverage. If your premium jumped $600 annually and you can secure identical coverage for $400 less elsewhere, switching makes financial sense.

Poor claims handling drives many switches. When an insurer denies a legitimate water damage claim or lowballs a roof replacement estimate by thousands, trust erodes. Homeowners often discover during the claims process that their "full coverage" policy contains exclusions they didn't understand.

Life changes frequently necessitate policy changes. Refinancing your mortgage might reveal that your current coverage doesn't meet the new lender's requirements. Moving into a home with a swimming pool, trampoline, or certain dog breeds can prompt your current insurer to non-renew, forcing you to find a carrier that accepts these risk factors.

Finding better coverage for less money happens more often than people expect. Insurance companies adjust their risk appetites constantly. A carrier that offered you mediocre rates three years ago might now have competitive pricing in your ZIP code, or a regional insurer you didn't know about offers superior coverage at 20% less.

Switching After a Claim: What to Expect

Filing a claim doesn't prevent you from switching, but it complicates the process. Your current insurer must continue processing the claim even after you cancel—they remain liable for covered losses that occurred during your policy period. However, switching immediately after a large claim often triggers higher quotes from new carriers.

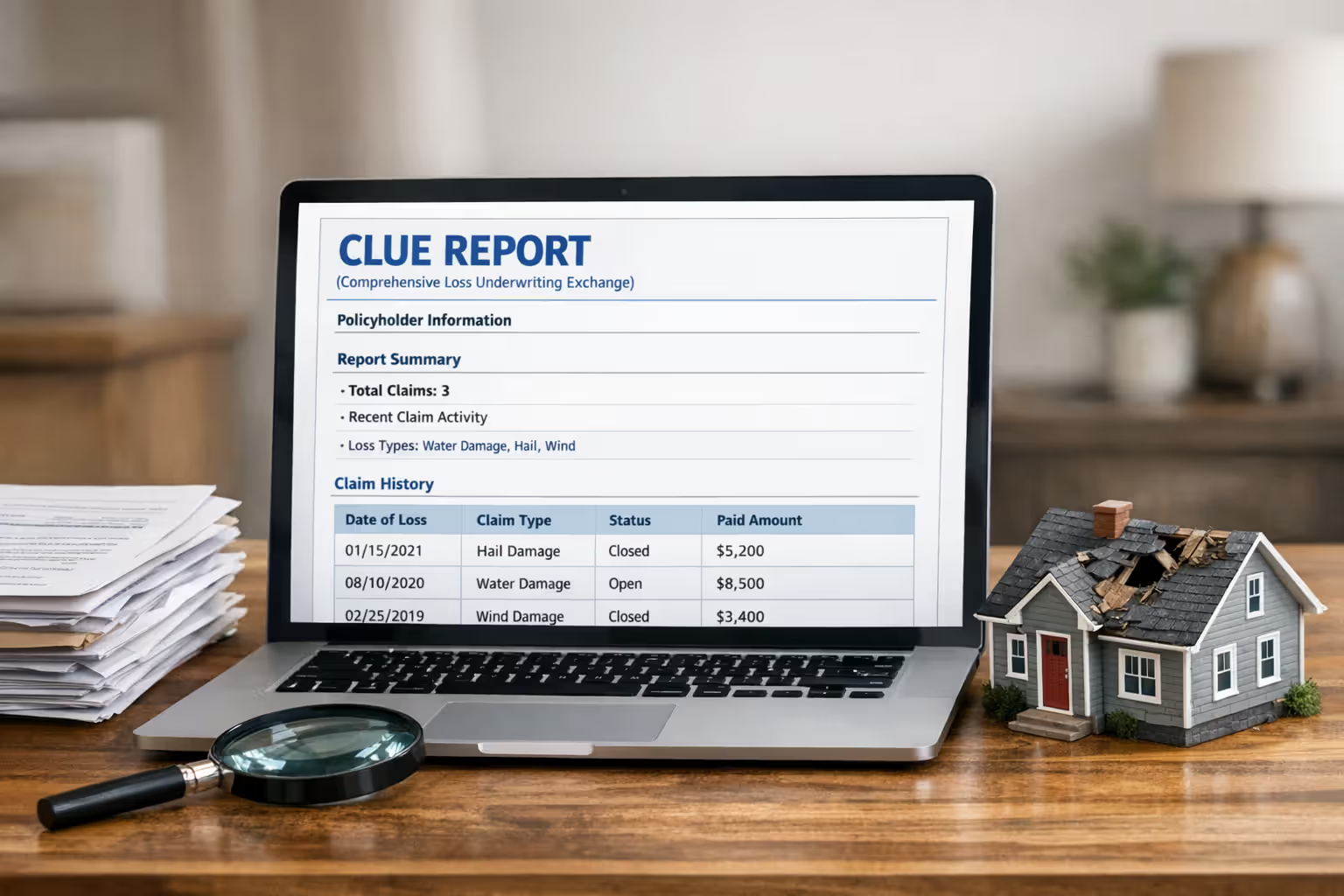

Insurance companies view recent claims as predictors of future losses. A $15,000 roof claim filed two months ago will appear on your Comprehensive Loss Underwriting Exchange (CLUE) report, visible to all insurers for seven years. Expect new carriers to either increase your premium, exclude certain coverages, or decline to write your policy altogether.

The strategic approach: if you're unhappy with your insurer but anticipate filing a claim soon, file the claim first. Switching before filing means your new insurer handles the claim, which could work in your favor if they have better claims service. But if the loss occurred during your old policy period, even by one day, the old insurer remains responsible.

Author: Lauren Bishop;

Source: sixth-fleet.com

Changing Policies Mid-Term vs. at Renewal

Switching at renewal avoids cancellation fees entirely. Your policy simply expires, and you start fresh with a new carrier on the renewal date. No penalties, no complicated refund calculations, and no risk of the old insurer imposing short-rate charges.

Mid-term switches offer flexibility when you've found significantly better coverage or rates. If you're paying $2,400 annually and find identical coverage for $1,600, waiting eight months until renewal costs you roughly $533 in unnecessary premiums—likely more than any cancellation fee. The math matters.

Timing affects your new policy's annual renewal date. Switch mid-term, and your renewal date changes permanently. Some homeowners prefer aligning their insurance renewal with their mortgage escrow analysis or tax season for easier budgeting. Others don't care about the date and prioritize immediate savings.

Step-by-Step Process for Changing Homeowners Insurance Providers

Step 1: Shop and compare before canceling anything. Request quotes from at least three carriers, providing identical coverage specifications—same dwelling coverage limit, deductible, liability limits, and endorsements. Generic quotes based on different coverage levels tell you nothing useful. Many homeowners compare a $250,000 dwelling limit quote against their current $350,000 policy and think they've found a bargain.

Step 2: Review mortgage requirements. Contact your loan servicer and request their insurance requirements document. They'll specify minimum dwelling coverage (usually replacement cost), required liability limits, deductible maximums, and acceptable carrier ratings. Some lenders won't accept carriers rated below A- by AM Best.

Step 3: Select your new policy and set the effective date. Choose a start date that allows for proper coordination—typically 2-4 weeks out. Never set the effective date for the same day you're shopping. You need time to review the actual policy documents, not just the quote.

Step 4: Pay the first premium and obtain proof of insurance. Your new policy isn't active until payment clears. Request the declarations page and evidence of insurance letter immediately. Send copies to your mortgage servicer within 24 hours of binding coverage.

Step 5: Confirm the new policy is active. Call your new insurer and verify coverage is in force. Check that your property address, coverage limits, and mortgagee information appear correctly on the declarations page. Errors here create coverage gaps.

Step 6: Cancel your old policy. Submit written cancellation to your old insurer specifying the cancellation date—which should match your new policy's effective date exactly. Email works, but certified mail provides proof of delivery. Most insurers also accept cancellation via their online portal.

Step 7: Follow up on refunds and escrow adjustments. Your old insurer should issue a refund for unused premium within 30 days. If you pay through escrow, notify your mortgage servicer about the refund and request an escrow analysis to adjust future payments based on your new premium.

Author: Lauren Bishop;

Source: sixth-fleet.com

Documentation needed throughout this process: current policy declarations page, mortgage loan number, property deed or closing documents, home inspection report (if recent), and CLUE report. Order your CLUE report free annually at LexisNexis to review what information insurers see about your claims history.

The changing homeowners insurance providers steps guide requires attention to sequencing. Canceling before your new policy activates, even by one day, leaves you uninsured. If a fire occurs during that gap, you're personally liable for the entire loss—potentially hundreds of thousands of dollars.

Potential Costs and Penalties When Switching Policies

Insurance companies impose cancellation fees to recoup administrative costs and discourage frequent switching. These fees vary significantly based on timing and your policy's specific terms.

Pro-rata refunds return the exact unused portion of your premium with no penalty. If you paid $1,200 for annual coverage and cancel after six months, you receive $600 back. Several states mandate pro-rata refunds for policyholder-initiated cancellations.

Short-rate refunds penalize early cancellation by withholding 10-15% of the unearned premium as an administrative fee. Using the same example, you'd receive approximately $510-$540 instead of $600. The insurer keeps the difference.

Flat cancellation fees charge a fixed amount—typically $25-$75—regardless of when you cancel. This approach is less common but simpler to calculate.

Minimum earned premium clauses require the insurer to keep a certain amount even if you cancel within days. Some policies specify a $100-$200 minimum earned premium, meaning early cancellation yields little or no refund.

| Timing of Cancellation | Refund Calculation Method | Typical Fee Range | Coverage Gap Risk |

| At renewal (policy expiration) | Full premium paid for new term only | $0 | Low—clean transition |

| Mid-term (1-6 months in) | Short-rate: 10-15% penalty on unearned premium | $50-$200 | High if not coordinated |

| Mid-term (7-11 months in) | Pro-rata or short-rate | $25-$100 | Moderate |

| Within first 30 days | Minimum earned premium applies | $100-$200 retained | High—rushed transition |

New policy fees add to switching costs. Most insurers charge $25-$100 in policy fees at inception. If you're switching to save $200 annually but pay a $75 cancellation fee and $50 new policy fee, your first-year net savings drops to $75.

Escrow account adjustments can temporarily increase your monthly mortgage payment. When you switch to a cheaper policy, your escrow account holds excess funds collected for the old, higher premium. The servicer should refund this excess or apply it to future payments, but timing varies. Conversely, switching to a more expensive policy may require an immediate escrow shortage payment.

Mistakes to Avoid When Replacing Your Homeowners Insurance

Canceling before the new policy activates ranks as the costliest error. Homeowners assume they can cancel today and start new coverage tomorrow, but underwriting, payment processing, and policy issuance take time. A three-day gap without coverage could mean total financial loss if disaster strikes.

Comparing unlike coverage leads to false savings. A quote for $200,000 dwelling coverage with a $2,500 deductible costs less than your current $300,000 coverage with a $1,000 deductible—but you're not comparing equivalent protection. Match every coverage element: dwelling, other structures, personal property, loss of use, liability, medical payments, deductibles, and endorsements.

Ignoring replacement cost vs. actual cash value creates nasty surprises after a loss. Actual cash value policies cost less but pay depreciated amounts. Your 15-year-old roof might cost $12,000 to replace, but an ACV policy pays perhaps $4,000 after depreciation. Always verify you're getting replacement cost coverage on both the dwelling and personal property.

Switching too frequently damages your insurance profile. Carriers view homeowners who switch every 6-12 months as unstable risks. Some insurers won't quote policies for applicants who've had three or more carriers in five years. Frequent switching also increases the chance of coverage gaps and administrative errors.

Not reading the actual policy before canceling the old one leaves you vulnerable. Quotes and declarations pages summarize coverage, but the full policy contains exclusions and limitations that matter. That cheap policy might exclude water backup, reduce windstorm coverage, or contain a percentage deductible for hurricanes that makes it nearly useless in coastal areas.

Failing to update your mortgage servicer promptly can trigger force-placed insurance. Lenders monitor insurance coverage continuously. If they don't receive proof of your new policy within their required timeframe—often 30 days—they'll purchase expensive backup coverage and bill you. Force-placed insurance costs 2-3 times more than standard policies and provides minimal coverage.

Author: Lauren Bishop;

Source: sixth-fleet.com

How Your Mortgage Lender Affects Your Ability to Switch

Your mortgage agreement grants the lender substantial control over insurance requirements. The loan documents specify minimum coverage amounts, acceptable deductibles, and carrier financial strength ratings. Switching to a policy that doesn't meet these requirements constitutes a loan agreement violation.

Escrow accounts complicate switching by creating a three-party payment system. You pay the lender, who pays the insurer. When you switch, you must coordinate with both. The old insurer refunds unearned premium to you or the escrow account (depending on who paid). The new insurer bills either you directly or the escrow account. Miscommunication here creates payment confusion and potential coverage lapses.

Lender approval isn't legally required, but practical necessity makes it feel mandatory. Technically, you can switch without asking permission, but if your new policy doesn't satisfy loan requirements, the lender will force-place insurance. Better to submit your new policy documents for review before canceling the old coverage.

Force-placed insurance represents the lender's nuclear option. If they can't verify continuous coverage meeting their standards, they'll purchase a bare-bones policy covering only their financial interest—not your personal property, liability, or loss of use. These policies cost $3,000-$5,000 annually for coverage you could buy for $1,200-$1,500. The lender adds this cost to your loan balance or escrow account.

Notification timelines vary by lender but typically require 30-60 days' notice before changing insurance. Submit your new policy's declarations page, evidence of insurance form, and a letter confirming continuous coverage with no gaps. Include your loan number on all correspondence.

Some lenders restrict which insurers they'll accept. They maintain approved carrier lists based on AM Best ratings and claims-paying history. A small regional insurer offering great rates might not appear on your lender's approved list, forcing you to choose between the savings and lender compliance.

Homeowners have the right to change insurance carriers at any time, but they should never cancel existing coverage until new coverage is confirmed in writing and they've verified their mortgage company has received proper notification. The risks of a coverage gap far outweigh any potential savings from rushing the switch

— According to Amy Bach

FAQ: Switching Homeowners Insurance Policy

Changing homeowners insurance offers real benefits when done correctly: lower premiums, better coverage, improved customer service, or all three. The freedom to switch at any time gives you leverage as a consumer—insurers know they must remain competitive or lose your business.

The key is treating the switch as a deliberate project rather than an impulsive reaction to a single rate increase. Compare actual coverage details, not just premiums. Coordinate timing carefully to avoid gaps. Communicate with your mortgage servicer proactively. Read your new policy documents before canceling old coverage.

Most importantly, switch for substantive reasons—meaningful savings, genuinely better coverage, or documented service problems—not because an aggressive agent made switching sound urgent. Your insurance protects potentially your largest financial asset. That protection deserves careful consideration, whether you're staying with your current carrier or making a change.