Homeowners insurance policy document on wooden desk with calculator, house keys, and small wooden house model

How to Buy Homeowners Insurance the Right Way Before Closing

Content

Purchasing homeowners insurance isn't just a formality—it's a financial decision that can determine whether you recover from a disaster or face bankruptcy. Most mortgage lenders require proof of coverage before closing, but even if you own your home outright, the right policy protects what's likely your largest asset. The process involves more than comparing premiums; you'll need to assess your actual replacement costs, understand coverage gaps, and navigate policy language that often hides critical exclusions.

Understanding What Homeowners Insurance Covers Before You Shop

Standard homeowners policies divide protection into four main sections, and knowing these categories helps you identify gaps before you buy.

Dwelling coverage pays to rebuild your home if it's damaged or destroyed by covered perils like fire, wind, or hail. This doesn't include your land—only the structure and attached features like built-in appliances, plumbing, and electrical systems. A common misconception: dwelling coverage doesn't automatically match your home's market value or the amount you paid for it.

Personal property coverage protects your belongings—furniture, clothing, electronics, and other possessions. Most policies cover 50-70% of your dwelling amount for personal property. If your home has $300,000 in dwelling coverage, you'd typically receive $150,000-$210,000 for belongings. Special limits apply to jewelry, art, and collectibles, often capping payouts at $1,000-$2,500 unless you purchase additional riders.

Liability protection covers legal expenses and damages if someone gets injured on your property or you accidentally damage someone else's property. Standard policies offer $100,000-$300,000, but that won't stretch far in serious injury lawsuits. Medical payments coverage, a subset of liability, pays small medical bills ($1,000-$5,000) regardless of fault when guests get hurt.

Additional living expenses (ALE) reimburses hotel bills, restaurant meals, and storage costs if your home becomes uninhabitable during repairs. This coverage typically lasts 12-24 months and caps at 20-30% of your dwelling amount. After a major fire, you might face six months in temporary housing—ALE prevents that from draining your savings.

Standard policies exclude certain perils entirely. Floods require separate federal or private flood insurance. Earthquakes need specific endorsements. Sewer backups, foundation cracks from settling, and damage from lack of maintenance aren't covered. Understanding these obtain homeowners insurance coverage guide fundamentals prevents surprises when you file a claim.

Calculating How Much Coverage You Actually Need

Guessing at coverage amounts leaves you either overpaying for protection you don't need or facing massive out-of-pocket costs after a loss. Two calculations matter most: replacement cost for your home and appropriate liability limits.

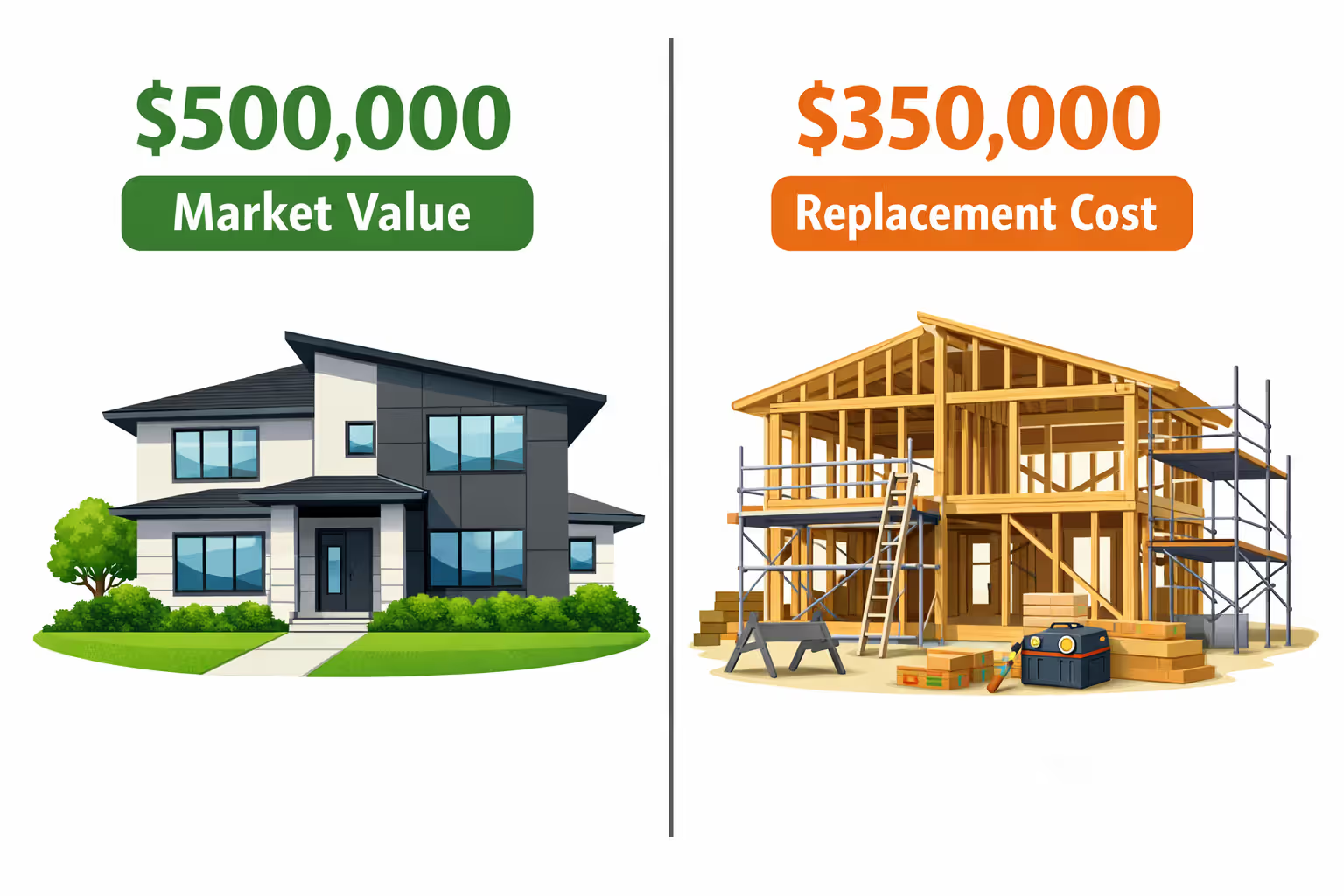

Replacement Cost vs. Market Value

Your home's market value includes your land and reflects what buyers will pay in your neighborhood. Replacement cost measures what it would cost to rebuild your home from scratch at today's construction prices—and that's what matters for insurance.

In hot real estate markets, market value often exceeds replacement cost. A $500,000 home might cost only $350,000 to rebuild because $150,000 of that price represents land value and location desirability. Insuring for market value means overpaying on premiums.

The opposite scenario creates bigger problems. In areas with expensive labor or building code requirements, replacement costs can exceed market value. After the 2017 California wildfires, many homeowners discovered their $400,000 homes would cost $600,000 to rebuild due to labor shortages and updated building codes. Their policies covered only the insured amount, leaving them with massive shortfalls.

Most insurers offer replacement cost estimators, but hire an independent appraiser for homes with custom features, high-end finishes, or unusual architecture. Budget $300-$500 for this appraisal—it's cheaper than discovering you're underinsured after a total loss. Include detached structures like sheds or garages in your calculations; they're typically covered at 10% of dwelling coverage unless you purchase additional protection.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Extended or guaranteed replacement cost endorsements pay above your policy limit if construction costs spike after a widespread disaster. These add 10-20% to premiums but provide crucial protection in catastrophe-prone areas.

Liability Coverage Amounts by Net Worth

Financial advisors recommend liability coverage equal to your net worth. Someone with $800,000 in assets needs at least $500,000-$1,000,000 in liability protection. Why? If you're found liable for $750,000 in damages but only carry $300,000 in coverage, plaintiffs can pursue your bank accounts, retirement funds, and other assets for the remaining $450,000.

Umbrella policies provide additional liability coverage beyond your homeowners policy, typically in $1 million increments. A $1 million umbrella policy costs $150-$300 annually—far less than the potential financial devastation of an underinsured liability claim. These policies require minimum underlying coverage, usually $300,000-$500,000 on your homeowners policy.

7 Steps to Purchase Your Homeowners Insurance Policy

The homeowners insurance buying process guide involves systematic preparation and comparison. Rushing through these purchase homeowners insurance policy steps leads to coverage gaps or overpaying.

Step 1: Inventory your belongings. Walk through your home with a smartphone, recording video of each room and narrating descriptions of valuable items. Open closets, drawers, and cabinets. Photograph serial numbers on electronics and appliances. This documentation serves two purposes: it helps you calculate accurate personal property coverage needs, and it becomes crucial evidence if you file a claim. Store this inventory in cloud storage, not just on your phone.

Step 2: Research insurers and check financial ratings. Not all insurance companies can pay claims after major disasters. Check AM Best ratings (A- or higher), state complaint ratios through your insurance commissioner's website, and customer service reviews. A company with slightly higher premiums but excellent claims handling beats a cheap policy from an insurer that fights every claim. Look for companies with strong presence in your state—they understand local risks and building costs better.

Step 3: Gather necessary documents. You'll need your home's purchase date and price, square footage, year built, roof age and material, heating and electrical system details, security system information, and claims history for the past 5-7 years. Have your mortgage statement handy with your lender's contact information. If you've made major renovations, collect receipts and permits.

Author: Ethan Caldwell;

Source: sixth-fleet.com

Step 4: Request quotes from multiple insurers. Get at least 3-5 quotes. Contact insurers directly, work with independent agents who represent multiple companies, or use comparison websites—but verify any online quotes with direct phone calls. Provide identical information to each insurer for accurate comparisons. Ask specifically about available discounts: bundling home and auto, security systems, new home construction, claims-free history, or professional affiliations.

Step 5: Compare policies beyond the premium. The cheapest policy often has higher deductibles, lower coverage limits, or more exclusions. Review each quote's dwelling coverage amount, personal property limits, liability protection, deductible, and specific exclusions. Some policies use actual cash value (which depreciates) instead of replacement cost for personal property—a significant difference when claiming a five-year-old laptop or couch.

Step 6: Complete the application. Applications ask detailed questions about your property and claims history. Answer honestly—misrepresentations can void your policy. Insurers verify information through databases like CLUE (Comprehensive Loss Underwriting Exchange), which tracks claims history. If you've filed claims in the past five years, expect questions about circumstances and whether issues were fully repaired.

Step 7: Finalize payment and documentation. Most insurers offer monthly or annual payment options. Paying annually often saves 5-10% compared to monthly installments. You'll receive declarations pages summarizing coverage, a full policy document, and proof of insurance for your mortgage lender. Read the full policy—not just the declarations—to understand exclusions and claim procedures.

Comparing Quotes: What to Look for Beyond the Premium Price

A buying insurance homeowners policy guide isn't complete without understanding how to evaluate competing quotes. Price differences often reflect coverage variations that aren't obvious at first glance.

Deductibles represent your out-of-pocket cost before insurance pays. A $500 deductible means you pay the first $500 of any claim. Higher deductibles lower premiums but increase financial exposure. Some policies use percentage deductibles (1-5% of dwelling coverage) for specific perils like wind or hail. On a $300,000 home, a 2% deductible means paying $6,000 before coverage kicks in—manageable for some, devastating for others.

Coverage limits vary by category. One quote might offer $300,000 dwelling coverage with $150,000 personal property, while another provides $300,000 dwelling but only $100,000 personal property. Check liability limits carefully—$100,000 might seem adequate until you face a serious injury lawsuit.

Exclusions and endorsements hide in policy fine print. Some policies exclude dog bites for certain breeds, water damage from specific sources, or home business equipment. Others automatically include ordinance or law coverage (which pays for building code upgrades during repairs) while competitors charge extra. Identity theft protection, equipment breakdown coverage, and water backup protection are common add-ons that vary by insurer.

Discount availability changes your effective premium. A policy that initially appears expensive might become competitive after applying discounts for bundling, security systems, or claims-free history. Ask each insurer to list every discount you qualify for.

Insurer ratings and reputation matter when you're standing in front of your damaged home. An insurer with a strong financial rating (AM Best A or higher) and good claims service reputation provides peace of mind worth a modest premium difference.

| Insurance Company | Annual Premium | Deductible | Dwelling Coverage | Personal Property | Liability Limit | Key Features/Notes |

| SafeHome Insurance | $1,240 | $1,000 | $350,000 | $262,500 (75%) | $300,000 | Includes water backup coverage; 15% multi-policy discount applied |

| Premier Protect | $1,095 | $2,500 | $350,000 | $175,000 (50%) | $100,000 | Lower personal property and liability; excludes certain dog breeds |

| Nationwide Shield | $1,380 | $1,000 | $350,000 | $262,500 (75%) | $500,000 | Guaranteed replacement cost; includes identity theft protection |

| ValueGuard Home | $985 | $2,500 | $325,000 | $195,000 (60%) | $300,000 | Lower dwelling coverage; actual cash value on roof over 15 years old |

This comparison reveals why the cheapest option isn't always best. ValueGuard's $985 premium looks attractive until you notice the lower dwelling coverage and roof depreciation clause. Premier Protect's low price comes with reduced personal property coverage and liability limits that might not adequately protect higher-net-worth homeowners. SafeHome and Nationwide Shield offer more comprehensive protection, with Nationwide providing guaranteed replacement cost—valuable after catastrophic losses when construction costs spike.

Common Mistakes That Cost Homeowners Thousands

Author: Ethan Caldwell;

Source: sixth-fleet.com

Underinsuring the dwelling is the most expensive mistake. Homeowners often insure based on purchase price or rough estimates rather than actual replacement cost. After a total loss, they discover their $250,000 policy won't rebuild their $400,000 home. Review replacement cost estimates every 2-3 years, especially after renovations or in high-inflation periods.

Ignoring replacement cost guarantees leaves you vulnerable to construction cost inflation. Standard policies pay only up to your coverage limit. Extended replacement cost (typically 125-150% of dwelling coverage) or guaranteed replacement cost (no cap) endorsements add 10-20% to premiums but eliminate the risk of being underinsured after widespread disasters that strain construction resources.

Skipping flood and earthquake coverage because "it won't happen here" backfires regularly. Standard homeowners policies exclude these perils entirely. Flood insurance through the National Flood Insurance Program or private insurers costs $400-$2,000 annually depending on flood zone. Earthquake coverage varies by region but typically adds 10-20% to premiums in high-risk areas. Even moderate-risk areas experience these disasters—Houston homeowners learned this during Hurricane Harvey when thousands of homes outside flood zones flooded.

Not bundling policies means overpaying. Combining home and auto insurance with one company typically saves 15-25% on both policies. Some insurers offer additional discounts for adding umbrella policies or other coverage types. Calculate total costs across all policies when comparing insurers.

Failing to update your policy after major life changes leaves coverage gaps. Finished the basement? Your dwelling coverage might not reflect the added value. Bought expensive jewelry or art? Standard personal property limits won't cover these items without scheduled endorsements. Started a home business? Your policy likely excludes business property and liability—you'll need a business policy or endorsement.

Homeowners consistently underestimate replacement costs by 20-30% on average, leaving them dramatically underinsured when disaster strikes. The single most important thing you can do is get an independent replacement cost estimate and review it every three years. Construction costs change, and your coverage needs to keep pace

— Janet Ruiz

When to Buy: Timing Your Purchase for Closing and Renewals

Mortgage lenders require proof of insurance before closing. Most lenders want coverage effective on the closing date, with the lender named as mortgagee on the declarations page. Start shopping 2-4 weeks before your closing date. This provides time to compare multiple quotes, ask questions, and avoid rushed decisions.

Some buyers wait until the week before closing, then panic and accept the first available policy. This often means overpaying or accepting inadequate coverage. Others purchase insurance too early—most insurers won't bind coverage more than 60 days in advance.

If closing gets delayed, contact your insurer immediately. Policies typically can't start before you own the home. Some insurers charge fees for changing effective dates, while others adjust without penalty.

Renewal shopping saves money long-term. Insurance companies often raise premiums at renewal, betting that customers won't shop around. Set a calendar reminder 45-60 days before your renewal date to request new quotes. You're not locked into your current insurer—switching mid-policy is possible, though you might owe a small cancellation fee or lose discounts for policy longevity.

Review your policy annually even if you don't switch insurers. Confirm dwelling coverage still matches replacement costs, update personal property values, and ask about new discounts. Life changes like paying off your mortgage, installing security systems, or retiring might qualify you for reduced rates.

Frequently Asked Questions About Buying Homeowners Insurance

Once you've selected a policy and completed the application, several administrative steps ensure smooth coverage activation and ongoing protection.

Payment setup determines when coverage begins. Most insurers require first payment before binding coverage. Choose annual payment if possible—it saves 5-10% compared to monthly installments and eliminates the risk of coverage lapsing due to missed payments. If monthly payments fit your budget better, set up automatic payments from your bank account. Credit card payments often incur 2-3% processing fees.

Document storage prevents scrambling during emergencies. Save digital copies of your declarations page, full policy document, and proof of insurance in cloud storage accessible from your phone. Keep physical copies in a fireproof safe or off-site location—you can't file a claim if your only policy copy burns with your house. Give a copy to trusted family members who might need to help you after a disaster.

Sharing information with your mortgage company satisfies lender requirements and prevents forced-place insurance. Send your declarations page and proof of insurance to your lender immediately after purchase. Most lenders require annual proof of coverage renewal—mark your calendar to send updated documents each year. If you escrow insurance payments through your mortgage, provide your insurer's payment address to your lender.

Setting calendar reminders helps you maintain optimal coverage. Create reminders for 60 days before renewal to shop competing quotes, annual policy reviews to update coverage amounts, and periodic home inventory updates after major purchases. Set a reminder to photograph new valuables and save receipts for items over $500.

Buying homeowners insurance isn't a one-time transaction—it's an ongoing relationship that requires periodic attention. The effort you invest in understanding coverage types, calculating accurate replacement costs, comparing detailed quotes, and maintaining updated policies determines whether insurance truly protects your financial security or leaves you vulnerable when you need it most. Take the time to purchase thoughtfully rather than defaulting to the cheapest or most convenient option. Your future self, standing in front of a damaged home with adequate coverage and a responsive insurer, will appreciate the careful decision-making you did today.